We’re pleased to provide you with insights like these from Boston Private. Boston Private is now an SVB company. Together we’re well positioned to offer you the service, understanding, guidance and solutions to help you discover opportunities and build wealth – now and in the future.

Getting up to speed before open enrollment begins in October

With “open enrollment” for Medicare just a few short weeks away (October 15th through December 7th), it’s time for people who have Medicare benefits to review their coverage and switch plans if they want different options — or more savings.

“Reassessing your choices every year to accommodate changes in your health or the prescriptions you’re using is important,” says Dianne Savastano, founder and president of Healthassist, an independent advisory firm that guides individuals and families through the health care and insurance maze. “Plus, there may be changes in your existing plan provisions or pricing that you need to address.”

In addition, many plan details, rules, and prices change from year to year, based on legislative changes and cost-of-living increases. In 2018, for example, the thresholds for high income earners were reduced, so more participants paid higher Part B and Part D premiums. Further changes are planned for 2019 (more on that later). “That’s why you really do have to pay attention before making decisions that will affect your health care options and expenses,” cautions Savastano.

It’s also a good time for anyone approaching Medicare eligibility at age 65 to get up to speed on how the program works and begin to understand their choices “before becoming inundated with marketing offers from insurance companies eager to sign you up,” says Savastano.

Here, with Savastano’s assistance, is a review of five key facts about Medicare that can help you make wise choices, whether you are new to the program or already enrolled.

Fact #1: For Americans 65+, Medicare is not optional

Once you reach age 65, you must enroll in Medicare, unless you are still covered by an employer’s health insurance plan. If so, you can defer enrollment and enroll during a Special Enrollment Period (SEP) when the employer coverage comes to an end. Once you retire and you are age 65 or older, Medicare isn’t optional, says Savastano, “it’s the ‘only game in town’.

In addition, you must enroll sometime between three months before and three months after the month of your 65th birthday (a total of seven months). If you don’t, you can still apply later during Medicare’s general enrollment period (from January 1st to March 31st each year), but you’ll permanently pay higher premiums as a penalty for your delay.

On the other hand, if you are fortunate enough to be able to retire before age 65, you’ll need to find a “bridge” of health insurance coverage until your Medicare benefits kick in. This could be COBRA benefits offered by your former employer, a policy purchased through your state’s health insurance exchange, or private insurance you buy on your own.

Fact #2: It’s unlike any other health care plan you’ve ever had

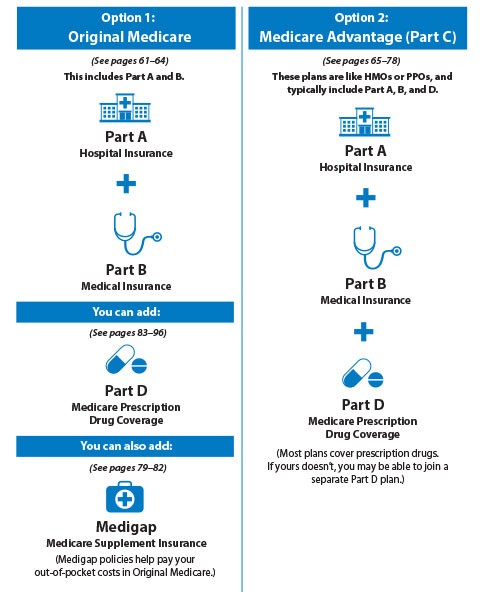

While you’ll have many choices of insurance carriers under some portions of Medicare, the structure of your coverage is very different from the plans you’ve been familiar with during your working years, as shown in the illustration below. Here’s how Medicare works:

- The basic portion of Medicare, Part A, covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. Most people pay no premiums for this part of your insurance, but it is subject to a deductible and coinsurance.

- Part B covers many of the medical expenses that Part A does not, including certain doctors' and health care providers’ services, outpatient care, medical supplies, durable medicate equipment, home health care, and some preventive services.

- If you are collecting Social Security, your premiums for this portion of Medicare can be deducted from your monthly Social Security check. If you’re still working, you’ll need to pay for this yourself every month directly or through an automatic deduction from your bank account. In addition, if your Modified Adjusted Gross Income (MAGI) exceeds certain limits, you’ll pay extra premiums for Part B and Part D. (See Fact #4.)

- If you decide to cover additional health care expenses that Parts A, B, and D don’t take care of, you have the option of adding Medicare Supplement Insurance through the purchase of a Medigap policy that “wraps around” traditional Medicare with additional coverage that can pay for your extra expenses, allow you to select your individual doctors, and have coverage in multiple states.

- Alternatively, and in lieu of traditional Medicare Parts A, B, and D, you can choose a Medicare Advantage Plan (also known as Part C) that combines all three parts in a single policy. These plans are similar to Health Maintenance Organizations (HMOs) or Preferred Provider Organizations (PPOs) because they require referrals and limit providers to those within their network. Most Medicare Advantage Plans include prescription drug benefits. Some charge a premium for the coverage they provide, while others do not.

- If you don’t have prescription drug coverage through a Medicare Advantage Plan, you’ll also need to purchase Part D insurance on your own. Again, the Part D plans available to you will vary based on where you live, so it’s important to compare them on the Medicare site.

