- Four converging forces — labor shortages, the migration of veteran talent from the autonomous vehicle sector and significant advances in hardware and industry domain knowledge — are creating a 2026 tipping point for widespread adoption of industrial AI in heavy machinery.

- Falling sensor costs and powerful edge compute put autonomy within reach and enable autonomous heavy equipment to make safety decisions in milliseconds.

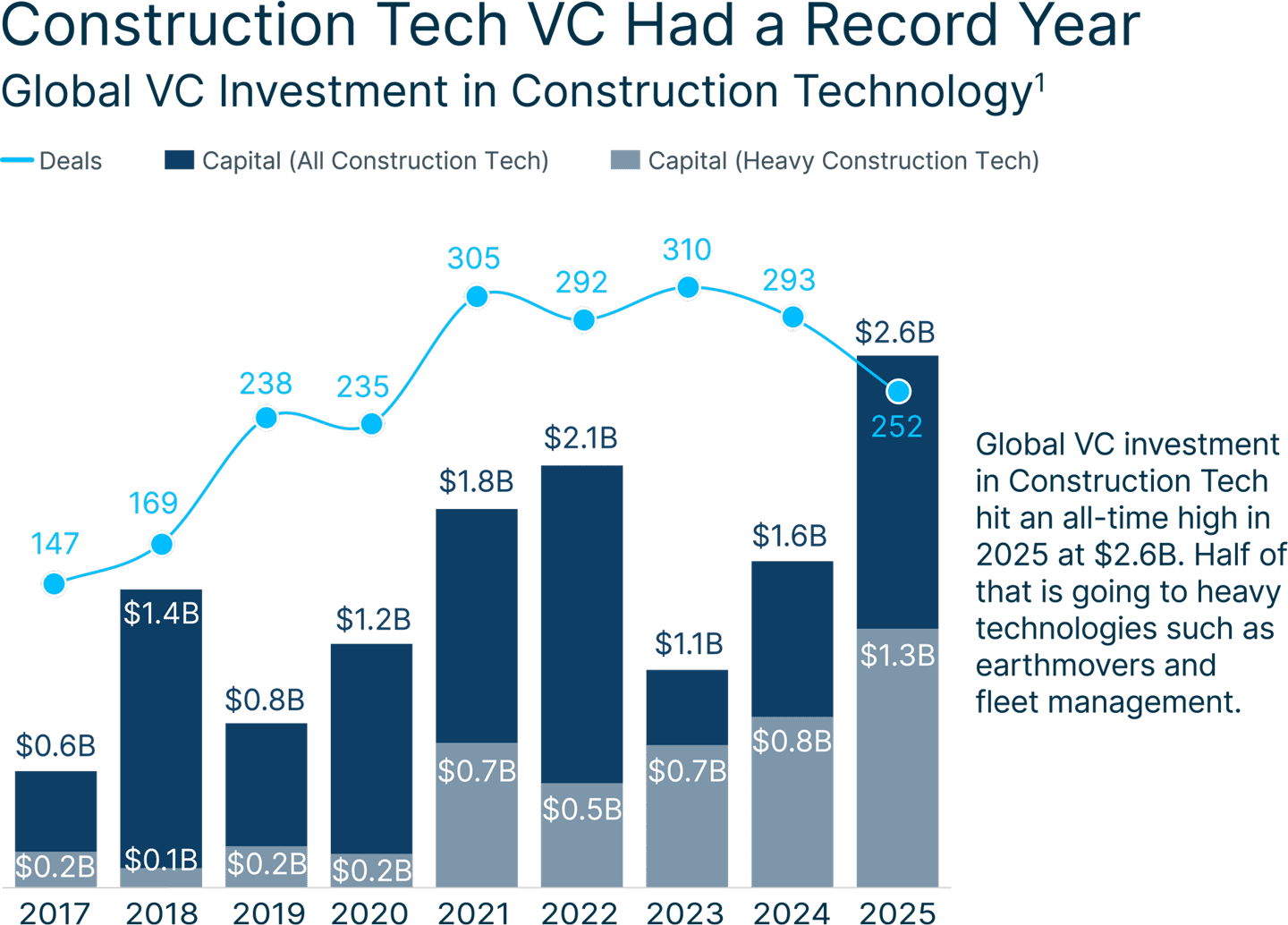

- Record-high VC investment in construction tech surpassed $2.6 billion in 2025 — a 63% year-over-year (YoY) increase — as elite autonomy talent from Waymo, Cruise, Tesla and Boston Dynamics pivots to embodied AI and retrofit platforms for heavy equipment.

