Key Takeaways

- Understand how much money you truly need now. Protect your ownership by not raising more than that amount.

- Early money is the most expensive money you’ll take. Make sure it doesn’t come with too many strings attached.

- Learn the key terms and instruments of funding. There are tools available to help forecast and understand long-term equity dilution.

Early stage founders often need to make time-sensitive fundraising decisions to propel their companies forward, yet they’ll freely admit that they rarely understand the long-term implications of their decisions.

We spoke with founders, investors and advisors to hear their tips for making sound fundraising decisions that you can use to benchmark your own experience. At the end of this article, you’ll find tables that show how founders are diluted over the long term in different scenarios.

-- Lewis

For many entrepreneurs, a successful fundraising round is a time to celebrate. For Ian Foley, a veteran of four startups, it’s always been a time of deep reflection.

The influx of money provides room to grow. But it comes at the expense of control and room to maneuver later on. By the time he founded AcuteIQ in 2014, Foley had learned an important lesson: “Only take as much capital as you think you really need.”

Figuring out how much that is, of course, is the hard part. If you raise too much, you could give away an unduly large portion of your company. If you raise too little, you risk running out of cash before you achieve the milestones needed to go back to investors again. Meanwhile, understanding the ins-and-outs of various financing instruments—convertible notes, SAFEs, equity rounds—and their long-term implications can be daunting.

So how should you go about it? Start with some good forecasting, do a fair amount of math and get help on cutting through the legalese. Here’s some advice from startup founders and advisors who’ve done it before:

Don’t raise more than you need

You’re going to get conflicting advice on this, with some people telling you to raise as much money as you can. The right answer will hinge on factors like economic conditions—bull run or downturn?—and the amount of buzz with investors your startup has generated.

Looking at it from a dilution perspective, the answer is clear: take as little outside capital as you can get away with. The money you raise early on, “is going to be the most expensive money you ever take,” says David Van Horne, a partner in the technology practice at law firm Goodwin Procter.

Your initial backers are getting equity at a time when your company has the least value, so each dollar invested buys a proportionally larger stake. That’s true even when you use an investment vehicle like a convertible note or a SAFE (which stands for simple agreement for future equity), both of which defer a decision about how much equity investors will get to a later date.

To be sure, if you raise a priced round at a high valuation, the long-term difference in dilution between raising $250,000 through notes and, say, $750,000 won’t be much. But the difference becomes more substantial if the valuation that you are able to raise at begins to rapidly decrease.

No early stage startup will be able to accurately forecast all its expenses. But you should try. Before going out to raise money, do your best to estimate what it will take to get your startup to the next stage, says Jim Marshall, head of SVB’s emerging manager practice.

“Map out the critical milestones that decrease risk in the business,” Marshall says. Once you reach that next stage, Marshall adds, “investors would be willing to pay more.”

Don’t rely on notes for too long

As you raise pre-seed funds from friends, family and angels, using convertible notes or SAFEs makes perfect sense. It allows you to get going quickly, without having to put a precise value on your company. Because of the added risk they assume, note and SAFE holders will typically get a discount when you do your first priced round.

But don’t go down this road for too long. As the amount you raise through these instruments grows, so does the pressure to raise a priced round with a high valuation. Say you’ve netted $500,000 through SAFEs or convertible notes, and when it comes to a priced round you can only command a $3 million post-money valuation, your note holders will own more than 20 percent of the company, after accounting for the discount.

“The last thing a founder wants to do is give away 40, 50 or 60 percent of the company before they've even raised a Series A, which I've seen many times,” Marshall says.

SAFE or convertible note? Don’t overthink it

Both a SAFE and a convertible note are ways to raise money without having to put a specific value on your company and determining how much equity the investor is getting.

Like a convertible note, a SAFE entitles the holder to shares, often at a discount to the first priced round. Unlike a convertible note, a SAFE doesn’t command interest and has no maturity date. Here’s a helpful primer on differences between a SAFE and a convertible note.

But keep in mind that as long as the terms are not out of the ordinary, going with one or the other won’t materially change your startup’s ownership structure in the long term.

SAFEs, which were pioneered by prominent incubator Y Combinator, have become increasingly popular in recent years, in part because templates are freely available. “More and more founders say, ‘we’re just going to use this form from YC,’” says Ivan Gaviria, a partner at law firm Gunderson Dettmer. “It can often save money in lawyers.”

