- The recent Fed pause appears to be prolonging the higher rate environment for now, but the situation is dynamic and there are longer-term implications for managing corporate cash.

- Staying entirely focused on money market funds increases reinvestment risk and opportunity cost, but selectively adding duration may help lock in higher yields and stabilize income.

- Thoughtful cash segmentation allows treasurers to balance liquidity, capital preservation and return as the rate cycle evolves.

Economic vista: Higher for longer? What now?¹

Jose Sevilla, Senior Portfolio Manager

At the Federal Open Market Committee meeting on April 29, the Fed left interest rates unchanged at 3.50%-3.75% for the third consecutive time. At first glance, this decision appears favorable for corporate cash investors: Money market funds and short-term deposit vehicles continue to offer attractive yields, providing meaningful income on idle balances. However, the implications of this pause extend further. A “higher for longer” rate environment that persists in 2026 presents a markedly different set of opportunities — and risks — than what corporate treasurers faced just a few years ago.

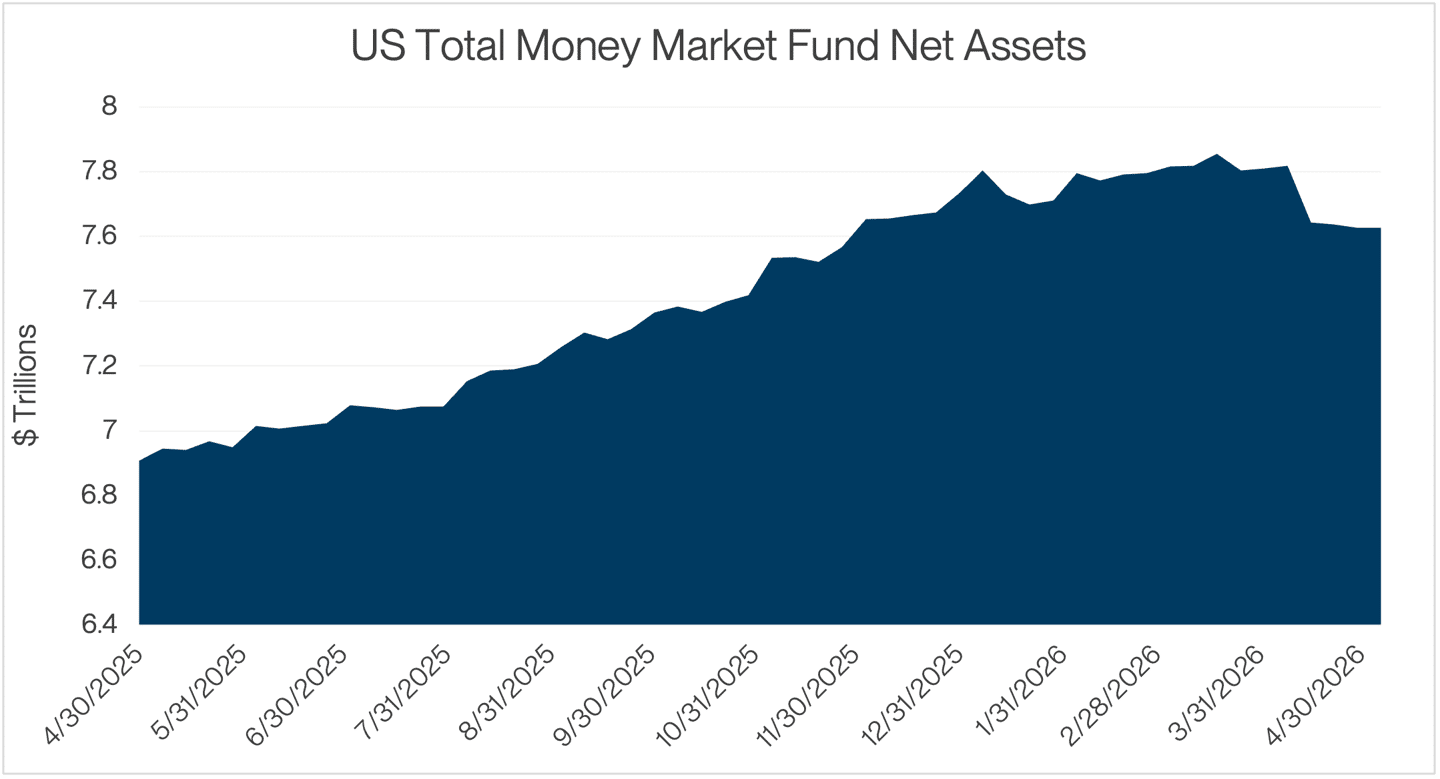

Liquidity across the corporate landscape remains exceptionally strong. Over the past 12 months, money market fund assets have risen to $7.75 trillion, which may reflect a continued preference for safety and flexibility amid persistent economic uncertainty.2

Source: Bloomberg (ICI All Money Market Funds Total Net Assets — WMMFAMTN Index). Data as of 05/06/2026.

