- In 2023, the Secured Overnight Financing Rate (SOFR) became the benchmark interest rate that replaced the London Interbank Offered Rate (LIBOR) as the standard reference rate for dollar-denominated short-term funding.

- SOFR is essentially a real-time indicator of short-term dollar funding conditions, heavily influenced by Federal Reserve policy but also sensitive to market liquidity, Treasury supply and market stress.

- Today, SOFR remains slightly elevated relative to the fed funds rate, but we do not think this represents mounting pressure on US funding markets. Rather, this dynamic is likely temporary and demonstrates a healthy ability for the market to self-correct.

Economic vista: The scoop on SOFR

Christi Fletcher, Senior Portfolio Manager

There’s a new sheriff in town, and its name is SOFR.

Ever since mid-2023, SOFR became the benchmark interest rate that replaced LIBOR as the standard reference rate for dollar-denominated derivatives and loans, primarily used to price things like adjustable-rate mortgages, corporate loans and financial derivatives. This change may have been technical in nature and largely seamless to consumers, but SOFR is one of those highly technical financial concepts that is worth understanding. After all, it may determine how much it costs you to borrow from a bank, and it can influence how much banks pay on deposits. Plus, it can be an early indicator of banking sector health. So let’s break it all down.

Less drama, more transparency

Unlike LIBOR, which was based on bank estimates, SOFR is grounded in actual transactions to the tune of $1T-$2T in daily repo (overnight repurchase) market activity. SOFR is published daily by the Federal Reserve Bank of New York, and it measures the cost of borrowing cash in the repo market using US Treasury securities as collateral. Thus, SOFR is more reliable and harder to manipulate as compared to LIBOR, which suffered a high-profile scandal involving a few global banks. It’s worth reiterating that SOFR is secured by US Treasury collateral and thus considered nearly risk-free, and it’s a volume-weighted median of all overnight repo transactions.

What, exactly, moves SOFR?

- The biggest driver is Fed policy. When the Fed raises or lowers its fed funds target rate, SOFR typically moves in close alignment because both reflect the cost of short-term dollar funding.

- Since SOFR is based on repo collateralized by Treasuries, the market supply and demand dynamics can move rates. Heavy Treasury issuance can push repo rates (and thus SOFR) higher, while strong demand for Treasuries for collateral can pull it lower.

- Money market liquidity is also an influencer of rates. When cash is abundant in the financial system — for example, after quantitative easing — overnight funding tends to be cheap, and SOFR remains low. During tighter money conditions, often driven by seasonality at quarter- or year-ends when banks pull back lending, SOFR can spike.

- Inflation expectations are also reflected in SOFR trends. Higher inflation typically leads to the Fed tightening policy, which pushes the index higher over time. Falling inflation expectations tend to have the opposite effect.

- During periods of market stress or elevated volatility, risk appetite declines, and we usually see a higher demand for safe-haven liquid assets, like Treasuries. This can create unusual near-term moves in both the repo market and SOFR.

- Finally, the Fed uses tools like the Overnight Reserve Repo Facility and Interest on Reserves Balances to help keep SOFR within a target range. Changes to either of these rates directly affect where SOFR trades.

In short, SOFR is essentially a real-time indicator of short-term dollar funding conditions, heavily influenced by Fed policy but also sensitive to market liquidity, Treasury supply and market stress. In normal times, SOFR and repo yields range just a few basis points below the fed funds rate because supply and demand in the repo market are equal. In those atypical times when SOFR is above the fed funds rate, market participants tend to take notice.

SOFR > fed funds rate

Today, SOFR remains slightly elevated primarily due to tight liquidity in the overnight repo market, which is driven by heavy Treasury issuance, the Fed’s ongoing balance sheet reduction (also known as quantitative tightening) and high demand for cash to fund dealer inventories. When cash is scarce relative to Treasury collateral, repo rates rise and push SOFR up. Other market drivers can be Treasury debt settlements and corporate tax payments. If they coincide, we expect to see large amounts of cash being pulled from the financial system and deposited into the Treasury’s account at the Fed, which will then reduce the overall supply of reserves available to lend. The combined effect of these flows means that banks and primary dealers will need an immediate influx of cash to meet their settlement and payment obligations. This will elevate their demand for secured overnight funding, thus pressuring SOFR higher.