Because the insurance plans that supplement basic Medicare can vary widely in terms of coverage, costs, deductibles, and co-pays — and these can change every year — It’s important to compare the ones available in your area. Fortunately, there are tools to help you do this on www.Medicare.gov.

Source: https://www.medicare.gov/pubs/pdf/10050-Medicare-and-You.pdf, p. 4

Fact #3: Medicare only pays for a portion of your health care expenses1

While the different parts of Medicare are designed to cover specific services (as outlined above), you will have to pay for the services Medicare doesn't cover unless you have other insurance to take care of them. Some of the items and services that Medicare doesn't pay for include:

- Deductibles, co-insurance, and co-payments

- Long-term care

- Most dental care

- Dentures

- Eye examinations for prescribing glasses

- Cosmetic surgery

- Acupuncture

- Hearing aids and exams for fitting them

- Routine foot care

Fact #4: It could cost you more than you anticipated

What surprises Savastano’s clients the most when they start navigating their Medicare choices?

First, the fact that Medicare isn’t free. And second, that they may end up paying even more than they expected.

Even though Part A is usually “premium free,” for example, you’ll still need to pay deductibles and co-insurance charges for that coverage. And that goes for Parts B and D of Medicare as well. Purchasing one of the supplementary insurance options can help you pay for these additional expenses and other services that are not covered by Medicare.

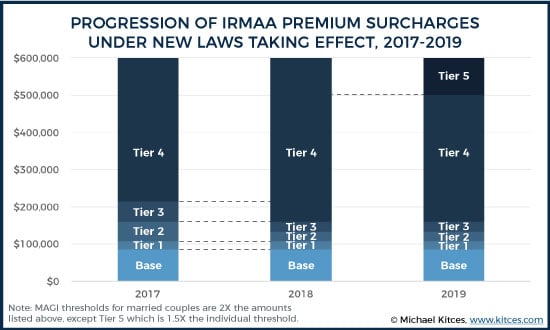

In addition, if you are in a higher tax bracket, you may be required to pay an Income-Related Monthly Adjustment Amount (or IRMAA) for your Part B and Part D coverage. Introduced in 2011 as part of the Affordable Care Act (ACA), the extra IRMAA charges are based on your level of income and can change from year to year. For 2019, a new tiering structure and adjusted threshold amounts will have an impact on some high-income earners. The charges for 2019 are shown below:

New medicare income related monthly adjustment amounts for 2019(before 2019 medicare inflation adjustments)

|

IRMAA Tier |

Individual MAGI |

Married Joint MAGI |

Part B Premium (Monthly) |

Part D Premium (Monthly) |

|

Baseline |

< $85,000 |

< $170,000 |

$134.00 |

Varies by plan selection |

|

1 |

Up to $107,000 |

Up to $214,000 |

+ $53.50 |

+ $12.40 |

|

2 |

Up to $133,500 |

Up to $267,000 |

+ $133.90 |

+ $31.90 |

|

3 |

Up to $160,000 |

Up to $320,000 |

+ $214.30 |

+ $51.40 |

|

4 |

> $160,000 |

> $320,000 |

+ $294.60 |

+ $70.90 |

|

5 |

> $500,000 |

> $750,000 |

+ $321.40 |

+ $77.40 |

The Social Security Administration (SSA) calculates each individual’s Part B and Part D premium adjustments each year based on the income reported to the IRS two years before. In 2018, for example, the SSA used 2016 income tax data. But if your income is lower in a more recently filed income tax return, you can contact Social Security (and submit the paperwork) to request a change in your IRMAA charges.

To learn more about the IRMAA rules, you can download Medicare’s free booklet “Medicare Premiums: Rules for Higher-Income Beneficiaries” at Medicare.gov.

Fact #5: Your choice of plans depends on multiple variables

In her practice, Savastano finds that people often assume that a supplementary Medicare or prescription drug plan with a higher cost will give them greater value. “But that’s not always true,” she stresses. “That’s why it’s so important to conduct a detailed analysis when you’re making your choices.”

Some considerations in your selection process include:

- The amount and type of your medications. With a prescription drug (Part D) plan, the covered medications and charges for them can vary widely among providers. “Sometimes they don’t cover them at all or they cover them differently. So you want to make sure that the plans you’re looking at cover your medications. Then you want to compare how one plan compares to another because the cost differential can be very high,” she explains.

- Your choice of doctors and where and how you like to access your care. When it comes to supplementary medical coverage, Savastano suggests starting with what you know by looking at what you had in the past. “If you had a traditional HMO or PPO you may be accustomed to having a referral requirement or staying within a network, so a Medicare Advantage Plan may be appropriate. But if you’re going to spend several months of the year in another state, you probably want to have more flexibility by choosing a Medigap provider. So a lot of your choices can be narrowed down based on what you’re comfortable with.”

- Your health status. “Whether you’re a heavy user of the health care system or a very light user will make a difference in the out-of-pocket costs you’ll incur going forward,” Savastano says.

Fortunately, you can start your exploration using the analytical tools available on www.Medicare.gov. They use the data you provide to serve up summaries of the coverage and costs of the plans in your region that most closely meet the criteria you choose.