- President Trump has nominated Kevin Warsh, a former inflation hawk and past critic of the Fed’s crisis-era actions, to be the next Fed Chair.

- The backdrop to Warsh’s nomination has been unusual given how the administration has criticized the current chair. Maintaining independence from politicization is critical for institutional integrity.

- The evolved mindset of Warsh will have a significant impact on monetary policy for years to come.

Economic vista: Focus on the Fed

Jon Schwartz, Senior Portfolio Manager

Nobody said the job was easy. The Federal Reserve (Fed) is tasked with a tricky dual mandate—balancing price stability (i.e., keeping inflation in check) while ensuring the economy is growing to maximize employment. Sometimes those objectives appear contradictory, and guiding monetary policy can be polarizing.

Soon, the Fed will be getting a new leader, and this marks a consequential moment for US monetary policy. It’s a critical job that will have ramifications that reverberate across global financial markets and economies. With that in mind, let’s take a closer look at the nomination of Kevin Warsh to be the next chair of the Fed.

Coming at a time of heightened economic uncertainty, intense political scrutiny of the central bank and simmering debate over the Fed’s role in addressing inflation and growth, Warsh’s selection invites serious discussion about the future of American monetary governance. While markets have understandably focused on potential interest rate paths and asset prices, this nomination also raises broader questions around institutional independence and the direction of the Fed’s framework.

Warsh is not a novice to the Federal Reserve or to the broader contours of monetary policy. A former Fed governor from 2006 to 2011, he played a visible role during the financial crisis and its aftermath, a period that reshaped modern central banking. His critics have labeled him a hawk on inflation (i.e. an official predisposed to prioritize price stability even at the cost of slower growth) and a skeptic of aggressive policy activism. Supporters point to a deep institutional experience and an ability to balance competing pressures. What makes Warsh’s nomination distinctive is not just his résumé, but his policy philosophy and how it has evolved. We’ll be watching how that evolution intersects with current political and economic realities.

A critic of crisis era tools

A defining theme of Warsh’s recent commentary has been his criticism of the prolonged reliance on unconventional monetary tools, such as quantitative easing (QE). While he supported emergency lending and asset purchases during acute downturns (as in the aftermath of the global financial crisis or the pandemic), he has become increasingly outspoken about the risks of maintaining a bloated balance sheet outside crisis conditions. Warsh argues that extended QE programs inflated asset prices, contributed to distorted incentives in credit markets and blurred the line between monetary and fiscal policy.

This is more than technical bookkeeping. The Fed’s balance sheet, which ballooned from around $800 billion before the 2008 global financial crisis to several trillion dollars today, now represents a scale of intervention that some economists argue makes it hard to unwind without disrupting the market. Warsh has suggested that a sustained reduction would improve “price discovery” in markets and help normalize the central bank’s footprint.

However, calls to shrink the balance sheet carry risks on their own. Reducing holdings too quickly could put upward pressure on long-term interest rates, complicate housing finance and tighten financial conditions at a delicate moment in the economic cycle. This illustrates a potential policy trade-off between restoring traditional monetary tools and maintaining market stability.

Warsh’s early reputation as an inflation hawk has softened in recent years. Some critics still worry that he may resist future rate cuts; however, more recent statements suggesting willingness to entertain lower interest rates in the context of broader balance-sheet reductions has tempered that criticism. This recalibration reflects a broader tension in economic policymaking: how to promote growth and affordability while maintaining credibility in inflation control.

Importantly, Warsh has also challenged what we he sees as the Fed’s heavy reliance on lagging economic data. He has advocated for updating the central bank’s toolkit with better real-time indicators and reducing dependence on forward guidance, which is the practice of signaling future policy moves to shape market expectations. These ideas resonate with some analysts who argue that a more forward-looking strategy could help the Fed navigate structural shifts like technological change and shifting labor dynamics.

Fed independence & integrity

The backdrop of Warsh’s nomination has been unusual. For months, the administration has criticized (and even threatened) the incumbent Fed chair Jerome Powell for not cutting rates quickly enough, thus raising concerns about political interference in monetary policy. After all, the Fed’s credibility is based largely on it being an independent institution, not under control of the Executive Branch and insulated from short-term political pressures.

