- The recent launch of military actions in Iran rattled financial markets, boosted volatility and caused a spike in oil prices. Now, investors are trying to handicap the short- and long-term impact of this geopolitical turmoil.

- We believe that prior oil-price shocks can provide valuable clues — not necessarily definitive answers — regarding the path of monetary policy, inflation and economic growth.

- Although the situation remains murky, in general, we see the Federal Reserve acting cautiously, a nominal long-term inflation impact (assuming prices don’t stay higher for longer) and variable paths for economic growth with a slight bias to the downside.

Economic vista: New oil-price shock, old story

Steve Johnson, CFA, Senior Portfolio Manager

Unfortunately, financial markets have seen this story before. Turmoil in the Middle East and a subsequent spike in oil prices are not exactly new territory. Every so often, it seems that geopolitical unrest in this dominant oil-producing region bubbles up and spooks investors. That’s exactly what’s happening now. With the war in Iran rattling markets, we think it’s worth stepping back to consider what history might tell us about the role of oil-price shocks with regard to monetary policy, inflation and economic growth in the United States.

A quick accounting of the last four oil-price shocks (1990-1991, 2002-2003, 2007-2008 and 2022) shows us that history does, in fact, rhyme. Here are three learnings:

The Fed acts cautiously

In the face of geopolitical turmoil and resulting oil-price shocks, the Fed tends to slow down or pause what may have otherwise been its policy bias prior to these events. For example, in 1990, Iraq invaded Kuwait, causing oil prices per barrel to roughly double from below $20 to almost $40 within months. The US entered the war in January 1991, by which time most of the spike in oil prices had reversed. At the first Fed meeting following the outbreak of the war, then New York Fed President Corrigan noted that “prior to the Iraqi developments, I would have leaned to easing. ... I also think it’s so uncertain that it could easily go the other way. I could easily envision unpleasant circumstances where we might have to tighten monetary policy.”

In 2002-2003, oil prices again spiked during the US-Iraqi war, and this was met with similar Fed policy inaction. In January 2003, then Fed Chair Alan Greenspan said, “The bottom line to all of this is that the military uncertainty is so overwhelming with respect to the question of potential monetary policy actions that the less we do, even in how we phrase our post-meeting statement, the better off we are.”

Although the culprit wasn’t geopolitical tensions, oil prices rose nearly 82% from August 2007 to June 2008 in the run-up to the collapse of Lehman Brothers in September 2008.1 A mix of rising demand from emerging market economies and stagnant production was largely responsible. In this episode, we see that the Fed was again biased to pause amid uncertainty, as it signaled its desire to do so in April 2008. Lehman’s collapse in September 2008 and the subsequent financial market turmoil obviously necessitated an end to inaction, with the Fed moving its policy rate to the effective lower bound until 2015.

And finally, in 2022, inflation was moving significantly higher while growth was strong and labor markets were tight on the back of the COVID-19-era stimulus. The Federal Open Market Committee (FOMC) was set to begin a hiking cycle with a 50-basis-point (bps) rate increase in March 2022. However, with Russia’s invasion of Ukraine and uncertainty around the war, the FOMC began with a more modest 25-bps increase. The FOMC minutes later stated, “Many participants noted that they would have preferred a 50-bps increase. However, in light of greater near-term uncertainty, a 25-bps increase would be appropriate at this meeting.”2

Mild impact on long-term inflation?