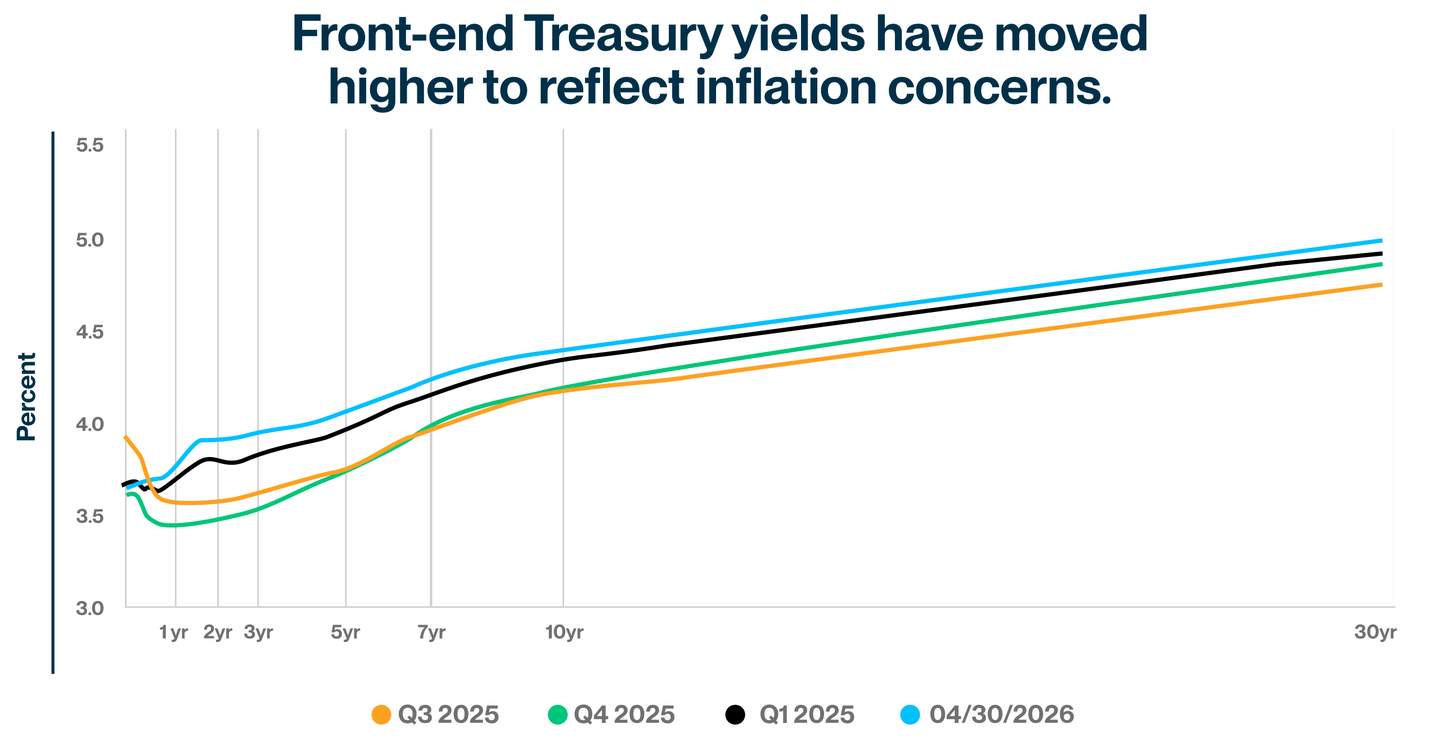

At the same time, the outlook for policy rates has become less predictable. Escalating geopolitical tensions in the Middle East have driven oil prices sharply higher, inflation remains “sticky” and stubbornly above the Fed’s 2% target, and the transition from Jerome Powell to Kevin Warsh as Fed chairman adds another layer of intrigue to the ultimate trajectory of monetary policy. Taken together, the Fed’s pause is beginning to look less like a temporary holding pattern and more like a meaningful opening for purposeful corporate cash management.

Why the Fed pressed pause

The Fed’s decision to delay rate cuts reflects the convergence of several forces shaping the near‑term economic outlook:

- Energy prices and geopolitics: Oil prices have jumped significantly this year, more than 50% through April, propelled by the continuing conflict between the US and Iran. Energy shocks complicate monetary policy because they tend to lift inflation in the short term while restraining growth over time. Higher fuel and transportation costs are likely to pressure corporate margins and curb consumer spending. With these competing dynamics in play, Fed policymakers appear inclined to wait for clearer signals that inflation remains curtailed before adjusting rates lower.

- Inflation remains above target: Given the energy price backdrop, progress on disinflation has slowed. Core personal consumption expenditures (PCE) are currently running around 2.7%, remaining persistently above the Fed’s 2% target. While earlier data suggested inflation was on a steady downward path, energy price pressures and lingering cost increases across services threaten to stall that momentum. In response, the Fed has modestly increased its own inflation projections, strengthening the case for patience rather than easing prematurely.