A central critique of other potential Fed chair nominees was that they might be too aligned with the White House’s policy preferences, thereby undermining the Fed’s longstanding independence. Warsh’s supporters, by contrast, argue that his background, including time at the Hoover Institution and in the private markets, equips him to resist overt political pressure while still engaging with economic priorities. Institutional credibility, the belief that a policymaking body will act predictably and transparently, is not merely a technical concern for markets. It underpins confidence in everything from consumer borrowing rates to international financial cooperation. A central bank perceived as beholden to political leadership risks eroding that foundational trust.

Thus, at stake is not just the next interest rate decision, but rather the larger narrative about what the Fed stands for. Does it remain an independent guardian of price stability and employment? Or does it become an instrument of political economic expediency? The answer will shape markets and public confidence alike. In many respects, Warsh represents a calculated risk for policymakers. He offers experience and intellectual heft, qualities that could anchor confidence, yet he also embodies contentious debates over the scope of central banking post-crisis. By attracting both praise and skepticism, his nomination underscores the fault lines in how we view the Fed’s mission: balancing independence with responsiveness, stability with innovation, and orthodoxy with adaptation.

As the Senate considers his confirmation, and as Warsh himself continues to articulate a vision for the Fed, these questions will matter not just to markets and policy makers, but also to everyday Americans. Mortgage rates, credit costs, employment dynamics and inflation expectations are all shaped by the Fed’s framework. How Warsh seeks to reconcile his past views with his present realities will be one of the most important policy debates of the year.