This situation clearly shows the impact of tight money market conditions on the secured funding rate, confirming that structural events and periodic cash drains are indeed potent drivers of SOFR volatility. However, we do not think this represents severe tightening of liquidity or mounting pressure in US funding markets. Rather, this dynamic is likely temporary, and we think it demonstrates a healthy ability for the market to self-correct.

Credit vista: Banking regulatory radar

Edward Lee, CFA, Senior Credit Analyst

Nearly three years have passed since the banking turmoil of 2023, which saw the collapses of several large regional banks in the US, as well as the failure of Credit Suisse in Switzerland. To an extent, those events exposed gaps in banking regulatory reforms that have been made since the Global Financial Crisis (GFC), from shortcomings in liquidity risk requirements to the absence of effective US regulations for interest rate risk in the banking book (IRRBB – a measure of risk to a bank’s capital and earnings that could arise from an array of interest rate shock scenarios). The turmoil in 2023 also highlighted other emerging risks, such as the velocity of deposit flight in an era of increasing digitalization.

Perhaps more so, the events served as a reminder that depositor trust and confidence form the bedrock on which every bank must stand, sometimes irrespective of static fundamentals and capital ratios. And while fundamentals are often front and center, the regulatory frameworks in which banks operate also play a central role, not only as a backstop to excessive risk taking, but also as a champion for depositor trust. It is no surprise, then, that rating agencies put significant weight on the strength and effectiveness of regulatory frameworks for their bank rating methodologies. As S&P notes, “strong prudential regulation and effective supervision is fundamental to banks’ credit strength.”1 We agree with this and thus wanted to dig into the regulatory environment to see what might be on the horizon and the possible implications for debt investors.