AI is moving out of chat interfaces and into the real world. Construction sites, mines, ports and energy fields are becoming a proving ground for new embodied AI models that are changing how heavy industry operates — taking human workers out of machines and placing them in command of robotic fleets of heavy equipment.

The AI models powering chatbots are not suitable for robots in the field. The text to token math works well for office work, but it isn’t reliable enough for the physical world where small errors, or data fabrications known as hallucinations, can have grave consequences. Machines using agentic AI require a physics layer in their computation to account for spatial awareness and the risks of operating in three dimensions. For that, a new generation of companies is answering the call.

This transition is occurring at a moment of need. While heavy equipment operators currently face structural labor shortages and escalating infrastructure demands, advancements in hardware and computing are opening new doors for AI. Breakthroughs in edge compute, sensor economics and real-world machine learning are making autonomy viable in complex physical environments.

At SVB, we bank many of the innovative companies and investors making this vision a reality. This article leverages our vantage point and proprietary insights to dive into the trends that are advancing autonomous machines and heavy equipment now and in the coming years.

Four forces are converging to create a tipping point for industrial AI in 2026:

- A growing labor shortage is accelerating the need to augment human operators.

- The talent that built self-driving cars is shifting toward heavy industry.

- Hardware advancements make physical AI uses more viable.

- Industry domain knowledge is becoming a competitive moat.

1. Let robots do the heavy lifting: Macro factors drive industrial automation

Heavy construction equipment sits in a Goldilocks zone of automatable work. Tasks like bulldozing, earthmoving, lifting and loading are essential enough, dangerous enough, and repetitive enough to make the case for automation intuitive. For much of the last decade, however, that case remained largely academic. While self-driving cars captured public attention, automation of working equipment stayed largely out of view.

Why self-driving cars happened first

The reasons were both technical and economic. The mass market appeal and straightforward sales motion of consumer autos and robotaxis made self-driving cars the logical place for autonomous vehicles (AVs) to start. Cars are relatively inexpensive to buy and retrofit, and city streets — with established traffic rules and fixed features — make for a more structured training environment.

Heavy equipment operates in very different environments.

Earthmovers handle extreme loads, operate under grinding mechanical stress and work on terrain that changes as the machine operates. Job sites lack fixed geometry, making the engineering aspect of autonomy far more challenging. Added to this, the fragmented market comprised of thousands of small companies makes it harder to scale.

AIM Intelligent Machines (AIM) is part of a growing cohort of VC-backed advanced technology companies bringing intelligent machines to the job site. AIM Founder and CEO Adam Sadilek holds a Ph.D. in artificial intelligence and spent a decade at Google’s AI lab working on AI projects, including the self-driving car effort that became Waymo. Before AIM, Sadilek built a physical infrastructure business. It was there, watching heavy equipment sit idle between shifts, waiting on operators, losing productivity, that the need for autonomy became impossible to ignore. AIM was built to solve that gap.

“We focus on earthmoving because our world depends on it — every single molecule our civilization needs comes out of the ground,” says Sadilek. “The complexity of moving amorphous terrain at scale is enormous. For example, unlike self-driving cars, earthmoving machines don’t have the luxury of a provided map because they are constantly changing the very terrain as they operate. The system has to understand not just the environment, but the impact of its own actions.”

That level of technical difficulty, compounded by a fragmented market, kept founder and investor appetite muted for years.

For many, the juice simply wasn’t worth the squeeze — until now. As core technologies like computer vision, simulation and specialized chips have matured, the calculus has shifted.

“Unquestionably, 2025 was the tipping point for heavy equipment autonomy,” said Ty Findley, Co-founder and General Partner of Ironspring Ventures, which invests exclusively in industrial innovation, including AIM. “With a construction labor gap ballooning, paired with the explosion of embodied AI capabilities and associated talent, autonomy is no longer optional. There is a reason CAT’s CEO and CTO were keynoting CES this year discussing autonomous equipment.

