State of the US Wine Industry

2026

Key Takeaways

The US wine industry is navigating a challenging cycle, but not all wineries are experiencing it the same way. A clear divide has emerged between those evolving with the market and those struggling to keep up. These patterns offer a roadmap for navigating slower demand and building toward more resilient growth.

01 The passive growth era is over—performance hinges on behavior, not conditions

Wineries in the top quartile reported 8% sales growth and 11.9% operating income, while the bottom quartile saw a 10.2% sales decline and -10.5% operating margin. These results reflect fundamental differences in how they are repositioning in response to demand.

02 Stabilization is coming—but not for everyone

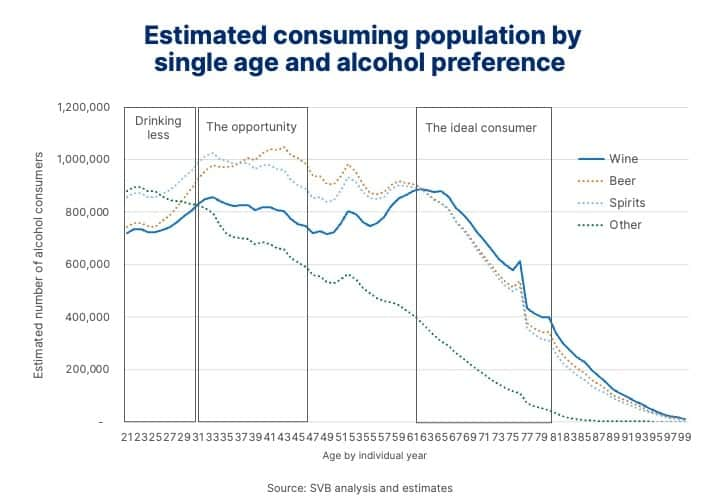

The older, wine-focused cohort is aging out, and younger adults aren’t replacing them at the same rate. Millennial and Gen Z drinkers are spread across more categories and drinking less overall, particularly under age 29.

03 Top performers prioritize the customer and use digital tools to extend that edge

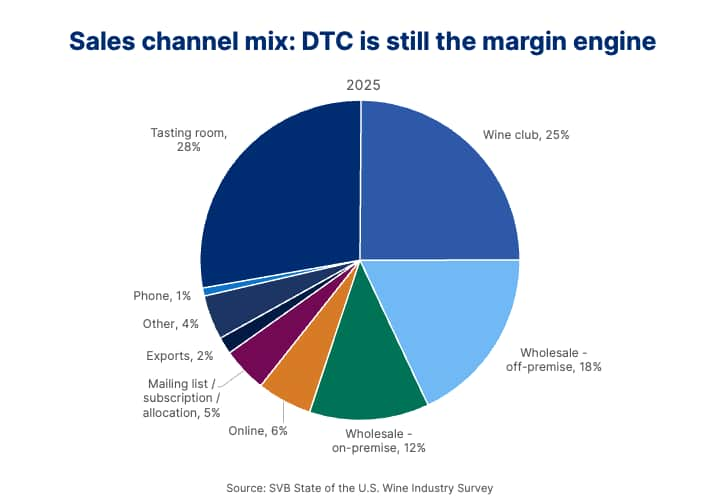

Leading wineries focus on customer alignment and brand clarity, treating direct-to-consumer (DTC) as a loyalty engine, not just a sales channel. Tasting rooms and wine clubs now account for 53% of the average winery’s sales, with some regions relying on DTC for as much as 78% of revenue.

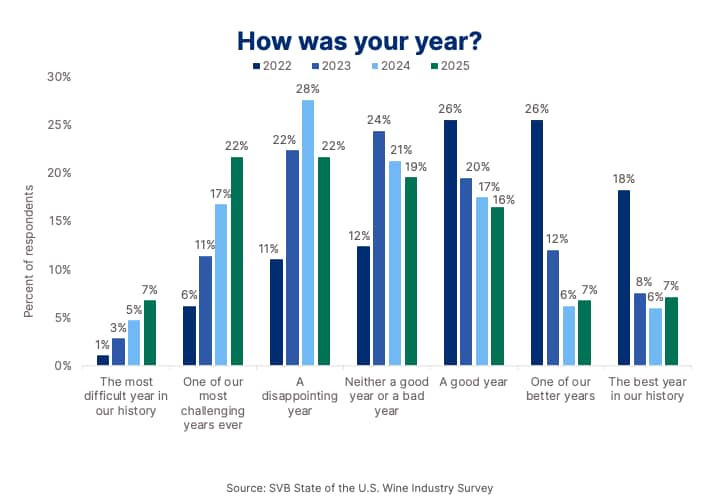

The share of wineries reporting a good year increased

Roughly half of wineries rate 2025 negatively, and about a third rate it positively. However, the share of wineries reporting “one of our better years” or even “the best year in our history” increased slightly.

Consumer patterns are rewriting the demand curve

Younger consumers are engaging with wine on different terms. These expectations influence the way demand shows up across clubs, tasting room activity and online, requiring wineries to rethink messaging.

Top performers treat direct channels as a relationship strategy

The most resilient wineries are shifting from transactional tactics to hospitality-driven strategies that emphasize connection and retention. They’re personalizing offers, refining brand experiences and aligning digital tools to reinforce—not replace—the in-person connection that drives loyalty.

Replay the full 2026 State of the U.S. Wine Industry discussion

Our live virtual event explored this year’s findings with Rob McMillan, EVP and founder of the SVB Wine Division. Rob is joined by Industry veterans Janie Brooks Heuck, Managing Director of Brooks Wine, Kristin Marchesi, Managing Director at Metis Mergers & Acquisitions, and Matthew Owings, COO and CFO of Rombauer Vineyards.

Explore previous wine reports

Written by SVB's Rob McMillan

As one of the US wine industry’s top business analysts, Rob assesses current market conditions and provides a unique trends forecast in his annual report.