To view the PDF version, click here.

Bottom line

- As a result of the Fed rate hiking cycle that began in 2015, the US has the highest interest rates among developed economy countries. Higher rates have been a key driver to US dollar (USD) strength in the current cycle.

- The prospects of a stronger USD has put exit FX hedging on the radar for USD funds with overseas assets. If these assets are domiciled in developed economies, FX forward contracts may be used to lock in up to +3% of internal rate of return (IRR) while helping with eliminating FX rate uncertainty.

- Exit date uncertainty may be best handled by longer tenors, as opposed to rolling shorter tenors.

Situation

A USD fund (“Fund”) invested in foreign-denominated assets in Europe has an expected holding period of 3 to 5 years. Currency fluctuations over that time horizon can be significant, and may cause a material drag on Fund total return.

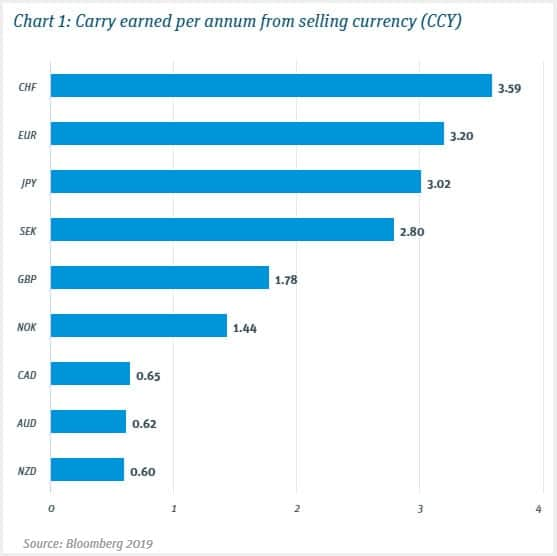

Global investors eyeing an exit may use FX forward contracts to hedge against currency movements1 . Due to the rise in US interest rates, currency hedgers receive a better rate for selling developed economy currencies (and buying USD) on the forward market as opposed to the spot market. This benefit, known as the FX carry pick-up, generally grows with tenor. Chart 1 shows the FX carry pick-up for selling G10 currencies versus the USD2 as of April 2019.

The value proposition in this case is attractive, especially absent of a strong view on the direction of foreign currencies. The Fund receives additional return and no exposure to currency risk.

Implementation consideration

Success of the forward hedging strategy relies on managing the economic impact of two unknowns: Exit asset value and exit date.

Exit value uncertainty is generally handled by executing the hedge in layers or tranches, starting with the initial capital as the first order hedge and then upsizing according to the rise in NAV. Alternatively, exit value uncertainty may be handled through the use of currency options3.Exit date uncertainty, on the other hand, may be addressed by rolling annual FX forwards, or by electing a longer tenor that will sufficiently cover the expected holding period and unwinding the hedge early as needed. The tradeoffs are central to deciding between the two. Rolling annual hedges requires less credit or collateral posting, but exposes the Fund to an undesirable cash event at expiry of the hedge which is not offset by cash flows from the exit. Opting for a conservatively longer tenor would require greater credit to enter into, but will avoid the cash event, assuming the exit occurs prior to the expiry of the contract.

Scenario analysis of alternatives

With an expected holding period of 3 to 5 years for its European assets, the Fund has two strategy alternatives involving FX forward contracts for hedging the realized USD IRR against a weaker euro.

| EUR/USD spot reference: 1.15 Alternative 1: Annual roll Direction: Sell EUR (Buy USD) Notional: €100.0M Tenor: 1 year Contract rate: 1.18 |

Alternative 2: Longer tenor, early unwind Direction: Sell EUR (Buy USD) Notional: €100.0M Tenor: 5 years Contract rate: 1.30 |

| After first year, spot is 1.10 Initial contract settles, the Fund receives +$8M from hedge gain, enters new 1-year hedge at 1.1300 |

No cash settlement Mark-to-market gain on the original forward is +$8M |

| After second year, spot is 1.20 Existing contract expires, the Fund pays $7M to settle hedge loss, enters new 1-year hedge at 1.2300 |

No cash settlement Mark-to-market loss between years 1 and 2 is -$7M |

| After third year, spot is 1.05, asset is sold Existing hedge expires with gain $18M Total hedge P/L: $8M-$7M+$18M=$19M $19M ($10M from spot, $9M from points) Proceeds from asset sale: $105M Total USD return: $105M+$19M=$124M |

Hedge unwound early, with spot 1.05, 2-year forward to original expiry is 1.11, total gain on the contract is $19M $19M ($10M from spot, $9M from points) Proceeds from asset sale: $105M Total USD return: $105M+$19M=$124M |

Summary and conclusions

Protection from a lower EUR/USD spot rate is the same for both strategies.