- Labor market cools but hasn’t cracked: An unemployment rate of 4.3% points to a labor market that is gradually softening but far from showing signs of distress. Hiring momentum has slowed down, and job openings have declined, yet widespread layoffs remain absent. This balanced environment affords policymakers flexibility to stay on hold. A sharper deterioration in job conditions could accelerate rate cuts, while renewed labor market strength could delay them further. For now, market expectations have shifted to no rate cuts in 2026, down from two projected at the start of the year.

Consequences for your cash

For corporate treasurers, a Fed pause is not simply about maintaining higher yields; it brings reinvestment risk and opportunity cost into sharper focus. Government money market funds are currently yielding a one-day average of 3.6%, levels that remain attractive by historical standards, particularly relative to the early 2020s. The Fed’s decision to hold rates steady suggests that these yields should remain anchored in the near term, providing reliable income for operating cash.

However, reinvestment risk is becoming increasingly relevant. Portfolios concentrated entirely in money market funds and short-term deposit vehicles are exposed to this risk. If rate cuts arrive sooner than anticipated, investors may be forced to reinvest idle cash at meaningfully lower yields. A decline of 50-75 basis points (bps) over a six-month period could materially reduce income for strategies that are dependent or overly focused on ultra-short rates.

Concurrently, a higher‑for‑longer rate environment presents a clear opportunity. By selectively allocating portions of total cash within a company’s spending plans to slightly longer‑duration instruments, treasurers can lock in today’s elevated yields, optimize portfolio returns, enhance income visibility and reduce reliance on constant reinvestment — outcomes that may be difficult to achieve by remaining exclusively in money market funds and deposit products.

