Key takeaways

-

Endure the inevitable challenges of growing your company by prioritizing your personal financial health.

-

Reduce personal exposure by solidifying your financial plans during your company’s early growth stages.

-

Use a longer-term approach to planning and consider your own basic needs throughout your journey.

The devil's in the financial details

As a founder, you have a vision for where you want your company to go, and how quickly you want it to get there. You’re focused on its long-term wellbeing commercially and financially. But if you’re like many founders, you may not have given the same amount of attention to your own financial health.

At SVB Private, our team helps clients think holistically about the founder experience – from both the personal and professional perspectives. Here, we’ve compiled five strategies we call ‘The Founder Stack’ to get you thinking about yourself the way you think about your company. Similar to the decisions you make regarding your CRM system, marketing tools and web hosting service, thought should be devoted to your estate, private stock, bank account and much more.

Related resource: How do I effectively manage my equity as a founder?

1. Assemble your financial team

Selecting the appropriate members of your financial team is an essential first step for you and your company’s long-term success. We recommend starting the selection process with your CPA as they will be instrumental in several critical financial decisions made by you and your fellow founders.

Selecting a CPA with the proper skills and background is important as there are several financial choices that will have significant impacts on your company as well as your personal financial health, such as:

-

Selecting the most financially advantageous company ownership structure (discussed further below)

-

Your eligibility for Qualified Small Business Stock exclusions

-

The tax benefits, feasibility and timing of Section 83(b) elections

To properly address these complex topics, we recommend selecting a CPA with extensive experience serving startups as well as a thorough understanding of your industry and sector.

2. Understand your salary and personal cash flow requirements

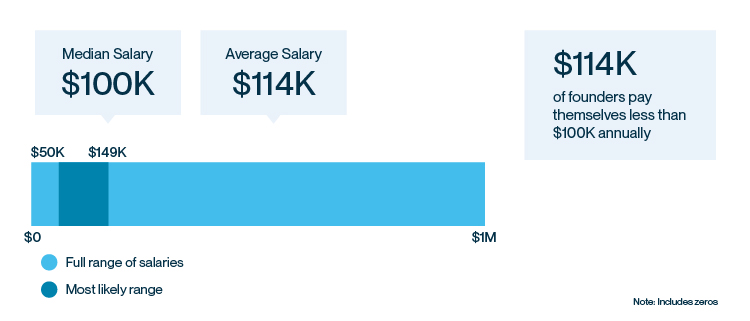

One of the most frequent questions we hear from founder clients is, “What should I be paying myself?” This is an important issue to consider as we’ve seen that many founders significantly underpay themselves then struggle to meet their family’s basic needs.

A study conducted by Pilot in 2022 found that nearly half of the 500 startup founders surveyed pay themselves less than $100,000 annually.1 The study indicates this is below the average salaries in US locations such as Boston, Texas, the San Francisco Bay Area, and in international locations, too.

Lower compensation can become a big issue (as can equity-only compensation), especially when founders are interested in making a large purchase, such as a home.

When it comes to housing, the challenge for many underpaid founders is the debt-to-income ratios required for traditional mortgages can make home purchases difficult. This may be avoided by adopting a more pragmatic philosophy to cash flow needs and salary expectations. We advise clients that there is no need to believe that financial sacrifices should be a badge of honor for founders.

Regarding equity-only compensation, a healthy number of founders expect that their equity stake in the organization will eventually take care of them as they’re busy pouring blood, sweat and tears into their company. Unfortunately for many founders, that doesn’t happen. That’s why we feel insisting on getting paid exclusively in equity can be a risky approach.

When discussing salary, we advise clients not to be afraid to ask for an equitable salary from their company’s board. The rationale for this is straightforward. With the basic needs covered by a reasonable salary, a fulfilled founder can devote more energy to the growth and long-term success of their company.

Taking some funds off the table for salary so you can meet some of your personal goals in the early days will nourish you for the longer term so you're not exiting too abruptly as you've taken care of some of your own needs along the way.

