- Startups are still expanding into the US, but they are doing so later in their lifecycle.

- Government spending in defense tech has increased, particularly in Europe, and venture investment has followed.

- Military conflict – particularly in the Middle East – is introducing new geopolitical risk variables that are slowing near-term deal activity while leaving longer-term global market outlooks intact.

Our latest global markets report highlights a familiar theme: the reorganization of the innovation economy during times of transition. Capital, talent and company-building strategies are adapting to uncertainty.

Three takeaways stand out for early-stage founders navigating global startup expansion in 2026:

1. Founders are still coming to the US, just later than before.

For decades, the default playbook for global startups was clear: build locally, then move quickly into the US to access capital and customers. That playbook has started to change.

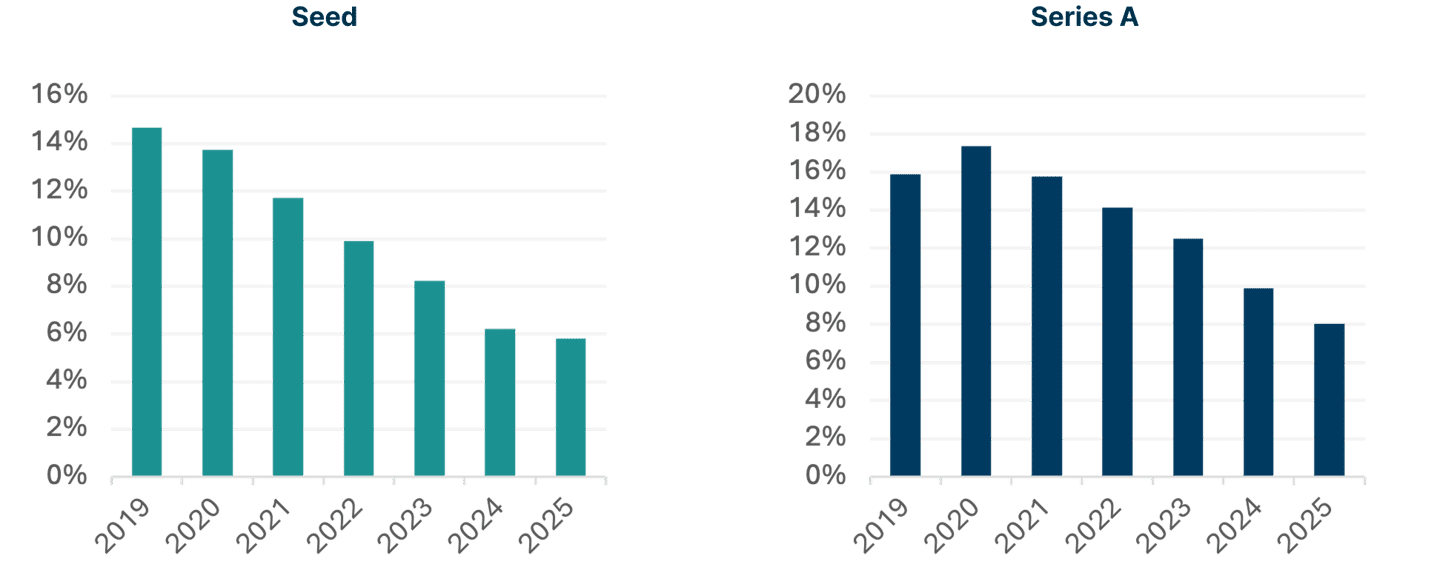

Companies are still expanding into the US, but they are doing so later in their lifecycle. In 2019, about 14% of seed-stage companies had already opened a US office. By 2025, that figure dropped to just under 6%, according to data from PitchBook. This trend has held at later stages as well.

Percentage of global companies with a US office

This shift reflects a couple of dynamics. First, local ecosystems have matured. In India, for instance, a robust IPO market has provided a pathway for founders to grow their companies from inception through public listing, without the need to access capital markets in the US. Second, policy friction — particularly around visas — has made US expansion more complex. Issuance of visas commonly used by startup founders — such as H1B, O1 and E2 visas — has trended down the past two years, according to data from the US State Department. This has led many early-stage companies to question whether they need to expand into the US or if they can reach their growth goals regionally, for instance expanding through Asian or European markets.

Still, the US remains the center of gravity, especially for AI. Silicon Valley remains the “place to be” for founders of AI companies, drawn to the talent, capital, technical expertise and network. Even with these draws, for many startups the path to the US market is longer and more complex than it once was.