The opportunity cost is growing

Meanwhile, high-quality short-duration investments — including investment grade corporate bonds, agency securities and commercial paper — are offering yields that exceed money market funds and deposit products. As the rate cycle approaches its eventual inflection point, selectively adding duration and locking in today’s yields can help preserve income that could otherwise erode once policy easing begins. Remaining overly concentrated at the front end of the curve increases the opportunity cost of forgone yield and income stability.

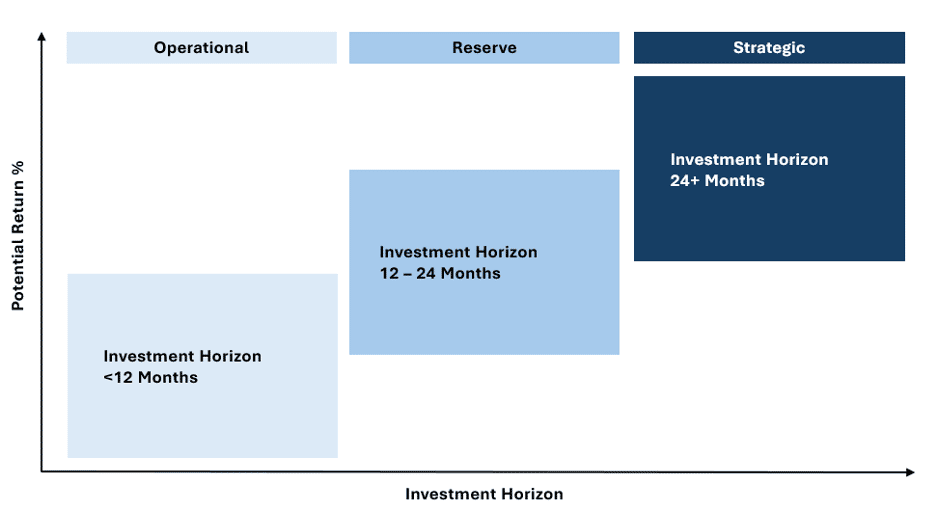

Consider a cash segmentation approach

Source: SVB Asset Management

Ultimately, we believe that effective cash management starts with recognizing that not all cash serves the same purpose. Segmenting liquidity into distinct cash buckets allows each portion of the portfolio to be managed according to its specific function, while maintaining capital preservation as its core principle across all segments. For example, treasurers may want to consider a three-bucket approach along these lines:

- Operational cash (<12 months): Operational cash supports daily obligations, including payroll, vendor payments and near-term debt service. Immediate liquidity is the primary focus.

- Reserve cash (12-24 months): Reserve liquidity provides a buffer for unexpected working‑capital needs. In the current environment, modestly extending maturities within this segment can enhance yield while preserving flexibility and prudent risk controls.

- Strategic cash (>24 months): Strategic cash represents capital unlikely to be needed in the near term. This segment can tolerate additional duration in pursuit of improved risk-adjusted returns.

The Fed pause isn’t permanent

A Fed pause in April does not imply a static environment, and parking all your cash in money market funds is not a viable set-it-and-forget-it strategy. Possible shifts in energy markets, labor data and geopolitics, as well as changes in Fed leadership, could quickly alter the outlook. The current higher-for-longer window presents an opportunity to reassess your portfolio structure, manage reinvestment risk and ensure investment policies allow sufficient flexibility to adapt. The pause offers time but not permanence. In cash management, standing still is always an option, but it’s rarely the optimal response to ever-changing market and economic conditions.

Credit vista: A shifting foundation

Emelynn Abreu, Credit Analyst

A solid foundation for any home is critical to ensure its structural integrity, stability and longevity. One might also say that the bond market provides a similar foundation for the entire housing market. Over the past two decades, we’ve seen both significant and nuanced changes in this foundation, and we continue to monitor the shifts. From our viewpoint, however, the housing bond market still looks to play an important role for income portfolios, even as the market continues to evolve.