![]()

Demand for heavy equipment > Supply of operators

Demand for heavy equipment work is accelerating. Total US construction spending has increased nearly 50% in the last five years, reaching roughly $2.2 trillion in 2025. The increase during those five years was more than the increase during the previous decade. Infrastructure upgrades, a surge in data center construction, energy projects and reshoring initiatives are all contributing to the boom. Manufacturing facilities alone account for 17% of the growth in construction spending over that period, up from 5% in the 2010s.

Notes: 1) Graph shows the change in spending from the baseline of total spending in January 2010. Some categories were combined for interpretation.

Source: US Census Bureau and SVB analysis.

While investment surges, a labor shortage is growing. The construction trade group Associated Builders and Contractors (ABC) estimates that 349,000 more construction workers are needed to meet project demand in 2026 and 456,000 new workers are needed by 2027. Aligned to that shortage, the supply of skilled equipment operators is not keeping pace with demand. Total employment of construction equipment operators increased just 14% from 2019 to 2024 — well behind the growth in spending — even as vacancies mounted. Consulting firm FMI estimates a deficiency rate of roughly 9% for construction equipment operators. That means one in eleven job postings for equipment operators is expected to go unfilled.

Source: US Bureau of Labor Statistics, Bureau of Economic Analysis and SVB analysis.

The safety stakes are equally high. Construction and extraction workers account for 20% of annual workplace deaths in the US, according to the Census Bureau. Construction workers are three times more likely to die in a workplace accident than the average US worker, and natural resources jobs can be much higher. Miners have a fatality rate six times higher than average. Contact-related accidents, which includes heavy equipment mishaps, accounts for about 800 deaths and thousands of injuries per year. Excavators alone rank among the leading causes of fatal accidents in construction.

How industrial AI is augmenting jobs

Automation offers a way to minimize these workplace risks. By shifting skilled workers out of machines and into roles commanding fleets, autonomy can unlock significant productivity gains while reducing exposure to hazardous conditions. From a safe distance, a single operator could oversee a fleet of robotic, mixed fleet earthmovers working simultaneously on a job site that is closed to humans. In an ideal scenario, operators would move into supervisory roles, managing workflows, safety and performance across multiple assets.

In the near term, removing operators from cabs changes the nature of their role but it doesn’t eliminate it, according to AIM’s Sadilek.

“There is such a labor scarcity and at the same time the world demands expanded infrastructure built faster, more natural resources extracted at larger scale and cost effectively,” Sadilek said. “Why would you replace anyone when there are already not enough people in this space to begin with? Keep them in the ecosystem, provide an upward path to them, make them safe, and give them game-changing leverage. When a human fleet manager is running a site with the added power from AIM’s physical AI, they deliver an order of magnitude more output compared to that same person sitting in the cab and manually running a machine.

2. From self-driving cars to bulldozers: Talent and VC shift toward heavy industry

Increasingly, top AI researchers and investors see physical-world applications as the next frontier for artificial intelligence. Recent moves have underscored that shift.

In November, Yann LeCun, Meta’s Chief AI Scientist and a Turing Award winner, announced he was leaving Meta to found a new startup focused on physics-based world models — systems designed to understand and reason about the physical world rather than process text and images alone. Around the same time, Google DeepMind hired former Boston Dynamics CTO Aaron Saunders, reinforcing its vision of Gemini as a platform for embodied intelligence and robotics.

Researchers understand that language models alone are not enough to build robust intelligence in the physical world.

US venture capital investment in construction technology

Venture capital is following that talent. Investors see particular promise in agentic robotics deployed on factory floors, agricultural fields and industrial sites, where the return on automation is immediate and measurable. US venture capital investment in construction-related technologies surpassed $2.6 billion in 2025, a record high and a 63% increase from the prior year.

Notes: 1) Heavy construction includes deals for heavy lifting, earth moving, remote fleet management and related terms.

Source: PitchBook Data, Inc. and SVB analysis.

