Key Takeaways

- The dollar is rebounding strongly since January 1 as uncertainty around the coronavirus and its impact on global trade support safe-haven currencies.

- Challenges for the euro continue underscored by soft eurozone data and difficult Brexit negotiations to come.

- The Federal Reserve signals a willingness to refrain from raising rates - even if inflation picks up - highlighting a bias toward lower interest rates for longer periods.

Recent US victories on trade (the signing of the USMCA and phase one of the US-China trade agreement) were quickly overshadowed by global concerns over an evolving pandemic and its impact on world economies. Through it all, US assets continued to see strong demand from overseas investors and the dollar continued a positive trajectory begun last October.

What happened?

Phase one US-China Trade agreement signed. After months of negotiations, phase one of a multi-phase trade agreement between the US and China was officially signed, signaling the beginning of a de-escalation in the conflict. Even so, US tariffs on $360B of Chinese goods remain, pending the outcome of phase two negotiations planned this year. Progress on the agreement has given investors reason for optimism. Indeed, as of the day phase one was signed, FX markets had already priced-in an improvement in trade, with the renminbi trending stronger since mid-December.

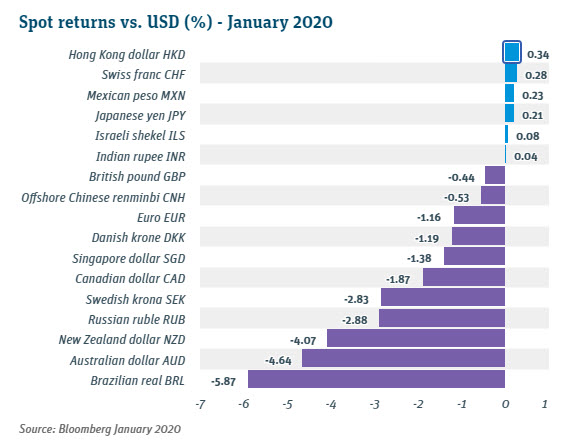

Brexit ratified. On January 23 the UK Parliament ratified the agreement that governs the United Kingdom’s withdrawal from the European Union, and on January 29 the European Parliament consented to the withdrawal. The pound was expected to appreciate following the announcements, but by the end of January fell instead, by almost 2%. The decline could be the result of investor concerns that Britain’s relationship with the EU could worsen as the UK and EU negotiate a new trade agreement due December 31, 2020. (Some are skeptical about the likelihood of meeting this deadline given that the UK’s agreement with Canada took 7 years to pass). FX markets are bearish against the pound.

Dollar remained strong through impeachment trial. President Trump has been acquitted of the two charges brought in the Senate impeachment trial. Interestingly, during the proceedings and prior to his acquittal, the dollar remained strong. Indeed, after the senate vote to proceed without further witnesses, the dollar lifted. Since the acquittal, stocks have climbed to record highs and the dollar continues to strengthen.

The Fed held rates. The Federal Reserve held interest rates steady after January’s Federal Open Market Committee meeting (FOMC), signaling confidence in the rate’s appropriateness given current economic conditions. Some investors and analysts anticipate the Fed will further cut rates during the year leading the US dollar to weaken in 2020.

What's in play?

Coronavirus. Today, the novel Coronavirus has spread to 25 countries. As China seeks to contain the virus, global supply chains are being interrupted and models show China’s first-quarter GDP growth may decline. However, as economists model the potential impact on the global economy, many project a quick rebound in growth once the virus is contained. Still, containment efforts by China are shaking markets, with decreased demand in commodities significantly impacting the price of copper and oil. As a result, the Canadian dollar fell 2% in January and the Australian dollar hit its weakest levels since 2009. The Chinese renminbi weakened to just above 7 RMB/USD – an important psychological inflection point in FX markets.

US-Europe trade agreements. Despite mixed economic conclusions, Trump touted the efficacy of tariffs during his State of the Union address, celebrating an energetic equity market place with very strong year-over-year performance. Indications are the President may revisit in-force trade agreements with EU members, with a focus on German autos and a digital tax likely to be negotiated this year. Anticipation of a potential trade war between the US and EU countries dragged the euro versus the US dollar by 1.75% in January.

US presidential election. As caucuses and primaries begin for this year’s presidential bid, news of the debacle in Iowa fueled a risk-on posture for stocks, with US equity markets jumping almost 2%. In fact, it appears that news that supports the re-election of the incumbent positively effects equity markets. (Expectations are the current administration, if reelected, will continue favorable business initiatives including lower taxes, increased fiscal stimulation, and positive US trade arrangements). Dollar performance remains mixed as Trump pressures the Fed to further relax monetary policy.

What's next?

Central banks may abandon negative rates. Some central bank members have a clear bias for additional monetary easing, even though others now consider protracted periods of negative interest rates potentially disadvantageous. European Central Bank President, Christine Lagarde, pressed EU countries, especially those who enjoy a fiscal surplus (such as Germany and the Netherlands), to increase fiscal spending as a preferred tool to stimulate economic growth. Analysts anticipate further spending by EU members could strengthen the euro 10%-15% in 2020.

A weakening USD. Financial markets are pricing in containment of the coronavirus and a rebound in global trade. Coupled with the expectation that central banks will provide excess liquidity forecasts call for strong emerging markets. As such, investors can expect the dollar to weaken and emerging market currencies which previously suffered from trade wars and central bank uncertainty, to strengthen. The dollar may lose ground, as safe-haven assets become less desirable.

Commodity prices decline. Commodity prices are considered a leading economic indicator as they portend demand for oil, copper and other industrial inputs. The Bloomberg commodity index fell to its lowest point since Q1, 2016, driven by the price of oil which today is off 20% from early January levels. Most economists do not see a strong rebound in commodity prices in 2020 even if global trade stabilizes and central banks keep interest rates low. Currencies associated with commodity exports like the Australian dollar and Brazilian real, already at historically weak levels, will continue to fight an uphill battle.