We’re pleased to provide you with insights like these from Boston Private. Boston Private is now an SVB company. Together we’re well positioned to offer you the service, understanding, guidance and solutions to help you discover opportunities and build wealth – now and in the future.

For long-term investors, litigation finance can be an effective way to diversify portfolios in today’s economic climate. See how providing capital to fund legal expenses is a less competitive option than traditional equity and fixed income investments that has the potential to offer promising returns.

Modern investors often hear the typical talking points on volatile equities and low-yielding fixed income. In current times, there is no shortage of risks to worry about in your investment portfolio. However, investors can benefit by expanding their investable universe beyond traditional markets. As Harry Markowitz made famous with Modern Portfolio Theory, an optimal portfolio is diversified among as many different types of uncorrelated risk assets as possible. An example of such a risk asset is litigation cases.

Litigation finance managers are tapping into a vast, diverse, and complex market with substantially less competition among professional managers than traditional equity and fixed income. This nascent and growing asset class exposes investors to legal risks inherently separated from the typical economic risk exposures. Long-term oriented investors would be well served to add litigation finance to their portfolios to improve the odds of efficiently reaching their financial goals.

This paper will define litigation finance, discuss why it should be considered in an investment portfolio and review the investment opportunity.

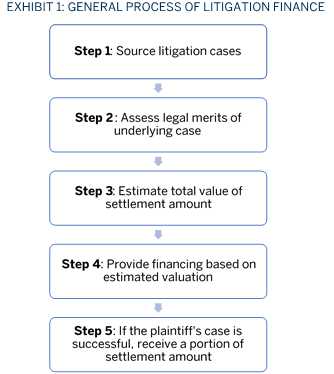

Wait, what’s litigation finance?

Litigation Finance is broadly defined as a third party funder providing capital to fund legal expenses in exchange for a share of any litigation settlement. Legal assets are collateralized for funders that can provide capital now. Simply put, litigation finance is investing in the unrealized values of legal cases—just as an equity manager invests in a stock in anticipation that the stock value will increase.

Contingency claims are central to the success of litigation finance. A contingency claim is a legal claim where payment is contingent on the case outcome. This structure presents an issue for law firms and claimants. Law firms must decide whether to finance meritorious contingency cases themselves (as in they don’t get paid before case outcome) or pass on the potentially lucrative settlement amount to third parties. Likewise, claimants are in a difficult position of paying expensive legal fees or searching for a law firm that will take the contingency. Litigation finance helps both parties avoid this tough decision while maintaining incentive alignment to resolve the case in their best interest.

Why allocate to litigation finance?

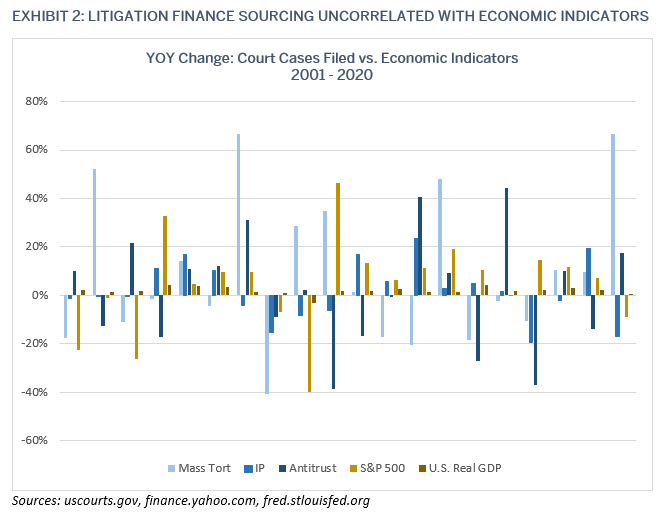

The biggest reason is diversifying risk exposure. Litigation cases are not influenced by the movement of the S&P 500 or vice versa. Theoretically, this makes sense. However, we were interested in empirically testing this as thoroughly as possible.

We examined the year-over-year change in the number of cases filed in U.S. District Court across three common case types for litigation funders: Mass Torts, Antitrust and Intellectual Property against the year-over-year change of the average S&P 500 and U.S. Real GDP levels over the same time frames (year ending March 31, 2020).