An influx of talent from companies like Waymo, SpaceX, Cruise and Tesla is bringing a disciplined, iterative approach to industrial autonomy. Many founders in the sector cut their teeth building self-driving cars, where perception, planning and safety-critical systems were refined over years of real-world deployment. Former Waymo lead engineer Boris Sofman founded Bedrock Robotics in 2024 alongside other Waymo alumni. In February, the company raised $260 million to develop technology that retrofits construction equipment to operate robotically.

For companies building autonomous machines, data is often the primary bottleneck. Physical AI systems require vast datasets capturing telemetry, risk and environmental context — data that must be collected through operation, not simulation alone. That process takes time. Nuro, for example, spent nearly a decade running human-driven vehicles in cities like San Francisco and Houston before launching its first large-scale data collection initiative for autonomous systems.

Notes: 1) Index values show trailing 3-month averages except in the max month, which is shown as 100.

Source: Google Search and SVB analysis.

Industrial settings can accelerate this feedback loop. While job sites are more physically challenging environments to map and operate, they tend to be more socially controlled. Unlike city streets, most job sites are fenced-off environments with clear objectives, fewer pedestrians and repeatable workflows. These factors help build data sets around tasks, instead of the endless edge cases that must be patterned for street driving. As deployments scale, the volume and quality of operational data improves, making systems safer and more capable over time.

Autonomy alone, however, is not enough. The next generation of industrial robots must move beyond scripted behavior to reason about unstructured environments. That requires new foundational models of AI designed explicitly for the physical world.

Notes: 1) Includes companies developing foundational models for robots.

Source: PitchBook Data, Inc. and SVB analysis.

FieldAI is one such example, alongside a growing cohort focused on embodied intelligence. Total VC investment in companies developing foundational robotic models reached $4.8 billion over the last four quarters. FieldAI has raised over $500 million to develop embodied AI models. Its systems act as robot brains, guiding machines through three-dimensional environments while managing risk and safety.

“Traditional models and traditional approaches were never designed to manage that risk,” Field AI CEO Ali Agha told TechCrunch.

3. Hardware advancements are making real world AI viable

Even the most robust AI models are only as strong as the hardware that underpins them. Two transformational hardware shifts are proving key to unlocking industrial autonomy.

Commoditized hardware

The first hardware shift is the commoditization of sensors. Over the last several years, the cost of cameras, light detection and ranging (LiDAR), radar cameras and inertial measurement units has fallen sharply, while performance has improved. Early autonomous vehicles in the mid-2010s relied on LiDAR that cost $75K or more. Today, advanced LiDAR systems sell for under $1K. Costs that were once prohibitive have given way to affordable components, making autonomy viable for many more machines.

Components that formerly required custom engineering are now available off the shelf. For example, instead of fitting conventional cameras with custom-made housings to reduce dust and glare, companies can now buy ruggedized cameras that require little to no modification.

As hardware has become cheaper and more modular, it no longer needs to be permanently embedded into machines. It can be easily moved between assets and upgraded over time.

For AIM, this flexibility is important, Sadilek said. The company’s retrofit system fits in a Pelican case, as easily deployable on a fleet of mining earthmovers today as it might be on a fleet of intercity snowplows tomorrow.

“The key is end customer success,” said Sadilek. “The AIM solution doesn’t make any assumptions as to what sensors or compute may or may not already be on the vehicles. The customer has a lot of power and optionality in how to automate their operations in a way that works for them.”

Edge and fog computing

In addition to cheaper parts, the second hardware shift is the rise of edge and fog computing. Heavy machinery cannot depend on cloud-based reasoning alone. Job sites often have unreliable connectivity, and many decisions must be made in milliseconds. New generations of specialized chips make it possible to run planning and safety systems directly on the machine, even in weather-exposed environments.

In edge computing, intelligence is processed by computers on the machine. A bulldozer detecting a large rock in the pathway, a robotic arm sensing and adjusting its reach to avoid an oncoming dump truck — these kinds of actions take split-second decisions that can’t be outsourced to the cloud or a nearby server. Conventional CPUs are too energy-intensive and slow to be reliable for edge computing, but new AI accelerator chips are up to the task. NVIDIA’s Jetson Thor is a gamechanger in this realm, purpose-built for real-time decision-making.

