Last month, currency markets were subdued while investors and companies waited for two potentially significant market-moving events: the general election in the United Kingdom on December 12 and US tariffs on Chinese goods on December 15. Of the five major currencies, the euro, Japanese yen, Swiss franc and Canadian dollar saw November trading volatility drop to 20-year lows. The UK pound was the exception, as nervous traders and investors adjusted positions ahead of the December 12 election.1

Currency market volatility has quieted because: 1) current macroeconomic growth and inflation rates remain steady; 2) interest rates remain low following synchronized easing of monetary policies by prominent central banks, and rate cuts by many other central banks from Russia to Turkey; 3) mixed global economic data dampens larger capital flow swings; and, 4) FX traders have been winding down positions as they adopt a wait-and-see approach.

An acceleration in activity in the global bonds and equities markets (or a return to the normal negative correlation between the two markets) could signal a return to volatility. In addition, sudden and profound geopolitical events (for example, a US Presidential impeachment or ‘no-deal’ Brexit) could trigger a rise in large cross-border capital flows, resulting in increased currency volatility.

A less volatile currency market is not an opportunity for complacency. Firms subject to meaningful FX risk should continually identify, manage and, as necessary, mitigate currency risk.

What happened?

US dollar remained steady. Bloomberg’s dollar trade-weight index climbed 1.1% in November 2, despite being overvalued (see my November 21 article, “Dollar overvalued according to PPP. Does it matter?”). Strong equity markets and relatively high bond yields continue to attract global investment into the U.S. According to CFTC (Commodity Futures Trading Commission) reports, dollar positions (long and short) held by large currency speculators are at the lowest levels since early 2018 - suggesting investors are waiting for further clarity regarding the direction of the dollar.

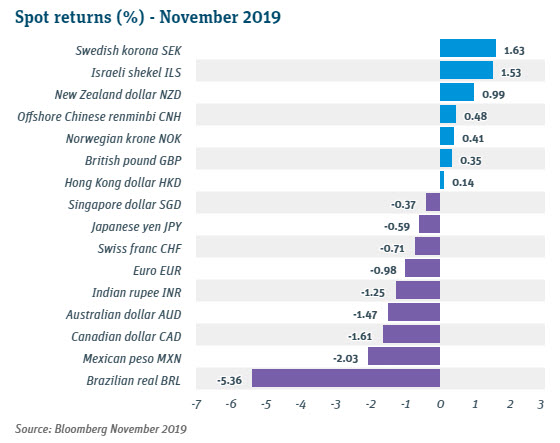

UK pound steady and gaining. The UK pound held its own against a strong dollar and peer currencies as investors anticipate the Conservative Party, led by Boris Johnson, to succeed over the Labor Party on December 12. A Tory victory is anticipated to push the pound even higher.

Brazilian real slumped to a record low. Brazilian policy makers triggered a sell-off in the BRL after signaling their comfort with a weak real. (They ultimately intervened to prevent a further collapse in the currency). Investors worry the government will not be able to reform the nation's high-cost pension system. Brazil’s central bank is expected to cut interest rates this month by an additional 50 basis points to 4.5%.3 The rate cut along with contagion fears associated with ongoing political turmoil in Latin America are expected to place further pressure on the BRL.

Christine Lagarde took over as ECB President. The European Council appointed former IMF Managing Director Christine Lagarde to be the president of the European Central Bank, replacing Mario Draghi. Lagarde emphasized the need for eurozone countries with budget surpluses to spend more to help boost the 19-members that share the euro.4 Getting Germany to engage in fiscal spending may be her biggest challenge.

What's in play?

US recession fears. Notwithstanding market speculation, a recession is nowhere in sight. The labor market, the service sector and consumer data all remain in reasonably good shape. On the other hand, manufacturing is weak, and business investment is down, as firms delay capital spending amid uncertainty regarding the US-China trade war and possible future US policy actions. The inverted yield curve – a widely-held predictor of recessions – is no longer inverted.

US-China trade agreement. Investors are optimistic that ‘phase one’ of the US-China deal will be signed before year-end, as both Presidents Trump and Xi have profound domestic political incentives that could turn on it. If an agreement is not reached by December 15, additional tariffs may go into effect. Trump may choose to suspend tariffs of course (as he did in October for $250 billion in Chinese imports). Watch the USD/CNY for any signals from the Peoples Bank of China.