The rate of change of cases filed (i.e. investment opportunities) and traditional economic indicators support the theory of a lack of correlation. Year-over-year change for each case type had a correlation coefficient below 0.50 with both the change in the S&P 500 and in U.S. Real GDP. Further, and possibly as important, changes in each respective case type were uncorrelated to each other, with correlation coefficients between -0.25 and 0.25 across the three. This provides further credence that investors are well-served to allocate to a diversified portfolio of litigation assets.

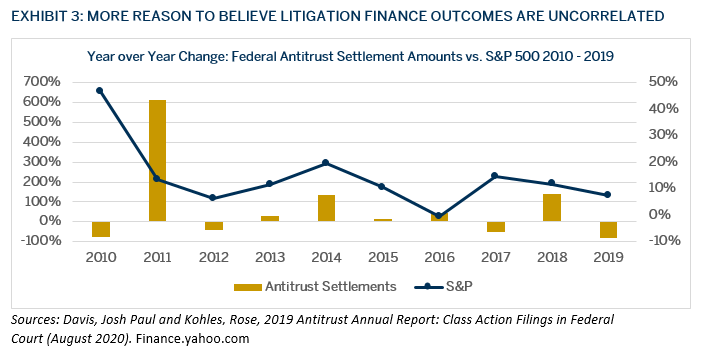

Number of cases filed are leading indicators of what investors actually care about—settlement amounts. While data on case settlement amounts is difficult to find due to their confidential nature, we were able to find total settlement amounts per year in Federal Antitrust Class Actions.

In a short time period, correlations between the yearly rate of change in antitrust settlement amounts and economic indicators is slightly negative, -0.11 to the S&P 500 yearly change and -0.12 to U.S. Real GDP yearly change (U.S. Real GDP was excluded from the graph due to small yearly changes that distorted the visual).

The data, albeit limited, supports the theoretical reasoning that the investment universe sourcing (cases filed) and the returns (settlements) of litigation finance are uncorrelated from traditional investment portfolios; thereby offering excellent diversifying exposure.

Asset class review - with less competition, skill can thrive:

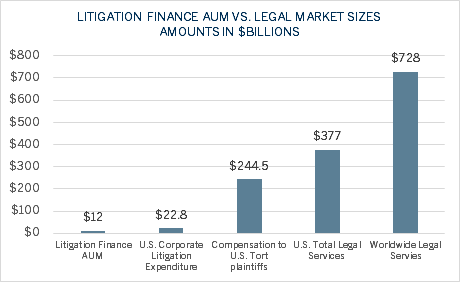

Like other areas of this asset class, there is an opaque view into the overall size. However, Westfleet, a broker in the space, estimates total assets under management of $10 - $12B across U.S. litigation funders1. This growth has primarily occurred in the last 5 – 10 years as law firms have become more aware of the opportunity provided by third party financing. In a 2018 survey, 70% of lawyers responded that they have used litigation finance, up from 10% in 20122.

In terms of opportunity, we get a glimpse into the market of litigation cases by looking at case numbers across state and federal jurisdictions. There are more than 250,000 – 300,000 federal U.S. district civil cases filed per year. At the state level, there are approximately 15 million civil cases filed per year3. Litigation spending by large U.S. corporates per year since 2015 has been approximately $20 billion4. U.S. total legal services, as in costs involved in litigation, have totaled more than $350 billion since 2017 and that figure is rising5. In 2016, the estimated compensation to U.S. tort plaintiffs was $244.5 billion6. Worldwide legal services totaled more than $728 billion in 20207.

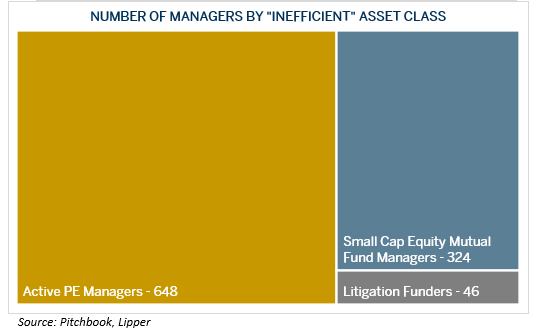

Litigation Finance is far less of a zero-sum game compared to investing in public markets where one side of a trade is always losing. There are an estimated 46 litigation funders in the U.S. If we compare that figure to other asset classes that are often considered less efficient, we see this is a much different game. According to PitchBook, there are 648 active U.S. private equity managers. According to Lipper peer groups, there are 324 small cap equity mutual funds.