Released in 2025, the Jetson Thor chip can deliver roughly two quadrillion tera floating point operations per second of AI compute. That’s a 7.5x increase in performance over the previous generation of chips released just two years prior. These powerful chips can enable the complex world models needed for embodied AI. Notably, Caterpillar announced in January of this year its collaboration with the NVIDIA Jetson Thor platform to enable real-time, on-site intelligence for its construction, mining and power equipment.

Fog computing is about processing intelligence from a nearby locale that is not on the machine. A typical use case for fog computing might be in a control site that is coordinating across many machines. At the edge, each machine is autonomously coordinating its own actions, but the fog computing system is deciding where assets should deploy for the system as a whole. More powerful on-site AI servers are helping fog nodes run more complex algorithms to optimize their feel operations and output.

Together, these advances are moving intelligence into the equipment itself. The cloud still plays a critical role, but increasingly as a training and fleet-learning layer rather than the brain of the system. Sensors, edge compute and control software now form a tightly integrated autonomy stack, and the companies that master that integration gain a durable advantage.

4. The right tools for the job: Domain knowledge is key in industrial AI

Industrial autonomy is not plug and play software. Deployments require deep, sector-specific knowledge and close integration with how work actually gets done across different interconnected parties.

At CES in January, Caterpillar announced a new lineup of autonomous heavy equipment, including excavators, bulldozers, loaders and haulers, reflecting a broader trend of incumbents embedding autonomy directly into their machines. Caterpillar also demonstrated an in-cab AI-assistant to coach and guide human operators and technicians. Embedding such AI makes a full-conversion to autonomy much easier.

Innovators are taking notice. Unlike enterprise SaaS, which often seeks to disrupt and replace incumbents, industrial AI companies are partnering with original equipment manufacturers (OEM). The heavy equipment industry relies on deeply embedded, often regionally located dealer and distributor networks that serve as the primary interface for customers for everything from the parts and maintenance to digital aftermarket products.

“Far more important than technical capabilities, innovators must deeply understand the incredibly complex nature of the heavy equipment go-to-market value chain and range of critical constituents within it,” Findley of Ironspring Ventures said. “From the OEM, to the equipment dealer/distributor, to the end customer actually breaking ground, all of those parties must be carefully coordinated to deploy autonomy at scale.”

Partnerships with tech providers are proving increasingly common in this space. AIM tends to white label much of their software and work directly with equipment manufacturers and owners. This process involves deploying an AIM team to a client’s site for several weeks to train operators and retrofit machinery.

“We’re a Switzerland of the heavy machinery market. We are partnering across colors of iron, geographical areas, and range from retrofit to OEM integrated solutions,” Sadilek said. “We are only beginning to announce the full gamut of AI fleet deployments and partnerships we have forged over the last four years of commercial operations around the world.”

Successful deployments also require integration with existing workflows — surveying, dispatch, fleet management and jobsite coordination systems that already underpin industrial operations. In this environment, domain-specific platforms consistently outperform general-purpose tools. Autonomy becomes most valuable when it fits into how equipment is scheduled, monitored and maintained.

Source: PitchBook Data, Inc. and SVB analysis.

One example of the opportunity in the space is the construction services company Trimble, which has quietly amassed $2.4 billion in ARR (out of $3.6 billion total revenue) powering many of the software and digital solutions used on construction sites. The flywheel of these connected products — from project management to geospatial tools — represents the kind of integration that embodied AI will need to achieve in order to scale.

As deployments grow, the market is beginning to consolidate. Perception, control and fleet-management software — once developed as separate solutions — are converging into unified platforms. Strategic acquisitions and corporate venture investments are accelerating that convergence, signaling a shift from pilots to production-grade ecosystems.

Looking beyond 2026

The winners in industrial AI will be those that combine human-machine collaboration, edge intelligence, real-world learning and deep domain integration. Progress will not be linear, and challenges around safety, regulation and deployment remain. But the direction is clear: As intelligence moves into machines, heavy industry is becoming one of the most consequential proving grounds for the next era of AI.

Acknowledgements

Special thanks to Ty Findley, Co-founder and General Partner of Ironspring Ventures, for lending his expertise and perspectives in industrial automation during the preparation of this article. His guidance and contributions helped shape and inform the key themes presented here.