Key Takeaways

- Foreign exchange (FX) rate uncertainty arises from the time an international portfolio company is sold and the funds are repatriated.

- The potential impact on Internal Rate of Return (IRR) can be significant.

- Short-dated forwards can be used to help mitigate the impact of currency fluctuations during this period.

Short-dated foreign exchange (FX) forwards can be used to help mitigate the FX rate uncertainty that rises between the time a portfolio company is sold and the funds are repatriated back.

Situation

A USD-based fund has a European investment that has recently matured. The repatriation process can take up to a month before all docs are finalized. Although the final EUR amount figure is known, the timing of the repatriation is unknown. The timing on the transfer of funds back to the US can take anywhere from a few weeks to a couple of months.

Should EUR appreciate in the interim, the total return (investment yield + FX yield) will increase. However, should EUR depreciate before the final conversion, the total return will decrease resulting in a lower overall final IRR.

To eliminate potential losses due to currency fluctuation, FX derivatives are often used to mitigate this risk so that firms can focus solely on the investment-generated returns.

Potential size of FX rate movement

According to the long-term average price for an at-the-money option in the EUR/USD exchange rate,1 we can assign a 1 in 10 chance that the EUR may move more than 5 percent in either direction over a 4-week period.2

Solution

An FX forward is a contractual obligation to exchange one currency for another at a pre-determined fixed rate and a specific date in the future.

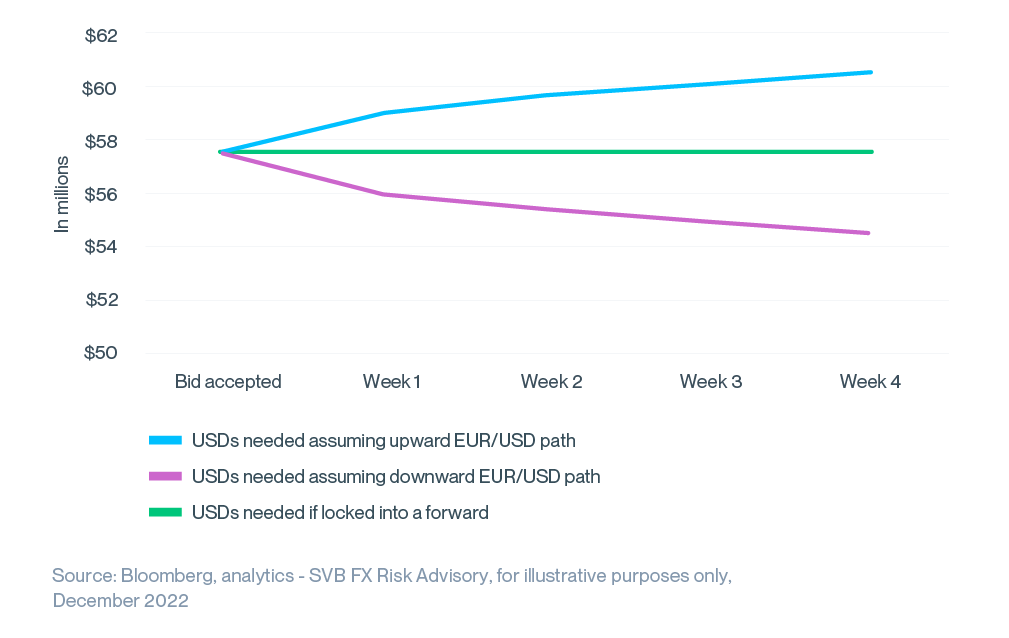

The fund sells the portfolio company for €50.0M to exit their investment. This translates to $57.5M according to the spot rate on the day the portfolio company was sold. Funds will be repatriated in 3 to 4 weeks.

- EUR / USD spot reference: 1.1500

- Direction: Sell EUR / Buy USD

- Notional: €50.0M

- Contract rate: 1.1510

- USD equivalent: $57.65M

- Tenor: 4 weeks

Scenario analysis

The total USDs that will ultimately be repatriated can change materially over a 4-week period.

According to an objective probabilistic framework, there is a 10 percent chance that on a €50.0M price tag, the price can change by more than $3.0M in either direction over a four week period.

However, regardless of where the EUR/USD exchange rate should be trading on expiry date, according to the terms of the forward contract, the Fund will be selling €50.0M in exchange for $57.65M for the exit.

Additional considerations

-

A forward contract represents an obligation to buy or sell currency at a predetermined price. Should the deal fail to materialize, the Fund would need to cash-settle the forward hedge to fulfill the obligation, resulting in a gain or loss depending on spot movements during the hedge period.

-

In the event the deal were to close earlier than expected, forwards may be unwound early without penalty. As a result of the early unwind, the Fund would not be exposed to potential losses from movements in spot rates since trade inception, as the position is hedged. However, movements in the forward curve, which are less material over short horizons, may introduce residual gains or losses.3

-

A delay in the expected deal close date can be handled by rolling the forward for an additional week, month, etc. as required. A “roll” is a standard FX contract, which requires cash settlement.

-

An FX credit line or collateral posting is required to execute forwards. These are small for short-dated tenors.

If you’d like to discuss your specific situation or for information regarding SVB’s tailored FX risk management services, reach out to your SVB FX contact or send an email to GroupFXRiskAdvisory@svb.com.

Read our other FX Risk Advisory papers.