Regulations matter

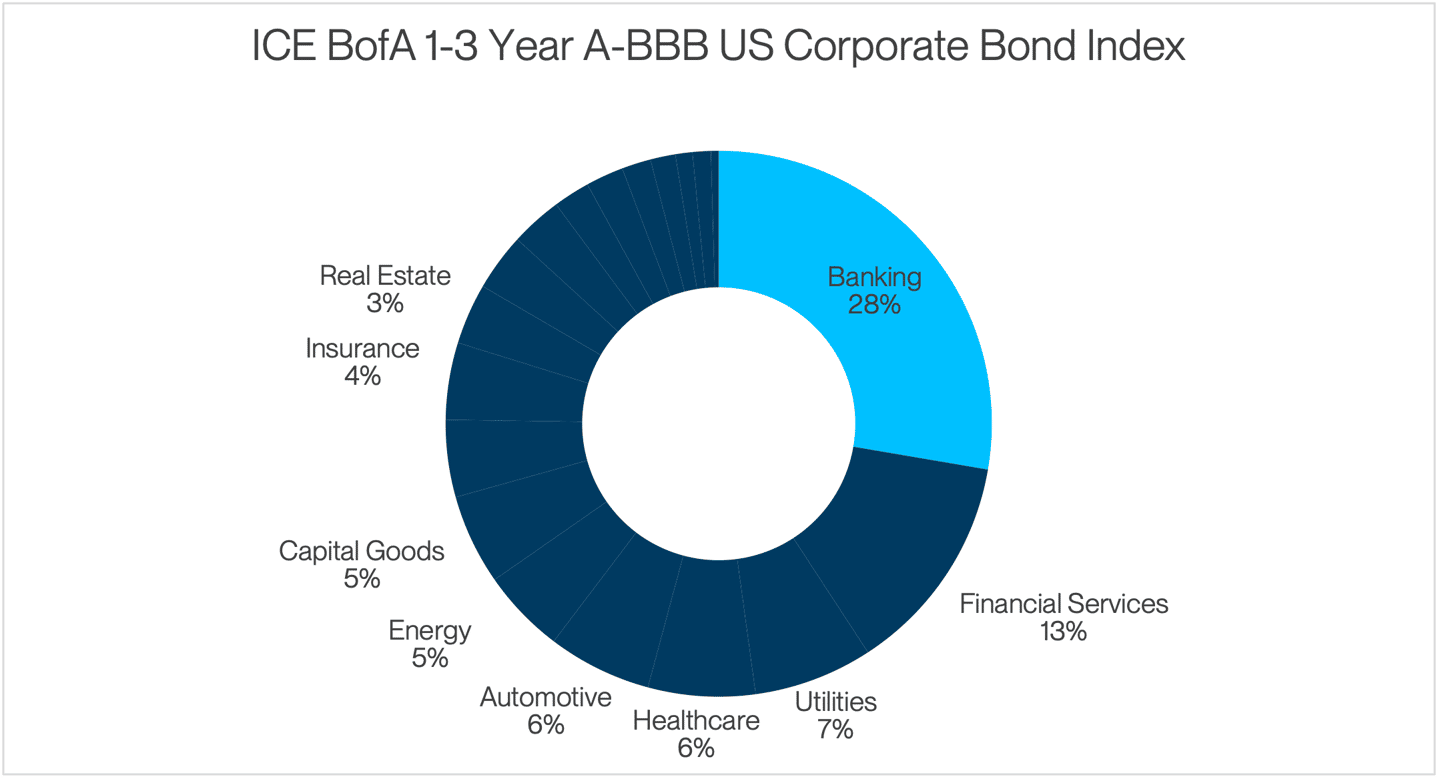

Regulations matter for banks, and banks matter to the overall credit market environment. After all, banks constitute the largest sector weight of US dollar-denominated, broad-sector investment grade corporate bond indexes. Within the Bloomberg US Corporate Bond Index (ticker: LUACTRUU), the standard benchmark for the investment grade corporate bond market, debt securities issued by banks account for ~22% of the total index outstanding. The concentration is even higher for indexes focused on the front end of the corporate credit curve, with banks accounting for 28% of the ICE BofA 1-3 Year A-BBB US Corporate Index. At first glance, this may not seem like an overly large share, but when one considers that the next largest non-financial sector weight is utilities at 7%, the strong relative sway of banks is clear. Large banks dominate the front end with their high regular issuance cadence, driven by regulatory requirements (i.e., total loss-absorbing capacity [TLAC], high-quality liquid assets [HQLA]), as well as the need to fund lending activities at a spread. Yankee banks, particularly those with significant holdings of US dollar-denominated assets and without any meaningful US retail deposit base, account for nearly half the issuance by all banks.

Source: ICE BofA. Data as of 01/20/2026.

Thus, a continuous in-depth understanding of banking regulation should be table stakes for debt investors. Often, changes to regulatory requirements affect bank liquidity, profitability and risk-taking capacity, which can, in turn, affect the perceived safety and yield of their debt instruments. Moreover, changes to capital and liquidity requirements can directly guide the shape and supply of bank issuance, which also influences bank debt yields and spreads. Case in point, regulations that penalize use of short-term wholesale funding, i.e., liquidity coverage ratio (LCR) and net stable funding ratio (NSFR), have driven large banks to substitute short-term funding sources2 with more long-tenor TLAC debt. Proactive monitoring of regulatory trends can help investors anticipate not only potential credit migration or rating actions, but also take advantage of relative changes in supply across the debt stack.

Where are we headed?