Related resource: How can founders qualify for their first home mortgage?

3. Examine your company's ownership structure

The structure of your company is another area that has substantial financial implications for you and your business. Of the three popular business structures used by founders interested in attracting investors, C corporations (C-corps) typically offer the most long-term financial benefits.

Compared to S corporations (S-corps) and limited liability companies (LLCs), C-corps offer advantages such as eligibility for Qualified Small Business Stock (QSBS) exclusions on the sale of the company shares that you acquire as a founder. For example, the QSBS exclusion offers potential tax savings of $10 million or 10 times your cost basis, whichever is higher.

If your company was registered as an LLC, you may also convert the business to a C-corp to qualify for the tax savings offered under the (QSBS) exclusion, as long as the C-Corp meets all eligibility rules under QSBS. If you have a C-Corp and have made an S-Corp election for tax purposes, your shares would not qualify.

For complete details regarding the benefits of C-corps and the steps involved in the LLC conversion, speak with an SVB Private Wealth Advisor.

Related resource: Why the timing of an LLC to C-corp conversion may offer significant tax savings

4. Develop your core estate plan

During the early days of your company’s growth, developing an estate plan may not be at the top on your to-do list. Not surprisingly, many first-time founders do not believe they have enough assets to bother with estate planning early on. This, however, would be a mistake as your new company adds an additional layer of complexity to your financial life that deserves attention sooner rather than later.

As a founder, an estate plan can help protect your family, your business, as well as your co-founders’ interests. For example, without a properly drafted estate plan, your business shares may be tied up in probate if you were to die. Some states also have laws that decide what happens to your assets, which would include your business shares regardless of your marital status and number of children.

The timing of your estate planning is also an important factor as it relates to the valuation of your company shares and the associated tax implications. As a rule, the sooner you act on your estate planning the lower your potential tax burden may be.

The rules governing founder estate plans are complex; however, getting started doesn’t have to be overwhelming. There are four documents in a fundamental estate plan:

-

A will

-

A healthcare directive

-

Living (revocable) trust

-

Powers of attorney

To get a better sense of the advantages of estate planning for early-stage founders, feel free to reach out to an SVB Private Fiduciary Advisor. We can work with you to explore the options that can help protect you, your family and your co-founders’ interests.

Related read: Estate planning essentials: 5 ways founders can get started with prenups

5. Integrate prenuptial planning into your estate plans

Similar to estate planning, prenuptial planning can add a layer of protection to your company as well as your personal finances. In the case of founder prenups, the protection can also extend to the control and direction of your company. And in the case of divorce, a thoughtfully drafted prenup can protect company shares (and possibly voting rights) from an ex-spouse who may or may not share you and your co-founders’ long-term vision for the company.

Naturally, many people may feel apprehensive about discussing this topic with a future spouse. However, you can broach the subject as more of a planning exercise with the business and co-founders in mind versus a purely financial discussion between two future spouses. Timing is also a factor with prenuptial planning. Many founders are apprehensive about broaching the subject and delay the discussions until there is not enough time to properly draft the documents. Getting started sooner rather than later also applies to prenuptial planning.

Related resource: Why founders need prenups and how to structure them

Because of their effectiveness, irrevocable trusts are often used when drafting prenups. Revocable trusts often lack the power needed to stand up when challenged in court. Another item to consider. If you do put your company shares in a trust, then marry, those shares are not considered part of community property. When working with your financial advisors, your prenuptial planning can easily fold into your estate planning discussions. Your financial team can help you navigate the details here.

A final thought

The most important thing as a founder is that you understand your options and discuss the possibilities with seasoned professionals such as the team at SVB Private. It is never too early to have these conversations as they could save you millions of dollars at the company you’re working so hard to grow.

Fully understand your financial options

If you’re interested in establishing a meaningful relationship with a financial team that specializes in the needs of early-stage founders, speak with an SVB Private Wealth Advisor today.