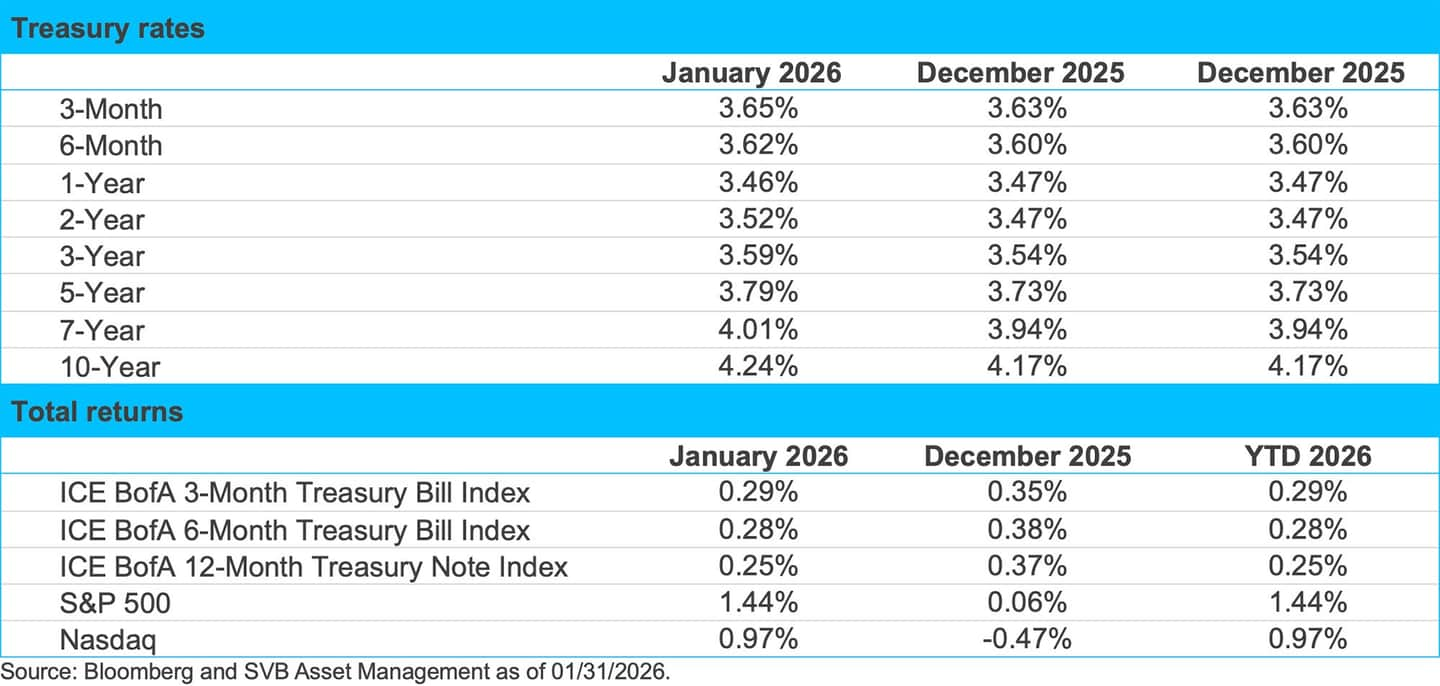

Markets

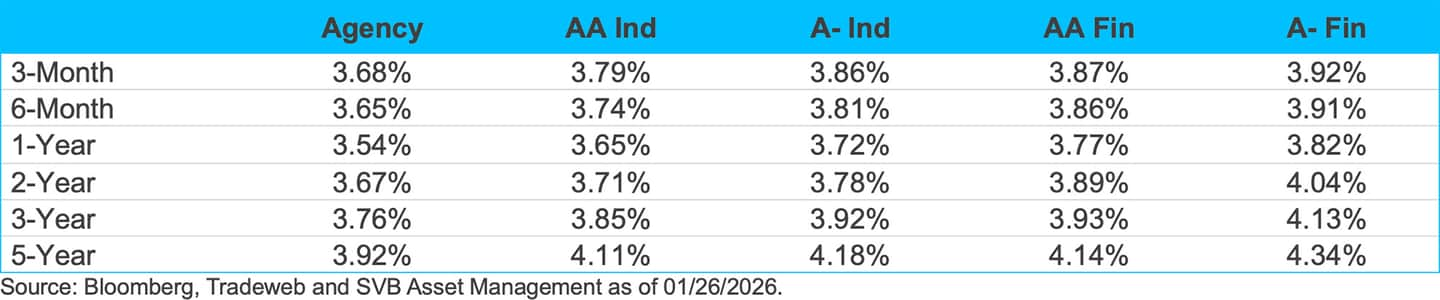

Agency and corporate yields

Source: Bloomberg, Tradeweb and SVB Asset Management as of 01/26/2026.

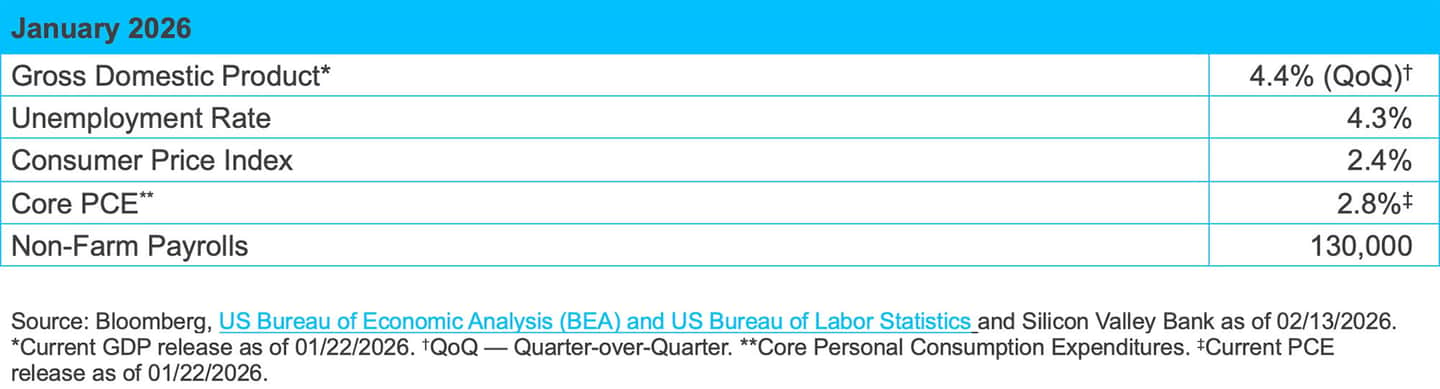

Economic indicators