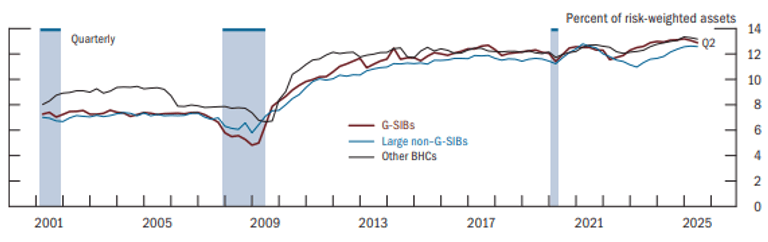

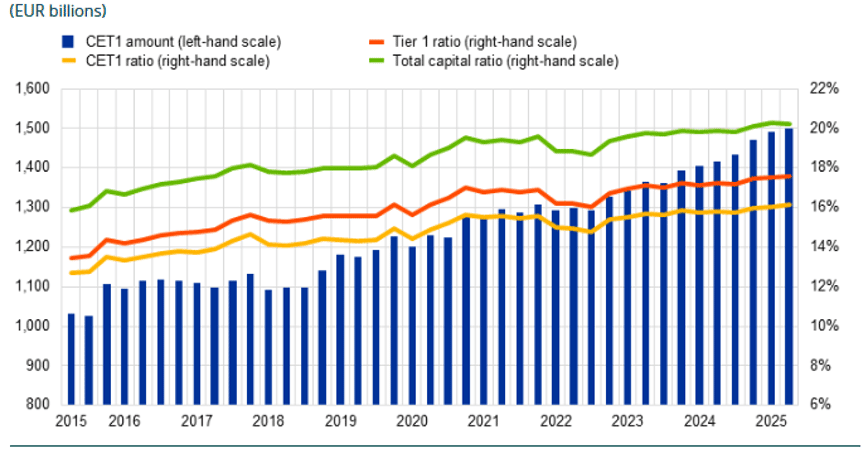

Despite the drag from complexity and additional costs, heightened requirements following the 2008 GFC have largely benefited the credit profiles of global banks. Global banks have seen a considerable reduction in credit risk and estimated loss-given-failure of own debt, largely owing to the abundant issuance of loss-absorbing capital (i.e., both Common Equity Tier 1 [CET1] capital and TLAC debt). The charts below show the steady increase of average risk-based equity capital ratios of large banks in the US and Europe.

Banks' Average Risk-Based Capital Ratios Remained Near Previous Peaks

Source Federal Reserve Board, Form FR Y-9C, Consolidated Financial Statements for Holding Companies. Data as of Q2 2025.

CET1 Amount and Capital Ratios

Source: European Central Bank (ECB). Data as of Q2 2025.

That said, the regulatory pendulum now appears set in the other direction for the major developed markets. Within the US, the tailoring rules of the US Economic Growth, Regulatory Relief and Consumer Protection Act in 2018, as well as incremental changes to capital buffers3 and supervisory requirements in 2025, are examples of targeted easing. Other items in the near-term pipeline include proposals to modify the G-SIB surcharge calculation, proposals to make broad changes4 in stress test and the reintroduction of Basel III Endgame, with the net direction biased toward lower capital requirements. The shifting regulatory environment is not limited to the US. In Europe, a task force formed by the ECB’s Governing Council has published policy recommendations calling for the simplification and reform of existing capital, stress test and supervisory requirements.5 In the UK, the Bank of England recently announced a reduction in capital requirements for major UK banks, starting in 2027.6 Exceptions to this broad regulatory shift are Switzerland, Australia and developed markets in Asia.

Concerns for debt investors?

Given the events of 2023 and the changing regulatory environment, investors are wondering: Should bank creditors be concerned with incremental easing in the US and Europe? We believe the short answer is no — at least, not yet. Rather than any wholesale rollback, the modifications and proposals thus far have been modest, rational and mostly focused on simplification and transparency. Capitalization, whether in the US or Europe, remains a strength, even with lower incremental requirements. Also, it is important to recognize that a shortage of capital was not the driving factor for the bank failures of 2023. Indeed, no reasonable amount of additional equity capital would have been sufficient to absorb all mark-to-market losses, caused by the historically sharp tightening in yield curves in 2022-2023 on every fixed-rate security holding, whether available-for-sale or held-to-maturity designated, and on every fixed-rate loan.