2. Defense tech's rise is bolstered by today's geopolitics.

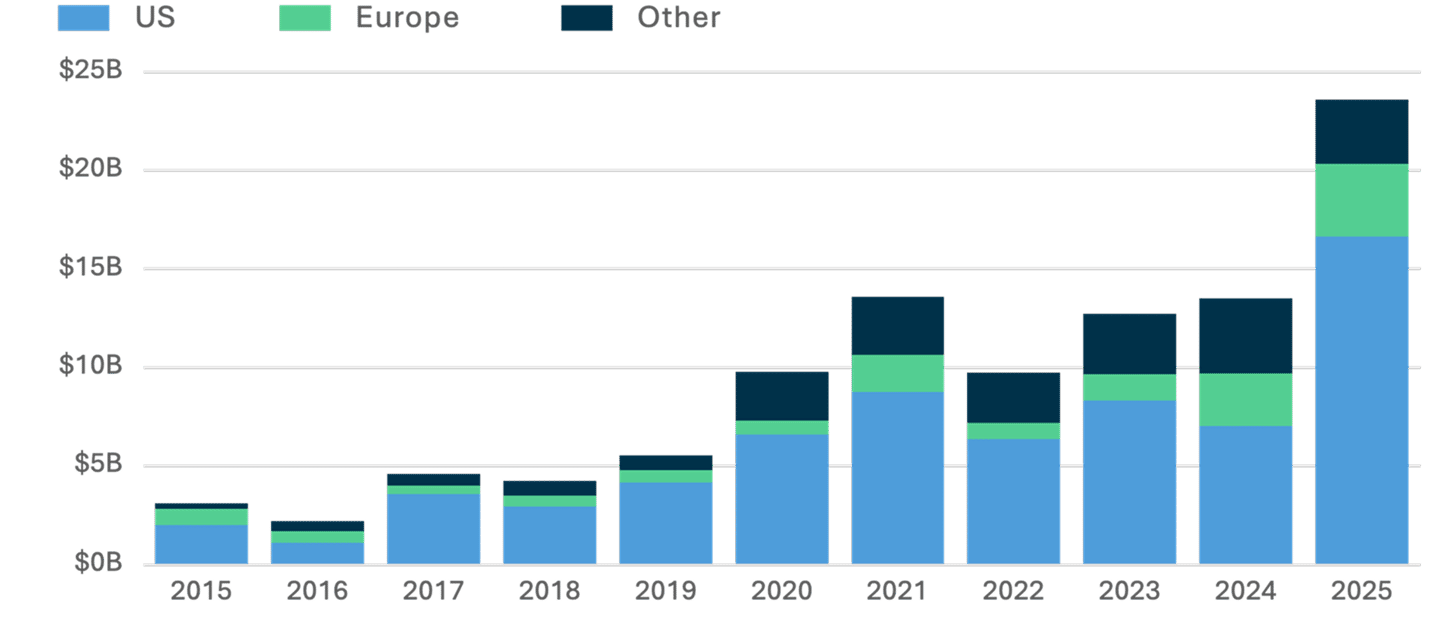

Five years ago, defense tech sat outside mainstream venture culture. Today, it is a core area of focus. Government spending has increased materially, particularly in Europe, and venture investment has followed.

Defense tech venture funding increased more than 350% in Europe between 2022 and 2025.1 Initially, the war in Ukraine was a primary driver for increased military spending and venture investment. Sustained demand for drones and cyber capabilities created a persistent need for innovation and technology in this vertical. That demand is now compounding, with the Iran war reinforcing many of the same needs at perhaps an even broader scale.

VC and growth investment into defense, by region and year

Drone warfare, missile defense and infrastructure vulnerability are at the center of this rapidly evolving landscape, and innovative startups play a key role in delivering these technologies.

Governments are responding accordingly, aiming for faster procurement cycles and a greater willingness to engage with newer, venture-backed companies. In the US, for instance, the “Acquisition Transformation Strategy,” released by the current Administration’s Department of War in 2025, aims to leverage private investment and increase innovation in military procurement.

While the ultimate effectiveness of these policy changes remains to be seen, it is a strong signal. Early-stage founders may find opportunities by developing “dual-use” defense applications of their otherwise commercial product lines. Venture capitalists (VCs), meanwhile, are primed to invest in innovative startups in this sector, as they see more consistent demand than in past cycles. In short, defense tech has become a sustained area of funding within the broader innovation economy.

3. Military conflict is this cycle’s wildcard.

While widening military conflict has fueled defense tech investment, its broader implications for the global innovation ecosystem remain uncertain. Since the report’s publication, fighting in the Middle East has escalated. It’s important to acknowledge upfront that the human cost outweighs any economic analysis. However, here we refer exclusively to implications for startup activity and venture investment. While the situation continues to evolve in unexpected ways, two dynamics are shaping how founders and investors are responding:

Near-term caution. Clients are reporting a slowing of deal activity as investors and founders navigate ongoing uncertainty. Chief among the concerns is whether key commercial centers — Dubai, Abu Dhabi, Doha and others — can continue to attract global talent and capital amid escalating security risks. In the near-term, VCs are hitting “pause” on deals as they assess how the conflict will unfold. In fact, startup funding in the Middle East and North Africa decreased 85% from February to March, according to data from Wamda. For founders in the region, this translates to potential delays in funding rounds, particularly at the series A or B stages.

Longer-term optimism. Despite near-term hesitation, there is broader confidence that capital flows will eventually normalize as the conflict resolves. Early-stage founders that are just starting to launch their ventures may find that they have timed the market well. By the time they are ready for a Series A round, the funding environment — and geopolitical situation generally — may have stabilized. The guiding principle echoes the early days of other macro disruptions like COVID or tariffs — maintain momentum through a period of uncertainty while anticipating a return to normalcy.

The full impact of the conflict on the regional startup ecosystem remains to be seen. Whether the situation resolves quickly or continues for an extended length of time, one thing is clear: Geopolitical risk has become a core consideration in investment and scaling decisions across the global innovation economy.

Closing

The common thread across each of these themes is resilience and adaptation to a changing landscape. Internationally-based founders are adjusting where and when they scale in response to evolving policy, especially related to immigration. They are often delaying their entry into the US market. VCs meanwhile are focusing capital on sectors aligned with a more complex world, with escalating military conflicts encouraging investment in defense tech. Founders are taking notice, with startups more likely today than in the past to push forward the military applications of their products.

The innovation economy remains intensely global, but today it must operate with a more explicit understanding of geopolitics than it did a decade ago. While investment priorities and company strategies will undoubtedly evolve over time, we are confident that investors and founders will meet today’s challenges with flexibility.