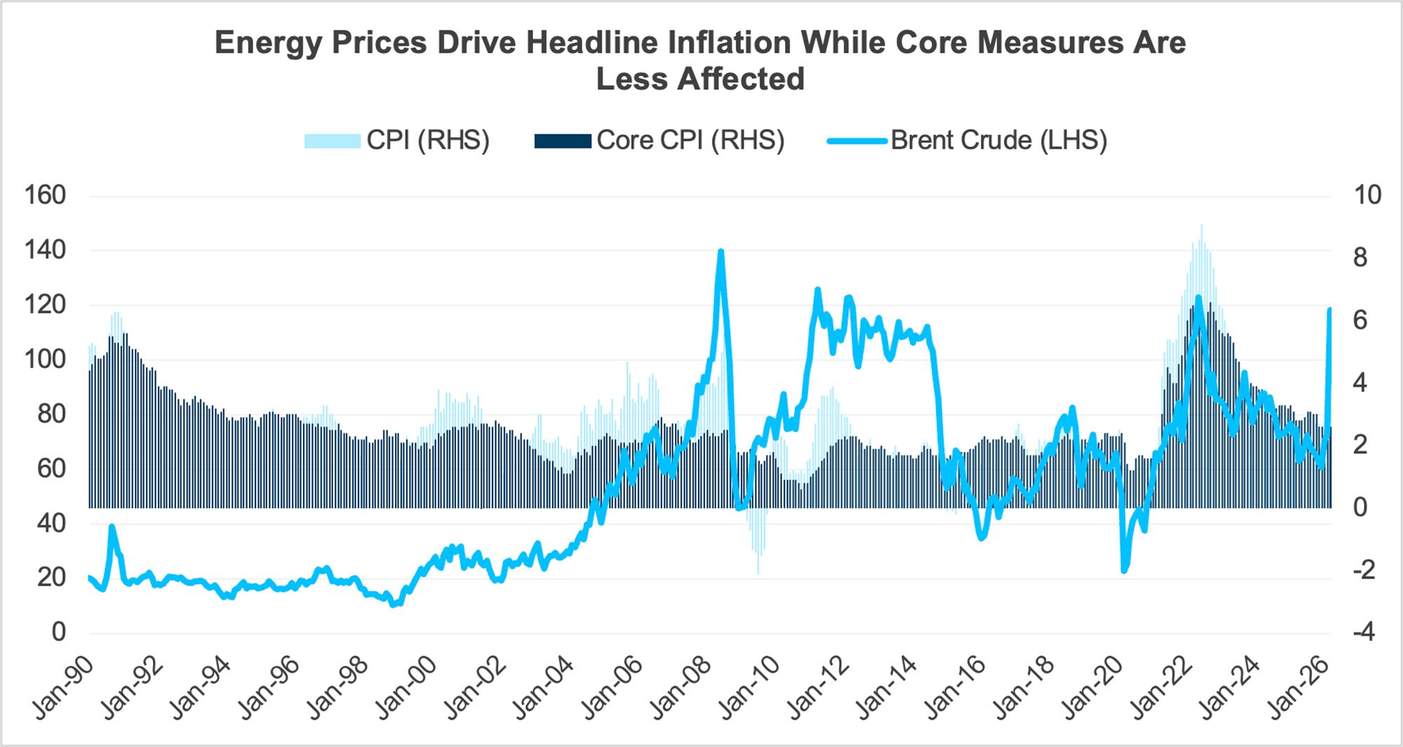

While the Fed initially acts more cautiously with oil-price shocks, the impact on inflation can be a bit trickier to determine. Importantly, a distinction of whether the oil-price shock is demand driven (coincident with stronger global activity) or supply driven (as we currently see with the Iran war) is important. General estimates for a supply-driven oil-price shock show that a ~10% sustained rise in the price of oil would add roughly 35 bps (0.35%) to headline Consumer Price Index (CPI) for three months before fading.3 Headline CPI, which includes both food- and energy-related items, takes on the brunt of the immediate oil-price-shock impact. The core measure of inflation, however, excludes volatile food and energy items. Thus, it would be expected to only increase by three bps (0.03%) before fading.4 To translate this expected impact into today’s context, Brent Crude rose about 63% during the month of March 2026 (from $72/barrel to $118/barrel) before reversing to $95 as of April 14.

Nobody truly knows if higher oil prices will be sustained, but clearly, headline inflation has already been more reflected as seen in the March 2026 CPI figures. Headline CPI increased from 2.4% in February to 3.3% in March, while core CPI increased from 2.5% in February to just 2.6% in March.

But it’s not all bad news. Some good news on the inflation front comes from the longer-term view, as illustrated in the above graph. In most previous oil-price shocks, inflation was not notably higher two years after the oil-price spike, as the price of oil typically reverses somewhat quickly. The lesson learned is that the sustained impact on inflation (not just the immediate impact) relies on whether the oil-price shock endures or is quickly reversed.6

