Key Takeaways

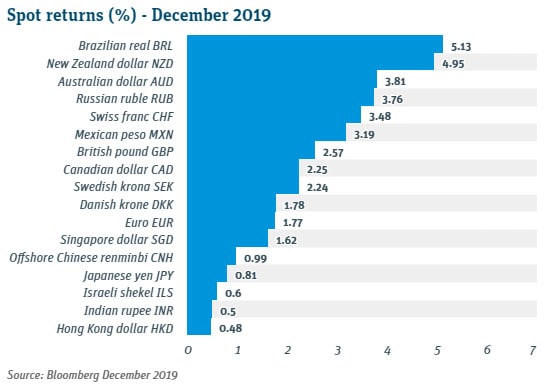

- The new year started with a headache for the dollar. Renewed optimism in the markets coincided with the dollar selling-off against all of its major peers for the second consecutive month.

- Geopolitical tensions are high in the Middle East, bringing a fresh risk of havoc to the markets in the new year.

- With the US Presidential election set for this November, global risks will shift focus to the US, putting pressure on the dollar.

The new year started with a headache for the dollar. Two of 2019’s major risk events passed in mid-December: the UK General Election and Phase 1 of a US-China Trade deal, giving clarity to the markets and increasing investors’ risk appetite. Renewed optimism in the markets coincided with the dollar selling-off against all of its major peers for the second consecutive month.

Geopolitical tensions are high in the Middle East after the US killed Iranian Major General Qassim Suleimani, bringing a fresh risk of havoc to the markets in the new year. With the US Presidential election set for this November, global risks will shift focus to the US, putting pressure on the dollar.

What happened?

The UK will finally leave the EU. Boris Johnson won a snap general election by the largest majority in parliament since Margaret Thatcher in 1987 and now commands a mandate to “get Brexit done.” The United Kingdom is scheduled to officially leave the European Union on January 31, 2020—1317 days since 51.9% of Brits originally voted to leave. The formal post-departure trade deal between the EU and UK is yet to be decided. Although Johnson would like to resolve details by the Dec 31, 2020 deadline, new EU commission president, Ursula von der Leyen, doubts a full resolution can be achieved before 2021. The uncertainty regarding a post-Brexit UK will likely drag the GBP/USD, taking it below 1.30 in in the months ahead. Pending a successful UK/EU agreement, look for the sterling to rally past 1.35, and flirt with pre-referendum highs of above 1.40 by late 2020.

US and China agreed to ‘Phase 1’ of trade deal. Phase 1 of 3 in a trade deal between the US and China includes commitments from China to increase purchases of American goods and services by $200 billion over the next two years, with an emphasis on agricultural products. In exchange, the US agreed to suspend plans for new tariffs on Chinese imports and reduce some existing levies. Chinese Vice Premier Liu He is scheduled to visit the White House on January 15 to sign the agreement, and President Trump has indicated Phase 2 discussions will start “right away.” Markets remain uncertain as to Phase 2 and future implications. The RMB has rallied 13 of the last 15 weeks, now almost entirely erasing losses from the trade war escalation over the summer.

Sweden abandoned negative policy rates: After setting negative interest rates for the past five years, the Riksbank (Sweden’s Central Bank) raised its policy rate 25 bps to 0.00%. Negative interest rates from the central bank is an extreme policy measure to provide support to a struggling economy and was used by 4 countries post-financial crisis. Sweden, Scandinavia’s largest economy, is the first to abandon the policy. With inflation trending below target (now at 2%) and slowing GDP growth, the hike can be seen as a return to more normalized monetary policy to spur growth rather than a conventional rate cut. The krone, the worst performing major currency versus the dollar in 2019 through October, recovered nearly 3% since the Riksbank indicated it would make the move.

What's in play?

Middle East tensions flare following Suleimani killing. Following the death of Iranian Major General Qassim Suleimani from a US drone strike, markets, fearing retaliation from Iran, reacted immediately pushing Brent Crude oil prices up over 6% to more than $70 a barrel. Since then, as tensions lessened, prices have fallen below $65 a barrel. Still, uncertainty surrounds Middle East stability. Following the killing, the Indian rupee and Korean won sold-off with prospects of higher oil prices, while the Japanese yen rallied as investors sought refuge in safe-haven currencies.

Australia’s fires cloud their economic skyline. The already struggling Australian economy could be tested further as tourism declines and business is disrupted following the bushfires that are devastating the country. The recent Australian dollar rally (from post-financial crisis lows) to .70 USD per AUD has all but been given back after dovish hints from the Reserve Bank of Australia (RBA) who is considering a rate cut of as much as 50 bps. If the RBA cuts rates during its Feb 4 meeting, lows of .66 USD per AUD may be in store.

Canada’s loonie falls out of range. Until recently, the Bank of Canada’s (BOC) ‘steady rate policy’ has consistently maintained loonie values in the $1.30 - $1.36 range. In December, the Canadian dollar fell below $1.30 CAD per USD for the first time since October 2018. A pause from the Fed and resurgent commodity prices towards year-end gave the CAD tailwinds pushing it below 1.30. Both the BOC and Fed are expected to keep rates on hold for 2020 with short-term rates nearly identical on both sides of the border. Broad USD weakness could take the pair to 1.25 by EOY.

What's next?

US presidential election. Throughout 2020, the Trump administration’s actions will aim to enhance the likelihood of a second term for the President, including efforts to complete Phase 2 of the China trade deal and continue or promise an expansionary fiscal policy. These measures would broadly contribute to a weaker dollar. On the other hand, democratic rivals’ proposals of expanding the federal government have markets spooked and may bring a bid to the safe haven dollar. Investor uncertainty as to whether the administration will change in November will be a headwind for the dollar during the year.

Taiwan’s rejection of “One country, two systems”. After a year of protests in Hong Kong, President Tsai Ing-Wen, an outspoken supporter of Taiwanese independence from China, was elected to a second term. So far, the Taiwanese economy has benefited from the US-China trade war, as the island nation provides an alternative source for tariff-hobbled Chinese goods. In fact, Tsai’s victory and the escalation of the trade war have propelled the Taiwanese dollar (TWD) to outperform all other emerging markets currencies in the latter half of 2019. Even so, investors remain uncertain as Taiwan continues to resist China’s “one country, two systems” paradigm. Continued confrontation with the mainland could reduce foreign investment and reverse TWD gains.

Emerging markets primed for a rally. With most developed central banks on pause and global growth forecasts slightly exceeding those of 2019, yield-seeking investors are finding emerging markets attractive. A steeper yield curve will provide a tailwind to EM currencies which have underperformed over the last couple years.