Key Takeaways

- The right insurance coverage is critical to your fund’s long-term safety and success.

- Choose an insurance partner you trust to help navigate the complexities of fund coverage.

- Consider consolidating your policies to potentially save on premiums.

Contributed by Kristen Ostro of Strut Consulting.

Note: This article aims to provide emerging managers with a general overview of the various facets of venture capital insurance. It is NOT professional insurance advice, which you should always seek from a licensed insurance advisor.

Starting your own venture capital (VC) fund can be exciting, challenging and incredibly fulfilling. Yet the set-up of every successful business involves some tedium. That’s where insurance comes in. As a new manager, you’ll come to learn your fund has a mix of general and very specific types of required insurance coverage. These requirements are most often dictated by investors and written into the limited partnership agreement (LPA), so you’ll have the facts going into fund formation negotiations.

Addressing your insurance needs may be a painful process, but having adequate coverage is critical to ensuring your firm’s long-term safety and success. Read on to learn about the next three steps to take.

1. Assess your primary risk exposures.

It’s important to find the right balance of coverage — an insurance portfolio that isn’t too lean and that comprehensively addresses your core critical risk areas, which vary based on your stage of growth, structure and assets under management.

Venture funds tend to have the following primary risk exposures:

Portfolio risk - When you invest in a company and take a board seat, you increase your exposure to, and risk for, portfolio-related litigation, such as intellectual property infringement suits.

Operating risk - Growing your fund and adding to your team means an increased risk for employment practices liability, based on issues such as harassment, discrimination, wrongful termination, etc. These types of issues are six times more likely to occur than any cybercrime or data breach, according to Travis Hedge, co-founder of Vouch Insurance. A business insurance platform for startups and investors, Vouch offers discounts to SVB clients. (Note: SVB has invested in Vouch.)*

Limited partner (LP) risk - The act of accepting an LP’s money opens you up to risk as both an investor and the custodian of their cash. The extent of your potential liability depends largely on the individual LP’s characteristics. Major drivers include the size of the LP, the type (institutional, endowment, etc.) and the LP’s experience with venture.

2. Find the right provider.

Insurance providers typically take a comprehensive approach to the coverage they’re trying to sell you, which can often be overkill. That said, you don’t want to be caught without adequate coverage in critical areas. Careful assessment of your current risk levels, your overall appetite toward risk and your budget may help you decide which provider best suits your needs.

Consider choosing a provider you trust to help navigate the complexities of coverage. Evaluate your options based on their customer service, including their client dashboard and the availability of additional client support resources (such as advice on the insurance implications of hiring remote workers during COVID). Also consider the insurance products and related services they offer, such as health insurance, employee benefits and compliance.

One additional consideration: If you’re investing in early-stage companies, they’re likely going to need insurance coverage, too, ranging from a solid directors and officers policy to protections against cybercrime and wire fraud.

It might be worthwhile to choose an insurance partner that can service and give preferred discounts to your portfolio. Typically, there’s no need to shop around for a lower rate, since the majority of insurance firms tend to pitch you to similar providers (including Chubb, Hartford and others). It may be helpful, however, to get a quote from one of the boutique insurance firms that has specialized market access in the VC space as a frame of reference. Ultimately, it’s a best practice to pick the firm you want to work with and stay the course.

