Key Takeaways

- 2020 saw the largest pandemic in modern times cause the deepest-ever recession and extreme market volatility. Unprecedented fiscal and monetary responses led to a quick rebound and return to financial market stability.

- Last March, the US dollar soared on panic-led demand, only to peak quickly and fall through the remainder of the year and into what we believe is the beginning of a secular decline in its value versus foreign currencies.

- Following the elimination of key uncertainties, investors entered 2021 with cautious optimism. Remedies may trigger further uncertainties however, brought about by critical transitions in Q1 of this year.

Investors are starting 2021 with great optimism following elimination of a long list of uncertainties: development and distribution of a Covid-19 vaccine, a contested US presidential election, a potential “no-deal” EU-UK post-Brexit agreement, EU negotiation of a massive Covid-19 relief fund and 7-year budget, and most recently, critical Senate elections in Georgia.

While we all hope for a return to (some sort of) normalcy, risks remain that could disrupt the health of nations, economies, and financial markets. Among the immediate risks are an escalation in Covid-19 cases and its variants, delays in vaccine production and distribution, fiscal and/or monetary policy mistakes, and the return of inflation.

What happened in 2020

-

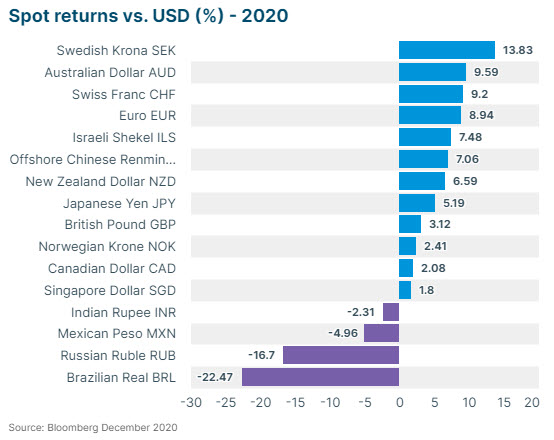

US dollar peaked in March, then reversed and trended lower. A coronavirus-induced market panic in March initially led investors to seek safety in the USD. The rally was short-lived, however, as our currency quickly turned lower and never looked back. By year-end, the US Dollar Index – a measure of the dollar against six peer currencies – fell over 13% from its March high.1 We forecast the dollar to continue trending down through 2021 and into 2022.

-

Investors embraced ‘risk-on’ posture. Despite unprecedented economic damage resulting from Covid-19, 2020 closed with the S&P 500 hitting record highs and credit spreads close to pre-pandemic levels. In fact, prices of all ‘risky’ assets soared. Domestic equities, foreign equities, emerging market bonds, all foreign currencies (including crypto currencies!) and commodities performed well. Investors anticipate central banks and governments will take efforts to continue to expand monetary and fiscal remedies well into an economic recovery.

-

EU-UK reached post-Brexit trade agreement. Approved Christmas eve, the historic agreement will prove to have far-reaching changes, as both sides are forced to adapt to the end of Britain’s 30-year membership in the European single market.

-

EU approved recovery fund and 7-year budget. After the leaders of Poland and Hungary initially blocked the EU’s recovery fund and 7-year budget, EU members finally found a compromise. This paves the way for a €1.8 trillion financial support package: disbursements from the €750 recovery fund begin mid-2021 through 2023.2

-

EU-China investment agreement reached. Seven years in the making, the deal will help redress what Europe views as having been an imbalance in economic ties. Even so, the agreement is considered a diplomatic win for China, even as China had regional disagreements and disputes with more than one country in Asia.

What’s at play

Several critical transitions early in 2021 could bring a new set of uncertainties to financial markets.

-

Georgia election results – Investor sentiment was super-charged following Democratic wins of two Senate seats in Georgia last week. A Biden presidency with Democrat-control of both houses of Congress means investors may see additional, faster-paced fiscal stimulus.

-

The Biden presidency – The president-elect has announced his intention to quickly enact new policies to address the Covid-19 pandemic, wobbly economy, and massive unemployment. Despite the Democratic “blue wave,” wide-ranging legislative changes will not be easy, given the party’s razor-thin margin in the Senate and reduced majority in the House.

-

Pandemic ‘second (and third) waves’ – The global spike in new cases and the emergence of at least two more contagious variants of the coronavirus means many populations face even tighter lockdowns – with concomitant social and economic damage.