Use caps as your guide

A cap is a way for note or SAFE holders to protect themselves against the dilution that would come from a startup raising a priced round at a high valuation, basically locking in a minimum future equity stake. A $5 million cap, for instance, would mean that a SAFE or note holder would own the same percentage of the company for any amount raised at or above the cap.

Founders, in general, dislike caps. It’s increasingly rare to find a deal without a cap, though. One upshot: They’re useful for understanding how much a SAFE or a note will impact dilution.

“It gives you a rough estimate of what impact it will have on you,” says Michael Cardamone, a managing director at Acceleprise, an enterprise software focused accelerator. Remember, however, that raising below that amount will cause more dilution.

Limit the options pool

You’ve raised your money, now you’ve got to build your startup team. But be mindful of the cost. “Don't allocate too large of an employee equity pool,” says startup veteran Foley, who is now a venture capitalist.

The logic here is the same as the one that underlies the calculus about how much you raise. If you give away too much to attract specific people, you end up diluting yourself and your investors more than you need.

Most startups reserve between 10 percent and 20 percent of equity for their option pools.

As you divide those pools among the staff you need, it’s worth giving special thought to how much you give to key employees early on. As a rule of thumb, a VP of engineering or head of sales who joins at the earliest stages might get between 1 percent and 2 percent. Other senior roles may warrant a half a percent.

Avoid super pro-ratas

You’ve just gotten a marquee investor interested, but as a condition of their investment, they insist on reserving the right to increase their stake in your company in future rounds, an arrangement known as super pro-rata.

“Seed investors are playing a portfolio game that involves a lot of losers,” says Gaviria. “When they get the winners, they really want to put the money behind them.” While standard pro-ratas, which allow investors to maintain their current share of ownership, serve as protection from too much dilution and are common, super pro-ratas could have a huge downside for your company, as they may deter new investors from coming in.

Many later-stage funds have target ownership stakes, and won’t invest unless they end up with at least a 10 percent to 15 percent stake, for example, says Cardamone. He recommends negotiating with investors who want for super pro-ratas. “At the end of the day, a lot of investors may ask for these sorts of things but they don’t want to get in the way of having a [future] round get done,” Cardamone adds.

The takeaway

Much of the advice we’ve discussed amounts to this: do your best to understand what you are getting yourself into; understand contractual terms; understand the math.

“I find that a lot of founders are so happy to get the money that they sign without thinking through the impacts,” Cardamone says.

There are various online tools to help with the nitty-gritty of fundraising and dilution, including Capital Calculator and Captable.io.

Once you’ve done all your homework, move quickly. Don’t waste time optimizing for a percent more here or a few thousand dollars more there. After all, you have a startup to run.

“It’s more important in the beginning stages to get the right people around the table and get smart money in relatively quickly and with relatively low friction,” Cardamone adds.

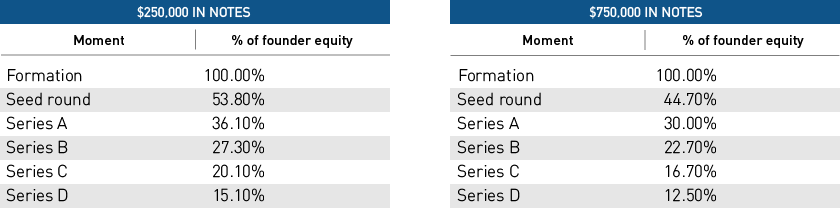

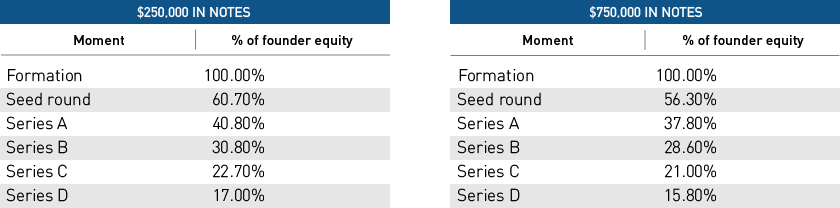

Startup equity dilution by the numbers

To show how convertible notes and SAFEs can impact dilution over the long term, we traced the percentage of a company a founder owns through four different scenarios. In each case, everything after the seed investment is the same.

Scenario 1: A company that raises a $2.5 million series seed at a $10 million post-money valuation. (Notes have a 20% discount, $8 million cap.)

Scenario 2: A company that raises a $1.5 million series seed at a $5 million post-money valuation. (Notes have a 20% discount, $8 million cap.)