A look back

In 2008, during the global financial crisis, the US government placed Fannie Mae and Freddie Mac into conservatorship under the oversight of the Federal Housing Finance Agency (FHFA), after mounting mortgage losses threatened the companies’ solvency and the stability of the housing market. FHFA assumed control of the companies to stabilize operations, preserve their assets and ensure continued support for the US mortgage market. As part of the rescue, the US Treasury entered into Senior Preferred Stock Purchase Agreements with both companies and injected roughly $191 billion of capital into both Fannie Mae and Freddie Mac.3

As a result, since the government’s takeover during the 2008 Great Financial Crisis, Fannie Mae and Freddie Mac debt has been viewed nearly as creditworthy as US Treasury securities, thanks to implicit government guarantees. Credit rating agencies, such as Moody’s and S&P, tie the credit ratings of Fannie and Freddie to that of the US government, given the critical role that Fannie Mae and Freddie Mac’s mortgage-backed securities (MBS) play in the US housing market. Together, Fannie Mae and Freddie Mac own or guarantee more than $7 trillion of mortgage debt or roughly 70% of the US housing market, underscoring its pivotal influence in housing finance, residential and multifamily property values and the broader US economy.4

A look at spreads

Consider the spread between US agency bonds, such as Fannie Mae and Freddie Mac, and US Treasuries. Treasuries are explicitly guaranteed by the full faith and credit of the US government, while Fannie and Freddie debt is supported by an implicit government guarantee. Although investors broadly expect government support in times of stress, as demonstrated during the 2007-2008 financial crisis, investors still demand a credit premium in lieu of the explicit legal guarantee. This component of the spread tends to widen when there is heightened concern about housing policy, political risk or the future status of the government-sponsored enterprises.

Since the start of the second Trump administration, policy makers have expressed a desire to privatize the government-sponsored enterprises (GSE) via an initial public offering. This is not a simple undertaking, and the process involves navigating various complex and untested legal issues. Chief among these is the significant question regarding the existing Senior Preferred Stock held by the Treasury, which is roughly a $323 billion shortfall under current risk-based capital requirements.5 Who might be responsible for this shortfall, and what would be the role of the government following privatization (if any role at all)? Another central question is the fate of that implicit government guarantee. Will it still exist? How might that affect Agency MBS spreads? And ultimately, where would Agency MBS fit in portfolios going forward?

If Agency MBS are no longer considered to be quasi-government securities, investors might demand wider spreads and see liquidity dry up to some degree. Prior to the 2008 Great Financial Crisis and before Fannie Mae and Freddie Mac were placed in conservatorship, spreads between US Treasuries and the Agencies widened considerably, by as much as 150 bps at the peak, only to tighten to levels near those of US Treasuries when the federal government took over the companies.

Under privatization, if the government guarantee becomes weaker or disappears altogether, investors would undoubtedly demand more credit compensation and thus wider spreads. In turn, Fannie Mae and Freddie Mac indebtedness would become true corporate credit risk, and pricing might mimic high-grade financials. A survey of MBS investors expects that privatization under the GSE’s current and severely undercapitalized levels could lead to a widening of risk premiums by as much as 45 bps or more.6 However, some analysts estimate that in a scenario where the GSEs retain government support and are better capitalized, spreads might widen by a much more modest 10-20 bps versus Treasuries.

Equally as important as the fate of the implicit government guarantee, some argue that spreads would ultimately depend on a broader set of structural considerations in any Fannie Mae and Freddie Mac privatization scenario. These include: the amount of capital held by the GSEs; the preservation of more recently created Uniform Mortgage-Backed Securities (UMBS) and TBA market liquidity; and whether banks, regulators and the Fed continue to treat agency MBS as quasi-sovereign risk assets. These answers could be just as important as the guarantee itself.