-

Covid-19 vaccine production/distribution – Investors have been willing to look past poor economic data thanks to encouraging vaccine news, however continued delays in distribution and additional adverse events could lead to increased market volatility.

-

Brexit – New trading terms between the UK and Europe mark the biggest shake-up in the UK’s political, economic, and foreign relations standing in half a century. In fact, the FTSE 100 Index was the worst performing G-10 equity market last year.3 As a result, UK stocks are relatively cheap, and its all-important financial sector (London) will likely benefit from global recovery and higher interest rates, and an increase in demand for the UK pound.

-

Rising US Treasury yields – Coming off extraordinary lows, the benchmark 10-year Treasury yield jumped over 1% for the first time since March 2020.4 Some analysts are forecasting a further move to 1.25%-1.50% by year-end. Such an increase would cause pain for many EM Latin American and African countries with large US-denominated debt.

-

Dollar positioning – Currency speculators are already positioned well short the USD,5 while large global money managers have only just begun to move out of US assets and the dollar. We agree with the consensus view that the dollar will decline in value over the long-term. In the short-term however – during Q1, and maybe into Q2 ‒ we may see less of a directional bias and more volatility. While volatility increases currency risk, it also offers opportunities, particularly to those firms that actively manage currency exposures.

" Last March, the US dollar soared on panic-led demand, only to peak quickly and fall through the remainder of the year and into what we believe is the beginning of a secular decline in its value versus foreign currencies. "

What’s Next in 2021

-

Cautious optimism. The outlook for financial markets in 2021 is best described as ‘cautiously optimistic.’ The consensus view is that the year will see further accommodative monetary and fiscal support, leading to a strong early-cycle economic recovery, with a rotation toward relatively cheaper ‘value stocks,’ foreign assets and their currencies.

-

US dollar in secular decline. Secular trends are not seasonal or cyclical but remain consistent over time. Following the US presidential election and distribution of a Covid-19 vaccine, demand for the dollar as a safe-haven asset has stalled. Additional factors may further reduce demand for the dollar this year:

-

The dollar should weaken with a global economic recovery given its counter-cyclical tendency (the dollar typically gains during global downturns and declines in recoveries). Commodity currencies including the AUD, NZD, and CAD, should benefit.

-

The Fed is more aggressive than other central banks in expanding its balance sheet (QE), planning to pump $120 billion a month into the financial system until the economy is near full employment.6

-

Popular technical trading strategies turned bearish the dollar in 2020 and may continue. Momentum trading – a strategy in which traders sell (buy) a currency that is declining (rising) – is now well-entrenched with the falling dollar; and cycle-based strategies suggest that the current dollar downtrend could continue for several years.

-

Cheap currency hedging costs for foreign investors – with the US yield curve steepening, large foreign investors in US Treasuries can now earn an even greater return by hedging away currency exposure (selling dollars forward).

-

-

Emerging market stocks and currencies in demand. The global economic recovery should favor EM stocks and currencies, in particular those countries with a rare combination of factors including: 1) a current-account surplus; 2) relatively high interest rates; 3) low government budget debt loads; and 4) an undervalued currency. Leading the list of countries/territories satisfying these factors are Singapore (SGD), the Czech Republic (CZK), Mexico (MXN), Brazil (BRL), Taiwan (TWD), China (CNY) and India (INR).7 China’s early departure from Covid-19 lockdowns and its aggressive stimulus measures will benefit China’s economy and currency, as well as those of its Asian trading partners.

-

Fourth election in two years for Israel. In late December, Prime Minister Netanyahu forced the government’s collapse, refusing a new budget that would accommodate coalition partner demands. The upcoming election on March 23 will take place while Netanyahu is on trial for corruption and amid a devastated economy struggling under the weight of the world’s health crisis.8 Fortunately, politics typically has little impact on Israel’s economy nor the value of the shekel, which continues as one of the strongest currencies in the world.

-

Rising inflation. Investors are increasingly wary of an inflation flare-up—possible if the Democratic “blue wave” leads to massive reflationary fiscal spending. More worrisome, central banks will be reluctant to raise rates since the tactic may destabilize the economy in a financial system with an unprecedented level of debt. The idea that inflation is not going anywhere has become entrenched, so markets are complacent. For now.

Please reach out to your SVB Currency Advisor for a deeper discussion about FX, what impact it may have on your firm, and ways to mitigate risk.