Variable impact on growth

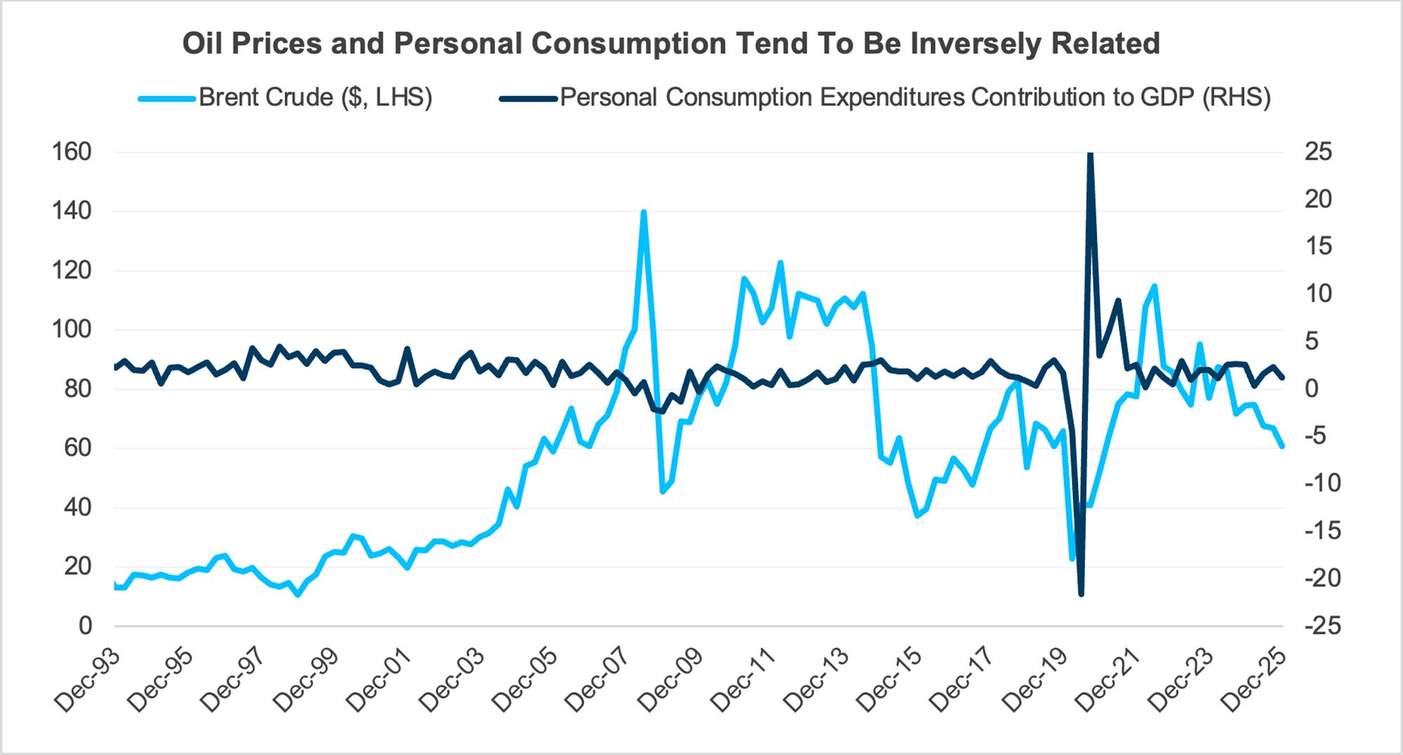

The research on the impact of oil-price shocks on economic growth also suggests multiple potential outcomes. The varied nature of the results stems from the multifaceted impact on the components of GDP. On the one hand, consumers face the brunt of an increase in energy prices (largely gasoline prices), which is clearly a negative for personal consumption (accounting for over two-thirds of GDP).7 Energy-intensive industries may also experience a drag, and defense spending may increase. On the other hand, energy producers see higher profits and may potentially increase investment, offsetting to some extent any consumer-driven decline in growth. All things considered, the research suggests that a 10% rise in the price of oil has a 15-bps to 20-bps (0.15% to 0.20%) negative impact on GDP.8

Source: Bloomberg. Data as of 04/14/2026.

Where to from here?

While there is little clarity on how long the Iran war will continue, history suggests that the Fed will likely err on the side of a cautious approach. Thus, those cheering for near-term rate cuts may be disappointed. On the other hand, history also suggests that the longer-term inflationary impacts may be short-lived if the price of oil reverses fairly soon. In fact, the impact may be less than feared for core measures of inflation. In terms of growth, that’s harder to forecast, but we believe it will likely be impacted negatively by lower personal consumption. Of course, nothing is certain, and time will tell if history is a credible guide for this latest chapter of oil-price shock.