Top-tier service providers

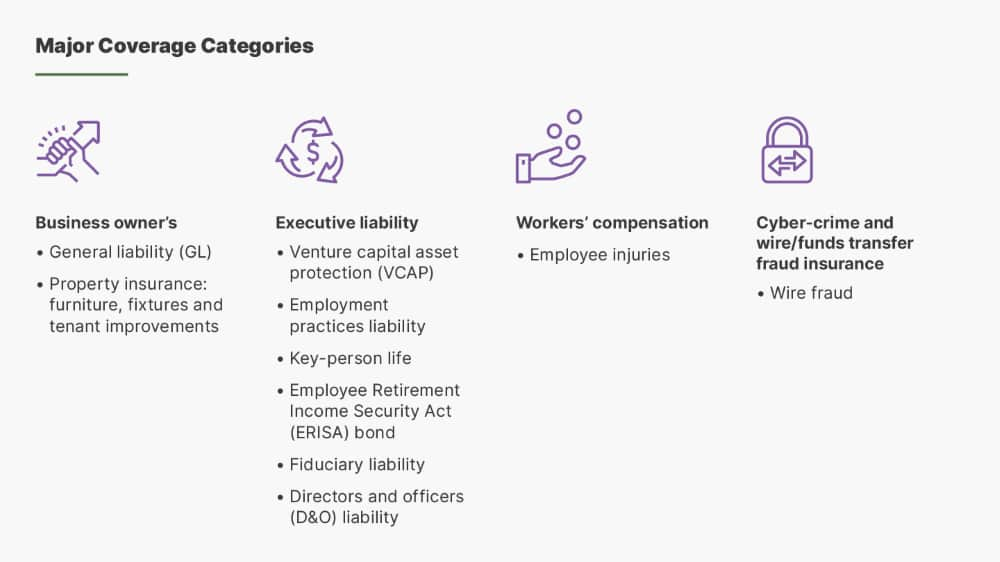

3. Select the right coverage.

As an emerging manager, there are three critical facts you need to know before delving into the details of insurance coverage:

- Some funds can get by on a bare-bones package, while others need top-tier coverage. The “industry standard” may not always match the actual needs of your firm. A basic foundation for venture firms consists of a business owners policy, workers’ compensation and venture capital asset protection (VCAP).

- As you increase your overhead, your insurance costs increase accordingly — so be thoughtful when considering a fancy new office or a new hire.

- You may be able to cut costs by consolidating your policies. Tiered savings usually depend on the coverage and can range from 2% to 15%.

Now for the details. Here’s what you need to know about the basic types of coverage most funds need, along with an estimate of how much they might cost.

General liability and business owner’s

A standard GL policy is a basic requirement for most funds for protection from common lawsuits related to business activities (such as advertising liability), as well as negligence, financial loss and other issues. Annual premiums average $600 to $1,200. Core coverage might include business and personal property limits indicative to cover your core assets:

- $1M occurrence/$2M aggregate GL limits

Common extensions to a business owner’s policy may include:

- $1M occurrence/$2M aggregate employee benefits liability limits

- $1M hired/non-owned auto liability

- A cyber extension/data breach coverage for $10,000 response expense, with a $50,000 defense and liability limit

- Up to $5M umbrella limit

VCAP

VCAP combines management liability, management indemnification, outside directorship and professional services liability. The standard recommendation for VCAP is approximately $1 million of coverage for every $100 million in committed capital. As your assets under management (AUM) increase, so will your premium costs, but getting this insurance early on and building a good track record can help keep your policy costs lower over time. To submit an application, you’ll typically need to include a formal private placement memorandum, annual audit documentation and your investor deck.

Note that VCAP was primarily built for private equity firms, and as a result, it doesn’t always keep pace with the needs of emerging managers. For example, carriers like Chubb often won’t even look at funds under $100 million AUM. What’s more, large funds can pay annual premiums of at least $15,000, which would be crippling for smaller funds.

You can navigate this situation by going with an alternative carrier, such as a specialty insurer like Axis or a regional insurer in your area. Alternatively, you can negotiate VCAP coverage forgiveness, citing factors like strong due diligence and/or requiring insurance at the portfolio level as leverage for your position, according to both Hedge and Benton Keith of Sterling Thompson Company. While VCAP coverage is the most expensive policy you’ll likely need, the upside is that it’s often considered a fund expense.

Sample quote (subject to change with market dynamics):

- $1M limit, $100,000 retention (the amount of money the insured person or business is responsible for in the event of a claim): $13,000 to $15,000

- $2M limit, $100,000 retention: $23,000 to $25,000

- $3M limit, $100,000 retention: $25,000 to $30,000

Employment practices liability (EPL)

EPL covers wrongful acts arising from the employment process and bridges the gap between general liability and D&O liability (more on that below). The most frequent types of claims covered under such policies include wrongful termination, discrimination, sexual harassment and retaliation. Coverage typically provides reimbursement for the costs incurred in defending a lawsuit but does not cover reimbursement for any penalties suffered. While you won’t need EPL until you hire your first employee, you can often consolidate coverage under your VCAP policy to reduce costs. It’s worth noting that employee salary ranges and carry offerings will be factored into your EPL and your insurance carrier may scrutinize your HR policies as part of the evaluation process.