Rather, the more proximate factors were risky funding structures exposed by sudden shifts in the macroeconomic environment and systemic liquidity, ineffective regulation for IRRBB, wrong assumptions about the velocity of uninsured deposit outflows, and ineffective mechanisms to monetize existing liquidity and to use contingent funding sources. In other words, the bank failures of 2023 were a confidence and liquidity crisis first before turning into a solvency crisis. While higher capital requirements promote greater safety and confidence, the benefit holds diminishing marginal utility at higher levels. Every additional unit of capital provides progressively less marginal safety assurance while reducing profitability and capital accretion.

Addressing liquidity risk

Experts from the Bank for International Settlements (BIS) have explored potential policy options for improving the effectiveness of regulatory liquidity requirements and central bank liquidity support. Key areas of focus have included a review of liquidity metrics and stress assumptions; better accounting for extreme, rapid and concentrated deposit outflows (such as those that might be accelerated by social media and digital banking); improvement in operational readiness for HQLA monetization; and better use of credible contingency funding plans.7

While US regulators have yet to formally propose changes to liquidity requirements, various recommendations8 have been discussed, including (1) a requirement for all Fed member banks to pre-position non-HQLA collateral at the Fed discount window to ensure the availability of immediate liquidity during crises and to destigmatize usage of the discount window; (2) the allowance for downward adjustment of the minimum LCR requirement during a stress event so that banks may use HQLA without triggering regulatory scrutiny; (3) exceptions for internal stress tests to diverge from standardized LCR assumptions and be tailored to unique funding and risk profiles; and (4) a reduction of complexity caused by overlapping requirements (e.g., LCR, 30-day internal liquidity stress test and resolution liquidity adequacy and positioning all measure a bank’s ability to survive a 30-day acute liquidity stress scenario). Regulators at the ECB are also rethinking liquidity regulation in an age of faster digital-age bank runs, with a focus on refining the LCR, improving bank operational readiness to draw on central bank facilities, analyzing and mitigating uninsured deposit leverage, and adopting technology for real-time liquidity risk monitoring.

What about interest rate risk?

Currently, the ECB incorporates IRRBB into its “Pillar 2” capital requirements,9 while US regulators supervise IRRBB primarily via supervisory reviews of internal bank policies with neither strict, standardized and binding quantitative limits nor incremental capital requirements for banks with high levels of interest rate risk. Since 2023, there have been various proposals to enhance the supervision of IRRBB by both the BIS and regulators in the US. In July 2024, the Basel Committee on Banking Supervision (BCBS) finalized an adjustment to its standard on IRRBB by revising interest rate shock scenarios, expanding the data time series for calibration and moving from a 99th to a 99.9th percentile value to ensure greater conservatism.10 In October 2025, the Office of the Comptroller of the Currency and the FDIC proposed a new framework to prioritize the supervision of material financial risks, such as interest rate and liquidity risk, over non-financial risks, such as reputational risk.11 In the same month, the Fed released updated principles, focusing on material risks and the overall condition of the firm, thus highlighting the need for better risk management in the banking book.12 However, there is no indication that US regulators intend to implement IRRBB-specific stress tests similar to the ECB or directly incorporate it into additional capital requirements.