In this example, the total gain from hedges inclusive of the forward points is also the same for both strategies because it was assumed that the EUR/USD forward points are static throughout the hedge period. In reality, the forward points will move, but the volatility is much less than the volatility of the spot FX rate.

As long as US interest rates are higher than EU interest rates, the forward point adjustment on the hedges will boost IRR. The benefit of longer dated versus shorter dated forwards is that this strategy locks the current carry benefit which is at multi-year highs.

Exit date uncertainty is best handled by longer tenors, as opposed to rolling shorter tenors, as they avoid interim cash events.

If you’d like to discuss your specific risk profile, contact Bobby Donnelly at bdonnelly@svb.com, West Coast/Central, or Ben Johnston at bjohnston@svb.com, East Coast. You can also contact the author, Ivan Oscar Asensio, Head of FX Risk Advisory, at iasensio@svb.com.

Read our other FX Risk Advisory papers.

1. An FX forward is a contractual obligation to exchange one currency for another at a pre-determined rate and date in the future. When used in hedging situations, FX forwards offer downside protection, IRR certainty, and favorable pricing over prevailing spot rates in G10.

2. The pricing of FX forward contracts is derived from three market factors: 1) spot exchange rates, 2) interbank interest rate differentials, and 3) cross-currency basis swap rates.

3. See SVB FX Risk Advisory Whitepaper, Exit FX hedging series: Part III.

The views expressed in this article are solely those of the author and do not necessarily reflect the views of SVB Financial Group, Silicon Valley Bank, or any of its affiliates. This material, including without limitation to the statistical information herein, is provided for informational purposes only. The material is based in part on information from third-party sources that we believe to be reliable but which has not been independently verified by us, and, as such, we do not represent the information is accurate or complete. The information should not be viewed as tax, accounting, investment, legal or other advice, nor is it to be relied on in making an investment or other decision. You should obtain relevant and specific professional advice before making any investment decision. Nothing relating to the material should be construed as a solicitation, offer or recommendation to acquire or dispose of any investment, or to engage in any other transaction.

Foreign exchange transactions can be highly risky, and losses may occur in short periods of time if there is an adverse movement of exchange rates. Exchange rates can be highly volatile and are impacted by numerous economic, political and social factors as well as supply and demand and governmental intervention, control and adjustments. Investments in financial instruments carry significant risk, including the possible loss of the principal amount invested. Before entering any foreign exchange transaction, you should obtain advice from your own tax, financial, legal, accounting and other advisors and only make investment decisions on the basis of your own objectives, experience and resources.

All non-SVB named companies listed throughout this document, as represented with the various statistical, thoughts, analysis and insights shared in this document, are independent third parties and are not affiliated with SVB Financial Group.

The views expressed in this article are solely those of the author and do not necessarily reflect the views of SVB Financial Group, Silicon Valley Bank, or any of its affiliates.

This material, including without limitation to the statistical information herein, is provided for informational purposes only. The material is based in part on information from third-party sources that we believe to be reliable but which has not been independently verified by us, and, as such, we do not represent the information is accurate or complete. The information should not be viewed as tax, accounting, investment, legal or other advice, nor is it to be relied on in making an investment or other decision. You should obtain relevant and specific professional advice before making any investment decision. Nothing relating to the material should be construed as a solicitation, offer or recommendation to acquire or dispose of any investment, or to engage in any other transaction.

Foreign exchange transactions can be highly risky, and losses may occur in short periods of time if there is an adverse movement of exchange rates. Exchange rates can be highly volatile and are impacted by numerous economic, political and social factors as well as supply and demand and governmental intervention, control and adjustments. Investments in financial instruments carry significant risk, including the possible loss of the principal amount invested. Before entering any foreign exchange transaction, you should obtain advice from your own tax, financial, legal, accounting and other advisors and only make investment decisions on the basis of your own objectives, experience and resources.

All non-SVB named companies listed throughout this document, as represented with the various statistical, thoughts, analysis and insights shared in this document, are independent third parties and are not affiliated with SVB Financial Group.

CompID-041819