European economies with upside surprises. Although Europe continues to suffer from sluggish economic growth, nearly all indices released in November exceeded expectations.5 Euro investors have reason for guarded optimism.

An expanding trade war. In retaliation for France’s ‘digital services tax’ on US tech companies, President Trump threatened France with a 100% tariff on key exports to the US, including cheese, handbags and Champagne.6 California sparkling wines remain available.

What's next?

Key central bank meetings:- December 10-11: Federal Reserve Board (FOMC). In the last policy meeting of the year, the Federal Open Market Committee is set to provide a new “dot plot", policy statement, economic projection and press conference.7 The Fed funds rate is expected to remain at 1.50 -1.75 percent.

- December 12: European Central Bank. No change is expected to the ECB’s -0.50% deposit rate or QE program of EUR 20 billion per month of asset purchases. However, it will be important to note Christine Lagarde’s comments in her first official policy meeting. Her focus is expected to be long-range and include views on fiscal spending and climate change.8

- December 19: Bank of England. The BOE is expected to leave its benchmark interest rate at 0.75%, although traders will be listening closely to BOE governor Mark Carney’s comments following the December 12 general election vote. He has said that a rate cut could be imminent if Brexit uncertainty continues to weigh on the UK economy. 9

1,2,3,5 Bloomberg 2019

4 The Guardian, “Lagarde makes first policy speech.” 11.22.2019

6 www.wgal.com, “US threatens 100% tariffs on French cheese and champagne.” 11.30.2019

7 CNBC.com, “Fed to keep rates on hold.”11.18.2019

8 “Christine Lagarde first speech as European Central Bank President.” 11.22.2019

9 The Guardian, “Bank of England cuts growth forecasts.” 11.7.2019

The views expressed in this article are solely those of the author and do not necessarily reflect the views of SVB Financial Group, Silicon Valley Bank, or any of its affiliates. This material, including without limitation to the statistical information herein, is provided for informational purposes only. The material is based in part on information from third-party sources that we believe to be reliable but which has not been independently verified by us, and, as such, we do not represent the information is accurate or complete. The information should not be viewed as tax, accounting, investment, legal or other advice, nor is it to be relied on in making an investment or other decision. You should obtain relevant and specific professional advice before making any investment decision. Nothing relating to the material should be construed as a solicitation, offer or recommendation to acquire or dispose of any investment, or to engage in any other transaction.

Foreign exchange transactions can be highly risky, and losses may occur in short periods of time if there is an adverse movement of exchange rates. Exchange rates can be highly volatile and are impacted by numerous economic, political and social factors as well as supply and demand and governmental intervention, control and adjustments. Investments in financial instruments carry significant risk, including the possible loss of the principal amount invested. Before entering any foreign exchange transaction, you should obtain advice from your own tax, financial, legal, accounting and other advisors and only make investment decisions on the basis of your own objectives, experience and resources.

All non-SVB named companies listed throughout this document, as represented with the various statistical, thoughts, analysis and insights shared in this document, are independent third parties and are not affiliated with SVB Financial Group.

The views expressed in this article are solely those of the author and do not necessarily reflect the views of SVB Financial Group, Silicon Valley Bank, or any of its affiliates.

This material, including without limitation to the statistical information herein, is provided for informational purposes only. The material is based in part on information from third-party sources that we believe to be reliable but which has not been independently verified by us, and, as such, we do not represent the information is accurate or complete. The information should not be viewed as tax, accounting, investment, legal or other advice, nor is it to be relied on in making an investment or other decision. You should obtain relevant and specific professional advice before making any investment decision. Nothing relating to the material should be construed as a solicitation, offer or recommendation to acquire or dispose of any investment, or to engage in any other transaction.

Foreign exchange transactions can be highly risky, and losses may occur in short periods of time if there is an adverse movement of exchange rates. Exchange rates can be highly volatile and are impacted by numerous economic, political and social factors as well as supply and demand and governmental intervention, control and adjustments. Investments in financial instruments carry significant risk, including the possible loss of the principal amount invested. Before entering any foreign exchange transaction, you should obtain advice from your own tax, financial, legal, accounting and other advisors and only make investment decisions on the basis of your own objectives, experience and resources.

All non-SVB named companies listed throughout this document, as represented with the various statistical, thoughts, analysis and insights shared in this document, are independent third parties and are not affiliated with SVB Financial Group.