Key Takeaways

- There is a high probability that foreign exchange volatility will impact your fund IRR from foreign-denominated investments; However, hedging is not for everyone.

- Venture capital investors should evaluate four key criteria to determine if action on FX is warranted: materiality, investment success likelihood, exit date visibility, and nature of the exit.

- SVB has developed a 4-point checklist that we recommend you use during the pre-close analysis and due-diligence stage of all cross-border deals in order to make informed decisions about risk management.

Click here to view the PDF.

Many funds in recent years have taken advantage of a strong US dollar to increase their capital allocations overseas: the number of funds banked by SVB that are invested internationally has doubled since 2016.1

Silicon Valley Bank serves venture capital funds offering financial services, strategic solutions and a full suite of banking products. SVB’s fund banking clients typically ask our FX advisors one question more than any other:

There is no one-size-fits-all answer. Whether it is wise for a given fund to hedge depends on a range of factors, including the asset type acquired and the relative size of the exposure.

We have developed a four-point checklist to help assist clients, as they make this important strategic and risk- based decision. This checklist may be used and referenced during the pre-close analysis and due-diligence stage of all cross-border deals.

- Materiality: How material is the potential loss from currency swings?

- Likelihood of investment success: What is the probability the deal will meet IRR goals?

- Exit timing: How much visibility and/or control do you have on the timing of the exit?

- Nature of exit: Is a cross-border transaction likely upon exit, due to the potential location of the IPO or acquirer?

Consider each item on the checklist in sequence. If a review of any of the four items finds that it would make hedging problematic or inefficient, it may indicate that the fund might not want to hedge its international positions.

Materiality

Two primary factors determine the materiality of potential currency-related losses: the size of foreign holdings and the potential impact currency fluctuations could have on them.

To gauge how the size of foreign holdings affects their materiality, measure the percentage of the fund’s net asset value made up of assets denominated in foreign currencies, broken down by currency. To measure potential impact, consider the loss that could result from an adverse move in the foreign currency. This projection varies by currency; it can be based on historical patterns or currency option prices, and generally assigns a level of probability to projected outcomes.

The combination of size and impact determines materiality. Consider the following hypothetical example:

A 20% depreciation in the euro—which would be large by historical standards—would have only a -1.5% impact on the fund’s performance.2

The upshot: Even a large currency move would present a small potential loss, so currency risk management would be a low priority.

A fund may meet the materiality threshold when:

-

both the size of a foreign-denominated position and the potential currency impact on performance are significant in their own right

-

the potential loss exceeds the fund’s risk tolerance.

For additional guidance or reference, please refer to our FX Risk Advisory white paper on materiality: Is FX material to your business?

Likelihood of investment success

The odds that a given investment will pay off tend to be relatively low for venture capital funds, which typically generate their overall returns from a handful of highly successful investments. The uncertainty around an individual investment’s likelihood of success can make it difficult for venture capital funds to hedge currency risk efficiently. The hedge contract must be supported with collateral or a credit facility at inception and settled with cash or currency at expiry, regardless of the investment performance. If the exposure fails to materialize, there is a potential for residual obligation on the hedge that would not be offset by the investment inflows.

Suppose a venture capital fund invests in 100 start-up technology companies, 90 in the US and 10 in Europe, and the fund expects 5 of the 100 to be successful. If its expectation is correct, and all firms have the same probability of success, the fund has about a 40% chance that at least one of its successful investments will be from Europe.3 As a result, the fund has significant odds of exposure to the euro.

Many funds prefer to hold off on hedging currency until there is better visibility into the likelihood of investment success. If the fund intends to participate in subsequent funding rounds, it may want to wait to hedge at least until it has deployed the last dollar of capital. For funds that have some capital invested and more to come, un-hedged positions may help mitigate risk. For example, a fall in the euro would adversely affect the value of European assets already purchased, but also would improve the purchasing power of USD capital in subsequent rounds.