We will be closely monitoring how the proposed privatization measures and other changes to the housing bond market affect their risk profile and spreads. Ultimately, that will determine their role in any broader fixed income portfolio.

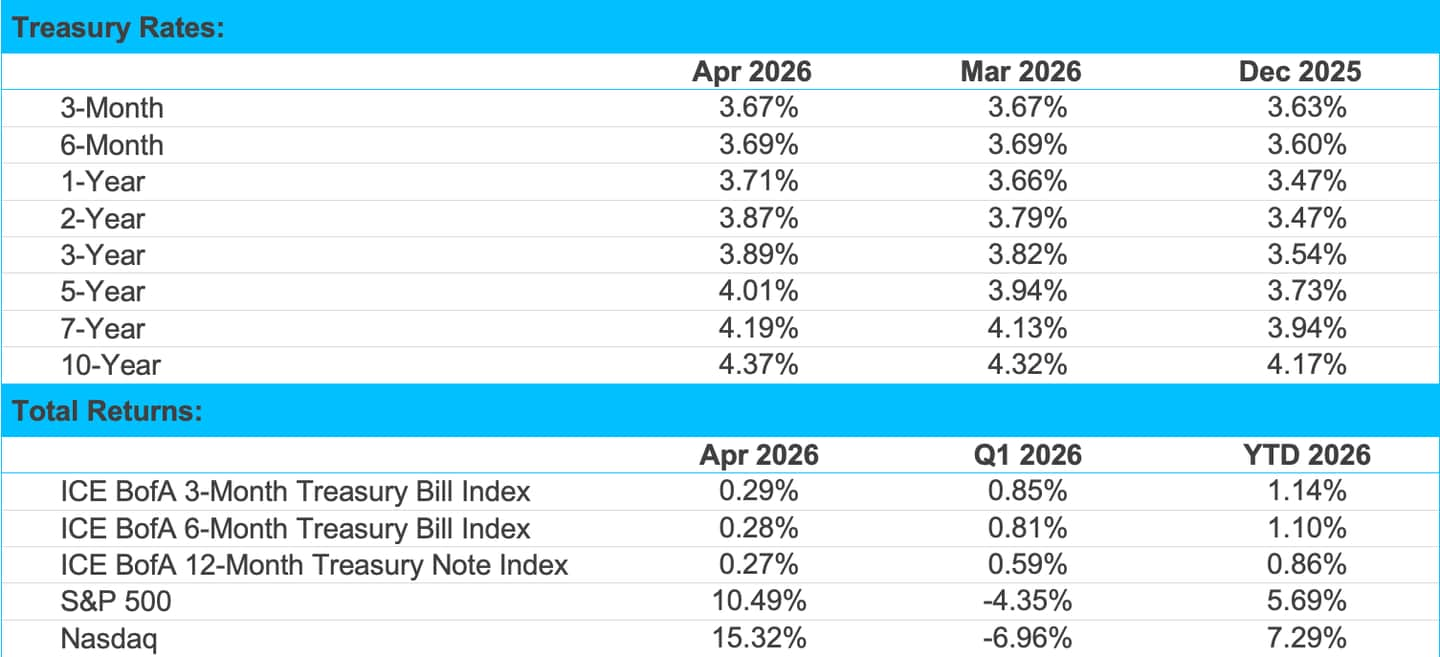

Markets

Source: Bloomberg and SVB Asset Management as of 04/30/2026.

Agency and corporate yields

Source: Bloomberg, Tradeweb and SVB Asset Management as of 04/30/2026.

Source: Bloomberg, Tradeweb and SVB Asset Management as of 04/30/2026.

Economic indicators

Source: Bloomberg and SVB as of 05/12/2026. US Bureau of Economic Analysis and US Bureau of Labor Statistics. *Current GDP release as of 04/30/2026. †Quarter over quarter. ‡Current PCE release as of 04/30/2026.