Rating agencies have taken the overall regulatory shift in stride, albeit with qualifications. Moody’s has reported that “regulators in some jurisdictions, led by the US, are likely to reduce ‘gold-plating’ of Basel rules and local regulations,” but the “combination of robust capitalization and gradually more proportionate regulation will support both credit strength and shareholder distributions.”13 S&P has noted that “Europe and the US may see a form of regulatory stabilization rather than a significant rollback,” while “broader regulatory rollback, though not the base case today, could have more serious implications for bank ratings.”14 Fitch has commented that the US and Europe are moving to a “pro-growth deregulation agenda” from “prudency primacy,” and suggests that a “more principles-based and lighter-touch regulation combined with lower capital requirements is likely to reduce the resilience of the banking sector to systemic market shocks.”15

In the end…

The crosscurrents of regulatory trends are complex and primed for further changes in 2026. The SVB Asset Management investment team is your partner in keeping abreast of the changes that may affect your cash investment portfolios. The ever-shifting regulatory environment is always on our radar, especially given the prominent role that bank debt plays in investment grade credit markets. While the areas discussed so far have focused mainly on capital and liquidity, other wide-ranging regulatory initiatives with indirect impact to the banking sector have been launched over the past year. This includes legislation aimed at increasing digital asset formation and encouraging de novo banking activity, as well as the reform of the bank merger review processes. Each proposal may have an impact to some extent, though not all appear consequential to the safety and performance of your portfolio. Thus, it pays to have dedicated, seasoned analysts who can sift through the noise, vigilantly peer around corners and provide proactive guidance, whether in calm markets or periods of elevated volatility.

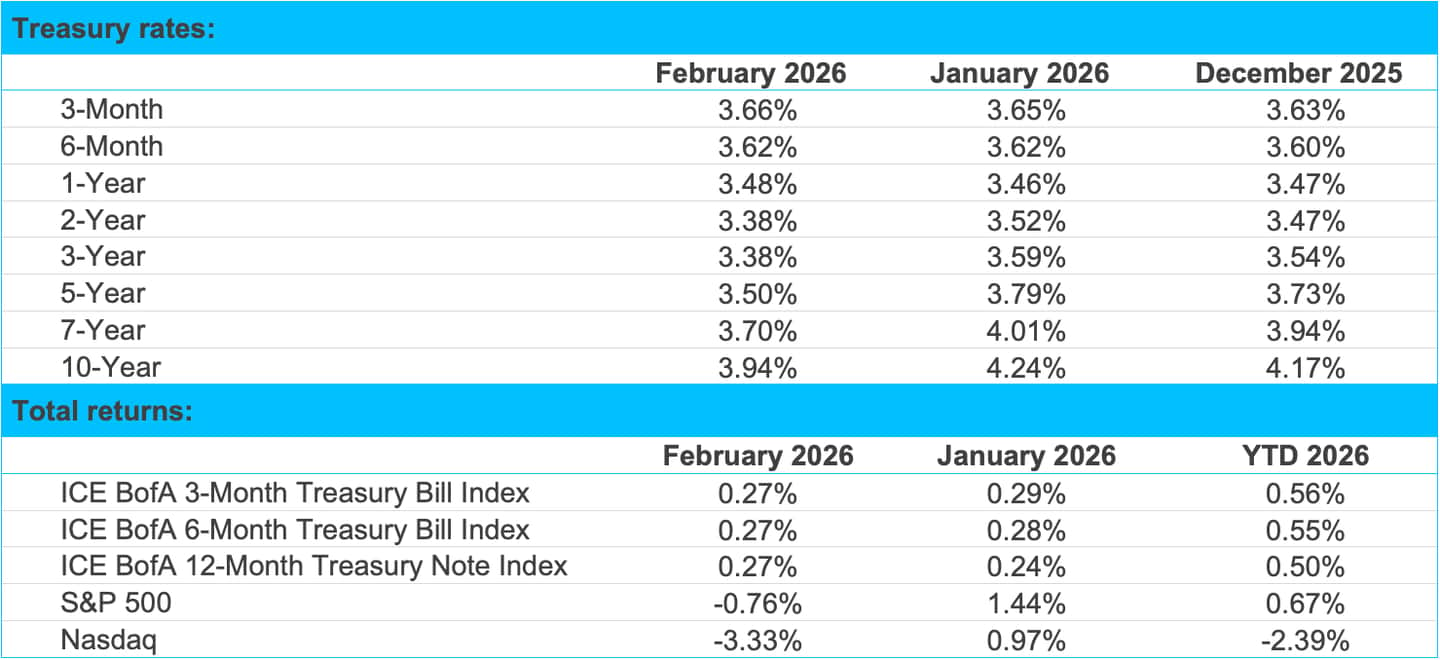

Markets

Source: Bloomberg and SVB Asset Management as of 02/28/2026.

