We’re pleased to provide you with insights like these from Boston Private. Boston Private is now an SVB company. Together we’re well positioned to offer you the service, understanding, guidance and solutions to help you discover opportunities and build wealth – now and in the future.

Learn how you and your family members can use credit to your advantage

As you develop your personal, professional and financial plans, having an understanding of your credit can help you more efficiently achieve your goals. Personal credit plays a critical role in our financial health, so it’s important to know how to create a solid foundation, monitor progress and build your credit into a dependable resource that can be utilized throughout your lifetime.

Today, we’ll define personal credit and discuss the fundamentals that can help you quickly establish, oversee and optimize your credit as you pursue your financial objectives.

What information is included in my credit report?

Your credit report is a detailed record of your credit history, starting from the time you initially establish credit. Your report includes information regarding the companies that have loaned you money, the amount of each of your past and present loans, how often your payments were made on time and whether or not you missed any payments along the way.

What does my credit score represent?

Your credit score is determined by a formula that measures your credit risk based on the information contained in your credit report. Credit scores are expressed as three-digit numbers that illustrate to lenders how likely you are to pay your bills on time.

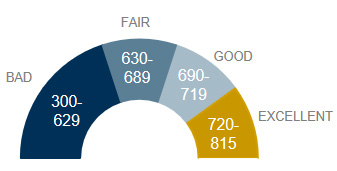

The FICO® score is the most widely used credit score in the U.S. Most credit scores have a range between 300 and 850. The higher the score the, the better your credit. A credit score in the 670 to 739-point range is considered good. Having a higher credit score gives you a better chance of being approved for more favorable financial terms such as higher credit limits and better loan rates, which may save you thousands of dollars in interest payments over the course of your lifetime.

How is my credit calculated?

Your credit score is based on a combination of factors that are used by the credit bureaus to predict the likelihood that you will repay your debts. The five factors used to determine your credit score are:

- How much you currently owe to creditors

- The number of on-time payments you’ve made

- The length of time of your credit history

- Your credit mix (the different types of credit you currently have outstanding)

- New credit (credit that has been added to your credit report during the last 12 months)

The factors above are weighted, where payment history and amount owed are considered the most important elements when calculating credit scores – representing 35% and 30% of your score’s calculation respectively.

What are the important credit terms to know?

Becoming familiar with the financial terms below will help you have a better understanding of the information often found in credit reports, loan documents and credit card offers.

- Annual percentage rate (APR) – The yearly cost of borrowing money expressed as a percentage of the loan.

- Available balance – The total amount of funds in an account that can be used for purchases or withdrawals.

- Billing cycle – The amount of time between the closing of two consecutive billing statements.

- Credit history – The record of how a person has managed their credit accounts to date.

- Credit limit – The dollar amount of credit a lender is willing to grant to a borrower.

- Credit utilization rate – The amount of revolving credit used divided by the available revolving credit (a percentage)

- Fixed APR – The annual percentage rate of interest charged. This rate will not change over the life of a loan.

- Index rate – An interest rate that changes with changes to a benchmark interest rate, such as the Prime Rate.

- Introductory APR – A reduced annual percentage rate offered for a set time period. Typically offered as a promotion.

- Prime rate – The interest rate that commercial banks charge when making loans to their most creditworthy customers.

- Outstanding balance – The amount of money currently owed on an interest-bearing debt.

- Revolving credit – Credit that allows a borrower to borrow and repay money repeatedly, such as a credit card account.

- Variable APR – An annual percentage rate that changes over the life of a loan, typically changing with an index rate.

How do I establish credit?

Getting started with credit need not be difficult. To establish your credit, we recommend turning to a financial institution that you already have a relationship with. Reach out to the bank that services your checking or savings accounts and explore options like applying for a credit card or, if needed, an installment loan for a home appliance, furniture or vehicle purchase. Applying for a gasoline credit card that you use only for fill ups is another effective, low-impact option. If you use it just for gas, a gasoline card allows you to establish credit while making relatively low-cost purchases of a necessity.

How do I use credit wisely?

When used correctly, an effective credit tool such as a no-fee credit card can help you establish your credit and make your money work harder for you. Selecting a no-fee credit card that offers you travel points or cash back options can help you get more from your day-to-day purchases. For example, when using a debit card for purchases, the funds are immediately withdrawn from your bank account at the time of purchase. However, when using a credit card for those purchases, the funds are not due from you until the next billing cycle – and you may also receive 1% cash back on some of the purchases.

Using credit cards versus a debit cards also offers an additional layer of fraud protection as the issuing banks closely monitor credit card transactions for fraudulent activity. Since credit card purchases are initially made with the issuing banks funds, the banks will work diligently with you to resolve any fraudulent charges that are discovered.

Why should I review my credit score?

Keeping an eye on your credit history and credit scores can help you better understand your current credit position and make improvements. Along with other information, potential lenders and creditors, including credit card companies, mortgage and auto lenders may use your credit scores and credit history to help make lending decisions. Basically, these companies will review your credit scores to learn how likely you are to pay back the money they lend you.

By proactively checking your credit reports, you will be more aware of what lenders will see when you apply for a loan or an additional credit card. Reviewing your credit reports can also help you detect any inaccurate or incomplete information. Because of this, it’s important to regularly check your credit scores and your credit reports.

How do I review my credit?

To review your credit you may request a copy of your credit report from any one of the three national credit reporting bureaus – TransUnion, Equifax and Experian. You may receive one free copy of your credit report from each of the three bureau every 12 months.

We recommend that you request a fresh copy of your report every three months or so, using a different credit bureau. Take some time to review your reports to be sure the information is accurate and complete. Also, make sure you recognize all transactions and immediately report any activity you do not recognize. Visit annualcreditreport.com to request your free credit reports.

How do I improve my credit score?

Once established, there are a few straightforward steps you can take to improve your credit score. Here are some impactful tactics to keep your credit heading in the right direction. Please note that it’s important to be patient as it can take time to build a good credit score.

DO:

Pay outstanding debts on time – Set up automatic payments or reminders to help keep all your payments timely

Pay in full – Try to make more than the minimum required payment, so your debt does not increase each month

Make use of different credit types – Such as revolving credit (credit cards) and installment loans (home mortgages, auto loans or student loans) in order to have a healthy credit mix

AVOID:

Max out your credit limit – A lower credit utilization ratio is always better

Close old credit accounts – The longer your credit history, the better

Open several new accounts at once – Lenders see this behavior as a red flag when reviewing your credit

Credit score ranges

Who can advise me with my credit needs?

An experienced financial planner can help ensure that you have access to the credit you need to pursue your personal, professional and financial goals.

An effective financial planner offers:

Organization – Bringing order to your financial life

Accountability – Helping you follow through on your financial commitments

Objectivity – Helping you avoid emotionally-driven decisions

Proactivity – Helping you anticipate and prepare for significant life transitions

Education – Providing explanations tailored to your options and potential risks

Partnership – Working with you to help you achieve your most critical goals

Who can I contact for more information?

As you explore your financial options, we would be delighted to help. When helping clients pursue their financial goals, we employ a diverse team of professionals to bring the custom-tailored services of a boutique wealth management firm to life. When it comes to execution, we provide the resources and technology of a large financial institution.

As our valued client, you have access to a full spectrum of wealth, trust and banking services. If you have been looking for a meaningful relationship with a wealth advisor who has the expertise needed to help you achieve your goals while mitigating risks, consider us.

For additional information regarding the key components of credit management, listen to our Using Your Credit Wisely podcast today.