With less competition for investment opportunities, there is more to go around for the fewer players in the space. With less competition for opportunities, litigation funders can be extremely selective. Most managers estimate they fund 5% or less of cases that they review. With less competition, there are fewer investors bidding up the price to finance an attractive case and fewer lenders bidding down the interest rates on law firm loans. These factors create advantageous competitive dynamics that add to our conviction in the space.

While the opacity of the asset class made research for this paper a bit cumbersome, the opacity can also be seen as a necessary, even positive, attribute. Take the public equity market as a comparison. If an investor is interested in researching a company, there are countless data providers with readily available information, packaged in a clean, uniform manner, providing investors with instantly actionable insights. This transparency creates lower barriers to entry and drives further competition, as we have seen over the last several decades. In comparison, litigation finance is highly complex with no central aggregators. More time and human capital intensive work is required. Likewise, ‘Litigation Finance: 101’ is not being taught in Business or Law Schools (yet). That is a very good thing for investors in this asset class.

Risk and return considerations:

There are risks to the asset class that investors should understand. First, litigation finance is a long duration asset. Cases generally take 3 – 5 years to settle based on manager estimates and outside research. There is a risk that the longer a case goes, the more likely the ruling will not be in the manager’s favor. At the same time, if a case takes longer than expected and still settles in the manager’s favor, distributions to investors will occur later in the fund life, resulting in a lower internal rate of return—commonly referred to as IRR and can be considered the annualized rate of return. As most exposure to litigation finance is through private funds with a committed capital structure, investors should be aware of the J-curve effect, named for the shape of the profit curve, where investors are likely to realize losses early in a fund’s life. This is caused by a fee drag, where investment managers charge a fee before profitable returns are realized by end investors, which likely coincides with the timing of case settlement.

The broad investable universe to litigation funders means there is a wide spectrum of available exposures. We largely split litigation finance into event-driven and credit exposures. Event-driven provides capital to directly support the outcome of one or more cases. This is similar to equity with higher risk/return and inherent binary risk of case outcome. A complete loss of capital on any one case is a possibility as is a large return on capital if the settlement is as expected. In these cases, managers should be aiming to earn investors 20%+ net IRRs. Event-driven exposure can lead to increased fee drag as managers tend to slowly deploy capital into ongoing cases over an extended time period.

The credit or lending approach has a lower risk/return profile with managers typically targeting low- to mid-teens net IRRs. This approach lends capital to a law firm or claimant with litigation cases acting as the collateral for the lender’s capital. Using this approach, deployment is more likely to occur earlier in the fund’s life, which should lessen the fee drag.

Why you should consider litigation finance:

You are likely seeing headlines regarding historical highs and lows—historically high equity valuations and historically low fixed income returns. Add in the evolving risk of inflation and it is fair to wonder if there is a way to avoid these issues. Litigation finance offers exposure to the outcome of litigation cases which are uncorrelated to traditional markets. This uncorrelated nature plus an asset class with less competition and high inefficiency makes litigation finance an attractive option for long-term investors.

We will continue to investigate, adapt and research litigation finance as the space evolves in order to offer you top-tier investment options. Our team is focused on improving the odds of successful investment outcomes and we believe litigation finance helps us accomplish that objective. For more information on our recommended investment options, please reach out to your financial advisor.

1. Westfleet Insider 2020 Litigation Finance Market Report

2. https://www.lexshares.com/blog/litigation-finance-growth-2030/

3. http://www.courtstatistics.org/__data/assets/pdf_file/0014/40820/2018-Digest.pdf

4. https://www.statista.com/statistics/941275/litigation-spending-united-states/

5. https://www.bea.gov/data/industries/gross-output-by-industry

6. U.S. Chamber Institute for Legal Reform’s “Costs and Compensation of the U.S. Tort System”

7. https://www.statista.com/statistics/605125/size-of-the-global-legal-services-market/