Sample quote:

- $1M limit/$150,000 retention per incident: $1,500

- $2M limit/$250,000 retention per incident: $2,500

- $3M limit/$350,000 retention per incident: $4,000

Key-person life

This coverage, which is typically negotiated in the LPA, protects LPs against the death or disability of a key or irreplaceable partner, executive, fund manager or employee whose loss would irreparably damage the firm’s ability to function. Typical rates start at $1,200 to $2,500 per year, but I’ve seen an allowance of up to $10,000 per partner per year, which can be treated as a fund expense.

ERISA bond

This bond, named for the Employee Retirement Income Security Act of 1974, protects your 401(k) plan against losses caused by acts of fraud or dishonesty and should represent a minimum of 10% of plan assets. A typical ERISA bond from Hartford includes a $20,000 limit of liability with an annual premium of $270. Premium bonds usually start at $1,000 annually per $1 million of coverage.

D&O liability

D&O liability protects the personal assets of the directors and officers (and their spouses) while serving on the board of the startups in which they’ve invested. This coverage protects them if they are personally sued by employees, vendors, competitors, investors, customers or other parties or actual or alleged wrongful acts in managing the company.

Fiduciary liability

This coverage protects the trustee from being held personally responsible for errors and omissions (E&O) in the administration of your employee benefits program as imposed by ERISA. To keep costs down, it’s best to fold this coverage in with your VCAP.

Workers’ compensation

Don’t forget that when you hire your first associate, executive assistant, or operations or platform employee, you’re going to need workers’ comp insurance. It covers injuries suffered by employees in the workplace, including wage replacement and medical costs. In exchange, employees give up the right to sue their employer for negligence. Premiums depend on the number of employees and other factors, but ranges are roughly $700 to $1,500 per year. Unfortunately, workers’ comp cannot be consolidated with VCAP and must be treated as a separate cost. Before signing up for workers’ comp, though, speak to your payroll provider to evaluate your needs.

Cyber-crime and wire/funds transfer fraud insurance

Wire fraud has been on the rise for years, as scammers have gotten smarter and more sophisticated. Since you’re managing millions, it’s wise to protect yourself and your team should someone fall victim to a scam. For example, sub-limited policies of $250,000 to $500,000 in per-incident coverage have premiums of $3,500 to $5,000, according to Jared Wood of HUB International. Limits of $1 million and up would be covered as a part of a crime bond, with annual premiums of roughly $5,000. It should be noted that an internal “bad actor” incident committed by an employee would be covered under your cyber policy, whereas funds transfer fraud would be covered under a crime bond. Depending on your exposure, premiums usually fall in the $1,500 to $5,000 range for $1 million in coverage.

Property insurance

I purposely put property insurance at the bottom of this list because I recommend holding off on getting office space until you absolutely need to (not to mention factoring in COVID). Office buildouts are expensive, and property insurance amounts are determined by a litany of site-specific factors including zip code, square footage, age of the building, landlord/property manager requirements, installed security and safety features, estimated cost of assets held within and others. All these factors can make the whole endeavor quite costly.

Fund insurance: tedious — but important.

If you’re committed to starting a fund, take the time to understand and obtain the insurance you need. Doing so means you’ll be able to protect the fund you’ve labored so passionately to create.

As you get your fund established, reach out to SVB for more resources and support.

Strut is a VC consulting firm focused solely on providing operations, investor relations, and platform/portfolio service support and expertise to fund managers of all sizes. Founded in 2016, Strut aims to help fund managers accomplish more with less, allowing them to succeed at the highest level.

Additional resources for emerging managers:

- Legal, Banking and Fund Administration: Three Critical Elements for New VC Funds

- What You Need to Know About Your Fund Administrator

Access further articles and resources on our Emerging Managers page.