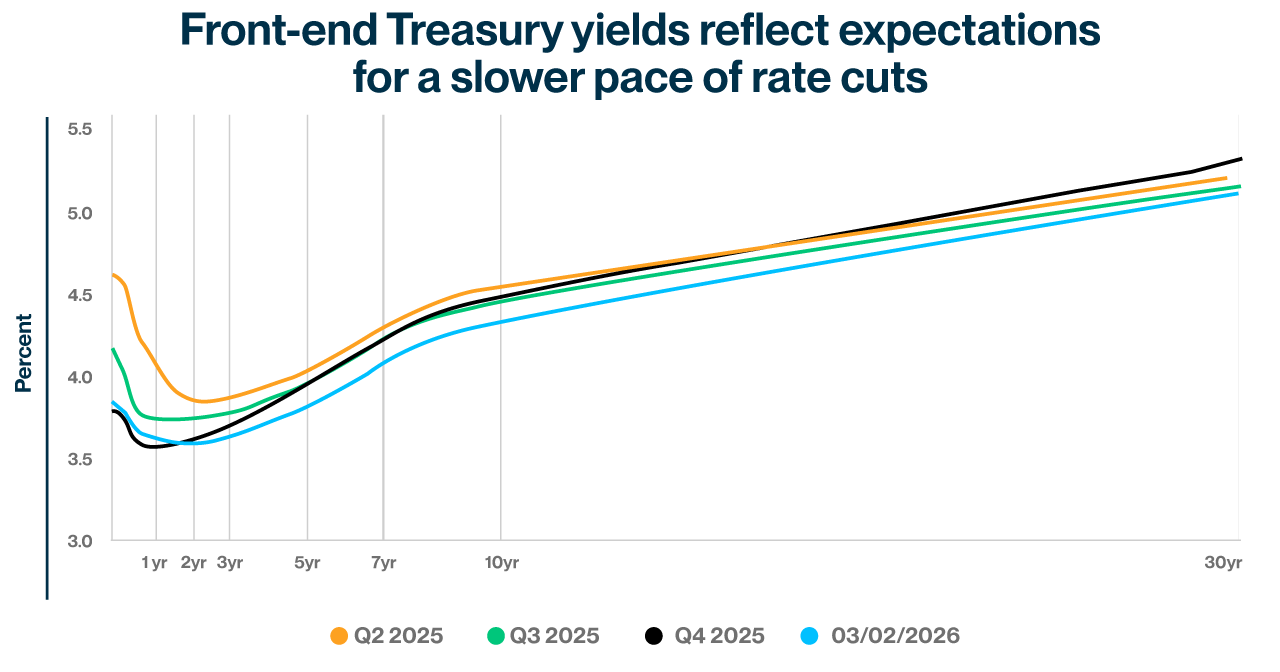

Agency and corporate yields

Source: Bloomberg, Tradeweb and SVB Asset Management as of 03/02/2026.

Source: Bloomberg, Tradeweb and SVB Asset Management as of 03/02/2026.

Economic indicators

Source: Bloomberg and Silicon Valley Bank as of 03/13/2026. US Bureau of Economic Analysis (BEA) and US Bureau of Labor Statistics. *Current GDP release as of 03/13/2026. †QoQ — Quarter-over-Quarter. **Core Personal Consumption Expenditures. ‡Current PCE release as of 03/13/2026.