Trading vista: The shoe drops⁹

Jason Graveley, Senior Manager, Fixed Income Trading

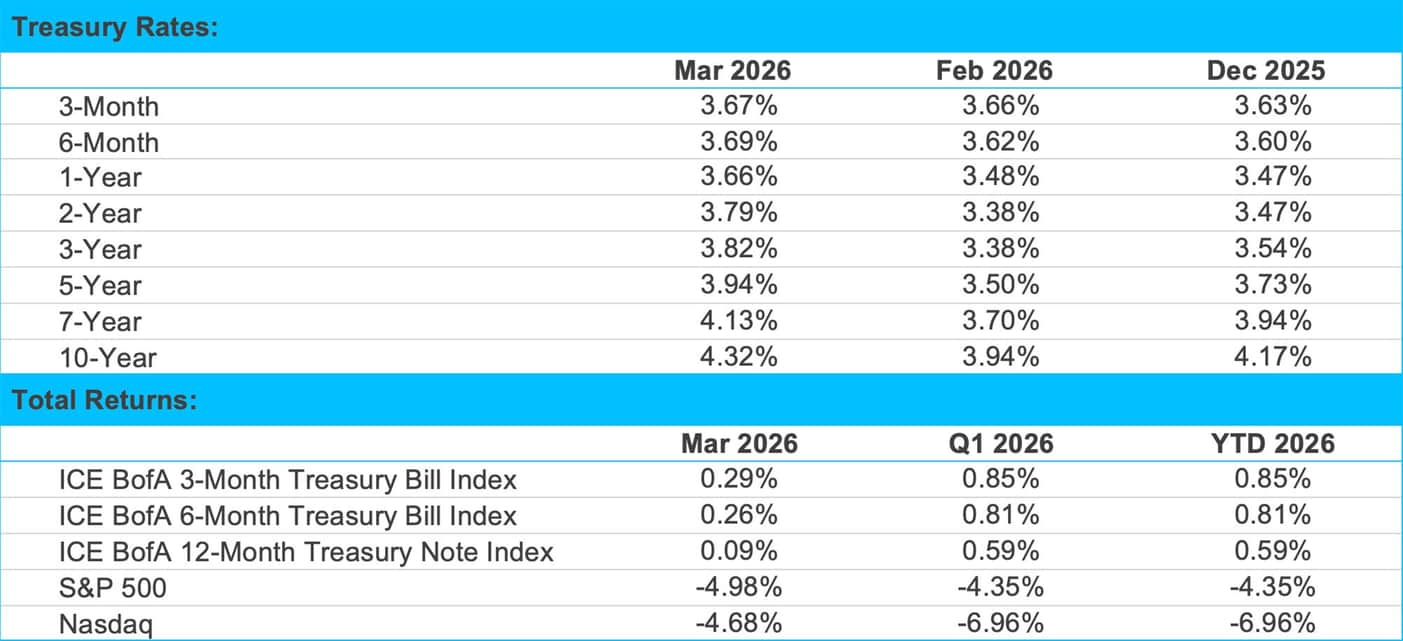

Through most of last year, markets seemed like they were waiting for the proverbial other shoe to drop. Benchmark yields ground materially lower from over 4.35%, while credit spreads tightened to some of their lowest levels on record. Bonds felt comparatively rich, yet all-in yields remained attractive enough to keep investors interested. Buying demand across the fixed income markets persisted as a 3.5% to 4% return was attractive on a historical basis.

In this environment, primary markets had one of their best years on record, as issuers looked to take advantage of the robust demand and attractive pricing dynamics. The chatter among most investors and traders was similar, and the status quo endured. Things were tight, but what exactly was the catalyst that might shift the calculus? Could it be inflation, payrolls or maybe the Fed? The data settled into a range, and many seemed to think that one surprise economic point would likely be balanced by the next. Oil was hovering around $60 per barrel, and the consensus was for two additional rate cuts with little conviction around the timing. It seemed like markets were drifting with a touch of complacency.

But it’s always calm before the storm. In late February, when the US launched new military actions in Iran, geopolitical turmoil took center stage, and the markets had their new catalyst. Since then, we have seen a large upswing in volatility, and there has not been a safe-haven bid for Treasuries. Rather, yields surged with the two-year Treasury note moving from a low of 3.37% to a YTD high of 3.98% within a month. Traders scaled back rate-cut expectations, fearing that a prolonged conflict could result in sustained high oil and energy prices, which in turn would fuel higher inflation.

At the time of this writing, oil was fluctuating on the news flow but still hovering around $100 per barrel. Gas prices, which tend to go up like a rocket and down like a feather, settled above $4 per gallon nationally. Thus, it’s no surprise that the latest inflation print accelerated to 3.3% year-over-year, reflecting more than 10% and 20% gains in energy prices and gasoline, respectively.

Meanwhile, spreads have moved wider — in some cases, more than doubling at their peak on short-duration offerings. The ICE BofA US Bond Market Option Volatility Estimate (MOVE) Index also reached its highest level in about a year this past March. The MOVE Index is a leading indicator of fixed income market volatility, further illustrating how quickly sentiment turned after the start of the conflict.

So where do we go from here? It all hinges on the outlook for Middle East peace and stability. The narrative keeps changing. Moments of de-escalation seem to be followed by new aggressions. However, markets generally appear to be handicapping a swift resolution to the conflict, though it’s far from a certainty. But as long as the market remains rattled, bouts of fixed income volatility are to be expected. All-in yields have settled into 3.9% to 4.5% for front-end paper, and with sentiment shifting, yields are likely to stay elevated for the time being amidst a more uncertain forecast. We continue to monitor the situation closely and will aim to focus on fundamentals and security selection to take advantage of any near-term volatility.

Source: Bloomberg and SVB Asset Management as of 03/31/2026.