Considerations related to the likelihood of investment success are clearer for growth capital funds that invest in companies further along in their life cycle and for private equity firms investing in relatively mature companies. These funds historically have more certainty around future valuations than venture capital funds do, and greater visibility into exit timing as well. Funds of these types may support having greater certainty about whether FX exposure will materialize, making them better suited to active hedging strategies.

Exit timing

Funds primarily hedge currency risk using forward contracts. Forwards enable funds to lock in a predetermined rate at which foreign currency will be converted to the home currency, typically the US dollar for US-domiciled funds, at a predetermined date. The forward represents an obligation to an amount and to a time. Visibility of exits is crucial for this second component.

Funds that focus on seed, series A and series B investments may have little visibility into their exit timing. Conversely, later-stage investors, fund-of-funds investors and credit funds that lend directly to portfolio companies have greater visibility into the timing of their exits. Likewise, funds with a strong presence on a portfolio company’s board have input and insight into both the type of exit and its timing.

All else being equal, greater visibility into a potential exit may make hedging currency risk more viable. However, there are situations in which it may also be appropriate to proceed with hedging despite exit date uncertainty. Shorter-dated hedges may be used and rolled as needed. Purchased options are also well-suited to deal with notional amount and timing uncertainties. For additional guidance on this important implementation detail, please refer to our FX Risk Advisory white paper: FX exit hedging: How far out to hedge.

Nature of exit

Different funds will have different types of exits. Private equity firms that purchase complete companies typically sell them in their entirety. When the company in question is outside the United States, the transaction often is denominated in foreign currency. Likewise, a fund-of-funds investor that invests in a fund denominated in the British pound will be paid investment returns in GBP. By contrast, fund-backed foreign life science and biotech companies sometimes opt to exit via US IPOs, so the funds can receive their returns in USD.

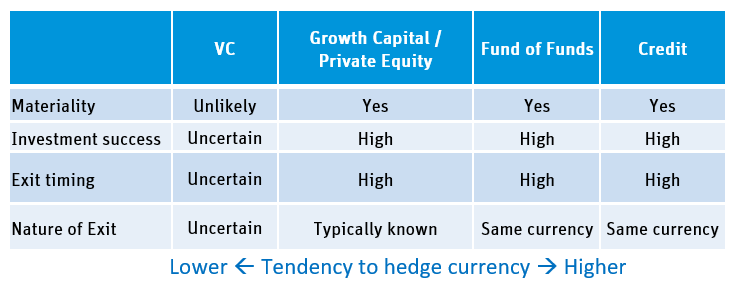

The bottom line

The table below summarizes how each type of fund might approach currency risk management.

Many venture capital firms tell us that they do not hedge their funds’ currency risk at the investment stage. SVB generally agrees. As the checklist demonstrates, hedging the underlying asset currency exposure is very difficult for most venture capital firms to justify.

The calculus is different for funds that invest in later-stage companies with higher valuations. Observations support that a much higher percentage of fund of funds investors and credit funds hedging their currency risk. The greater use of hedging is likely the appropriate path for these funds, considering the materiality of their currency risk, their likelihood of investment success, visibility into exiting timing, and the typical nature of their exits.

About Silicon Valley Bank’s Global Fund Banking FX Team

SVB’s Global Fund Banking team focuses exclusively on fund banking and has FX professionals on the east and west coasts to support your international investments. You may utilize the SVB Global Fund Banking 4-point FX Hedging Checklist when looking for a structured approach to managing currency risk. We welcome you to contact the SVB Global Fund Banking FX team as a resource, as you assess the value proposition of international investments and the associated currency risks. We are here to help at any stage of the process, from the pre-close analysis and due-diligence stage all the way through closing and beyond.

Contact Us

For more analysis on FX markets or information regarding SVB's FX services:

Contact your respective SVB FX Advisor or the SVB FX Advisory Team at fxadvisors@svb.com.

See all of SVB's latest FX information and commentary at: Foreign Exchange Advisory

1 SVB FX US Fund Client Activity Report 2016-2020

2 Calculation: [($15 million x -20%)/ $200m]

3 Calculation: 1 – probability that all European companies fail = 1 - 0.95^104